Asset Location: Optimizing Your Investments For Tax Efficiency

You’ve probably heard the investing basics: diversify your portfolio, keep costs low, stay invested for the long term. All solid advice. But there’s a less-talked-about strategy that may quietly improve your after-tax returns without necessarily changing what you’re invested in or taking on more risk. It’s called asset location, and it’s one of those planning details that tends to separate a thoughtful investment strategy from a generic one.

The concept is fairly simple: different types of accounts are taxed differently, and different types of investments generate different kinds of taxable income (or none at all). Asset location is the practice of deliberately matching your investments to the right account types, with the goal of reducing what you hand over to the IRS. It doesn’t change your overall asset allocation (your mix of stocks, bonds, alternatives, etc.), but it may noticeably improve how much of your return you actually keep.

Vanguard’s research suggests that a well-implemented asset location strategy may add between 0.05% and 0.30% of after-tax return annually,[1] which may compound into real dollars over time. More recent Vanguard research from October 2023 found that going a step further and optimizing placement of equity subclasses like U.S. vs. international and growth vs. value may add up to another 0.10% annually.[2] These are modeled estimates, not guarantees, and results will vary. But the potential is real enough to be worth understanding.

Start With the Accounts

Before you can decide what goes where, it helps to understand the three main investment account types and how each one is generally taxed.

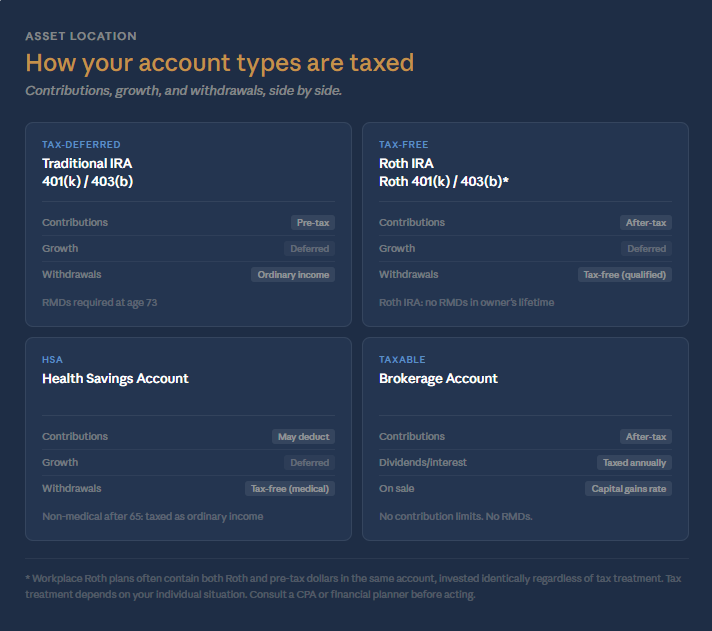

Tax-Deferred Accounts

Contributions to tax-deferred accounts (think traditional 401(k)s, IRAs, and 403(b)s) are typically made with pre-tax dollars, which may reduce your taxable income in the year you contribute. The money can grow without annual tax drag; you can generally buy, sell, and reinvest dividends inside the account without owing taxes on those transactions in the current year. The trade-off is that withdrawals in retirement are generally taxed as ordinary income. These accounts are also subject to required minimum distributions (RMDs) once you reach the required age. (Inherited IRAs come with their own RMD rules that often differ from those that apply to the original account owner, and are worth understanding separately if you’ve received or expect to receive one.)

Tax-Free Accounts

Roth accounts work differently. Contributions go in after-tax with no upfront deduction, but qualified withdrawals in retirement are generally tax-free, including all the accumulated growth. Roth IRA funds are not subject to RMDs during the account owner’s lifetime under current law. For these reasons, Roth funds may benefit the most from strong appreciation over time, since that growth may not be taxed upon qualified withdrawal.

One important nuance worth spelling out: workplace retirement plans like 401(k)s and 403(b)s often hold more than one tax type in a single account (even though it may be a Roth 401(k) or Roth 403(b) in name). Even when an employee is contributing to the Roth side, employer contributions are typically made on a pre-tax basis, meaning the same account may contain both Roth (after-tax) and pre-tax dollars. And because all funds in a workplace plan are invested through the same menu of options, everything is generally invested the same way regardless of the tax treatment of each dollar. That makes workplace plans poor candidates for implementing asset location within the account itself. It is one practical reason why rolling over retirement funds into IRAs, separating Roth dollars into a Roth IRA and pre-tax dollars into a Traditional IRA, may make sense over time, both from an asset location standpoint and for greater flexibility when managing distributions in retirement.

Health Savings Accounts (HSAs)

HSAs are sometimes lumped in with Roth accounts as “tax-free,” and for qualified medical expenses, they actually are. Contributions may be tax-deductible, the funds grow tax-deferred, and withdrawals for eligible healthcare costs are tax-free. That's a combination designed to address those specific planning goals.

As an investment vehicle for general retirement savings, though, HSAs have some real limitations worth keeping in mind. After age 65, you can withdraw HSA funds for any purpose, but non-medical withdrawals are taxed as ordinary income, similar to a traditional IRA. And the inheritance treatment is notably less favorable than a Roth IRA: when an HSA passes to a non-spouse beneficiary, the full account value is generally included in the beneficiary’s taxable income in the year of inheritance.[3] For these reasons, HSAs are often better suited to lower-volatility investments, particularly if the account could pass to heirs or if non-medical withdrawals in retirement are a realistic possibility.

Taxable Brokerage Accounts

Taxable accounts don’t offer upfront deductions or tax-free withdrawals, but they come with flexibility the other account types can’t match. There’s no contribution limit, no RMDs, and generally no restriction on when you can access the money. Investments held here are subject to capital gains tax when sold (at the generally lower long-term rate if held more than a year) and dividends may qualify for preferential tax rates as well.

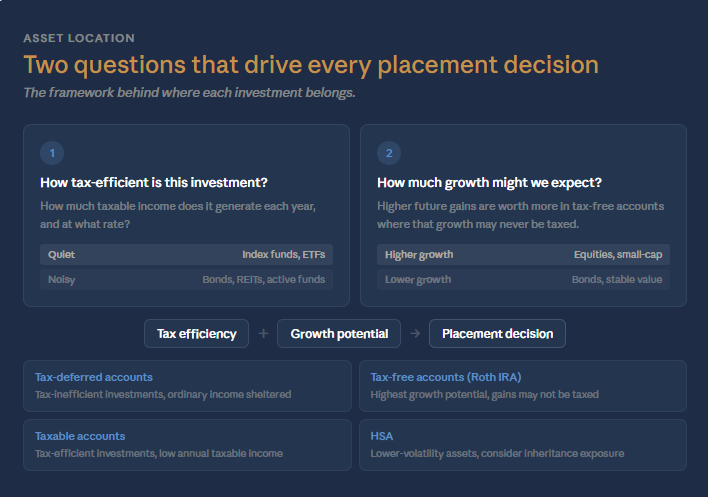

The Two Lenses That Drive Asset Location

Once you understand the accounts, asset location decisions generally come down to two overlapping questions: How tax-efficient is this investment? And how much growth might we expect from it?

Lens 1: Tax Efficiency

Some investments are relatively quiet from a tax perspective. A broad U.S. stock market index fund, for example, typically has low turnover and mostly qualified dividends, meaning it may not generate much of an annual tax bill if held in a taxable account.

Other investments are noisier. Taxable bond funds generate interest income every year, and that interest is typically taxed at ordinary income rates, the same rates that apply to your wages. REITs (real estate investment trusts) present a similar consideration: a large share of their distributions are often treated as ordinary income rather than the more favorably taxed qualified dividends, though they may qualify for a 20% deduction on that income under the Tax Cuts and Jobs Act.[4] Actively managed equity funds with high turnover may also generate short-term capital gains distributions taxed at ordinary rates, rather than the lower long-term capital gains rate that applies to longer-held positions.

The principle that follows: investments that tend to generate a lot of ordinary income are often better placed in a tax-sheltered account, where that income may compound without an annual tax hit. Investments that tend to generate less taxable income, or income that qualifies for lower rates, may be a better fit in a taxable account.

Lens 2: Growth Potential

The second lens is about making the most of your tax-free space. Consider two scenarios: a Roth IRA that grows from $100,000 to $400,000 over time, where all of that $300,000 gain could be tax-free upon qualified withdrawal, versus that same $300,000 gain inside a traditional IRA, which would likely be taxed as ordinary income when withdrawn. All else being equal, you’d take the tax-free account. (Safe assumption.) So apply that thinking to how you allocate within each account: generally, you’d prefer your higher-growth investments to be in the accounts that may not tax the gains.

Higher-growth assets held over long accumulation periods are often considered good candidates to hold more of in Roth accounts, since their future gains may not be taxed upon qualified withdrawal. Conversely, lower-growth, income-producing assets like investment-grade bond funds are often reasonable fits for a traditional IRA. Withdrawals would generally be taxed as ordinary income, but bond interest in a taxable account would likely have been taxed at ordinary rates anyway. The net result is that tax-deferred shelter gets applied where it may provide the most benefit.

Putting It Together: A General Framework

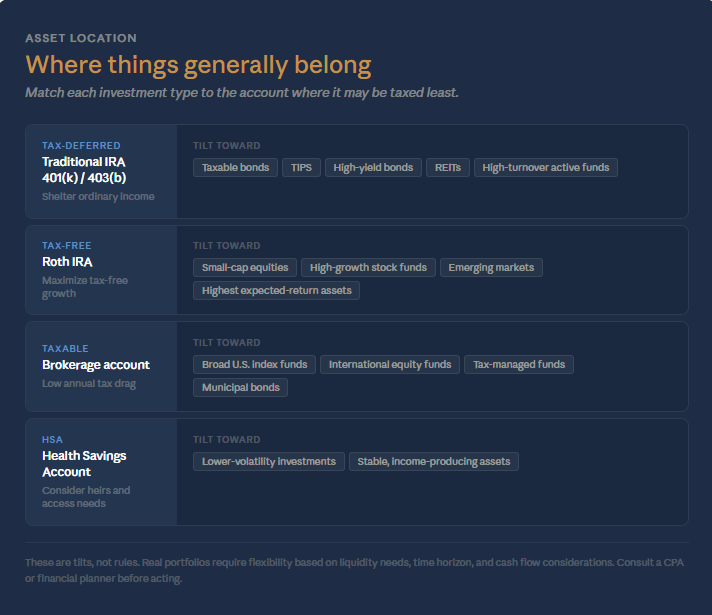

Combining both lenses produces a rough framework, though your specific situation always matters:

•Tax-deferred accounts: Tilt toward investments that generate more ordinary income. Sheltering that income from annual taxation may help reduce tax drag over time.

•Tax-free accounts (Roth IRAs specifically): Tilt toward assets with stronger long-term appreciation potential, since qualified gains may not be taxed upon withdrawal. As noted above, this applies more cleanly to IRAs than to workplace plans, where the mixed tax nature of the account limits what you can do with asset location.

•Taxable brokerage accounts: Tilt toward tax-efficient assets that generate relatively modest annual taxable income, or assets that carry specific tax advantages that are only accessible when held in a taxable account.

As Fidelity has put it: “You can’t control market returns, and you can’t control tax law, but you can control how you use accounts that offer tax advantages.”[5]

Worth emphasizing: these are tilts, not rules. Asset location is a directional framework, not a rigid prescription. You don’t have to perfectly segregate every holding to get value from it. Holding some bonds in a taxable account, some equities in a traditional IRA, or some growth assets in an HSA doesn’t mean the strategy is broken. It means you’re working with real constraints, which is what everyone is doing.

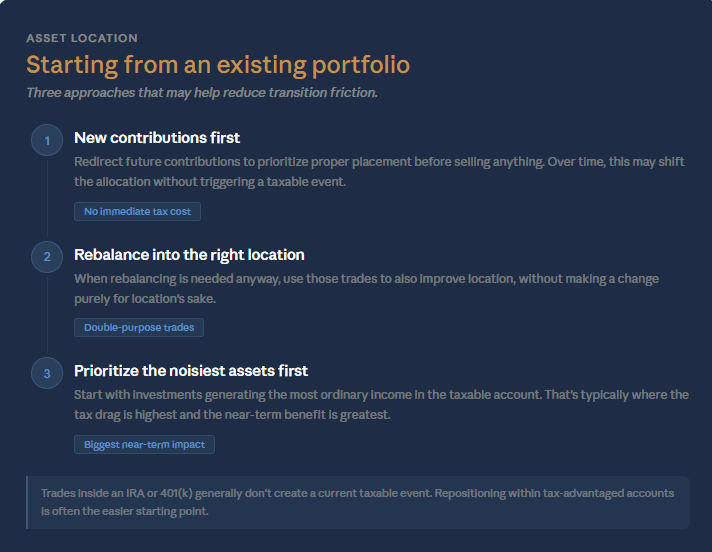

If You’re Starting from an Existing Portfolio

If your investments are already spread across multiple accounts and you haven’t been thinking about asset location, getting started isn’t always as simple as deciding where new contributions go. In many cases, moving toward a better-located portfolio will require selling some existing holdings and repositioning them into different accounts.

That transition has real costs. Selling appreciated investments in a taxable account to move them could trigger capital gains taxes. Depending on how long you’ve held those positions and your current bracket, that tax bill may offset some of the near-term benefit. There’s no universal answer here; it depends on the size of the embedded gain, your time horizon, and your current and expected future tax rates.

A few approaches that may help reduce transition friction:

•New contributions first. Redirect future contributions to prioritize proper placement before selling anything. Over time, this may help shift the allocation without triggering a taxable event.

•Rebalance into the right location. When the portfolio drifts, and rebalancing is needed anyway, use those trades to also improve location. Selling bonds in a taxable account and replacing them with equities while moving the bond exposure to a traditional IRA improves placement without making a change purely for location’s sake.

•Prioritize highest-income-generating assets first. If you can only reposition some holdings in the near term, start with the investments generating the most ordinary income in the taxable account. That’s typically where the tax drag is highest.

For investments already inside an IRA or 401(k), repositioning is generally simpler because trades within a tax-advantaged account don’t generate a current taxable event. If your bonds are sitting in a Roth IRA and your equities are in a traditional IRA, you may be able to swap the allocations without immediate tax consequences.

This is one area where working through the numbers with a financial planner tends to be worthwhile, since the right pace of transition often depends on a careful look at your specific situation.

Layering In Additional Strategies

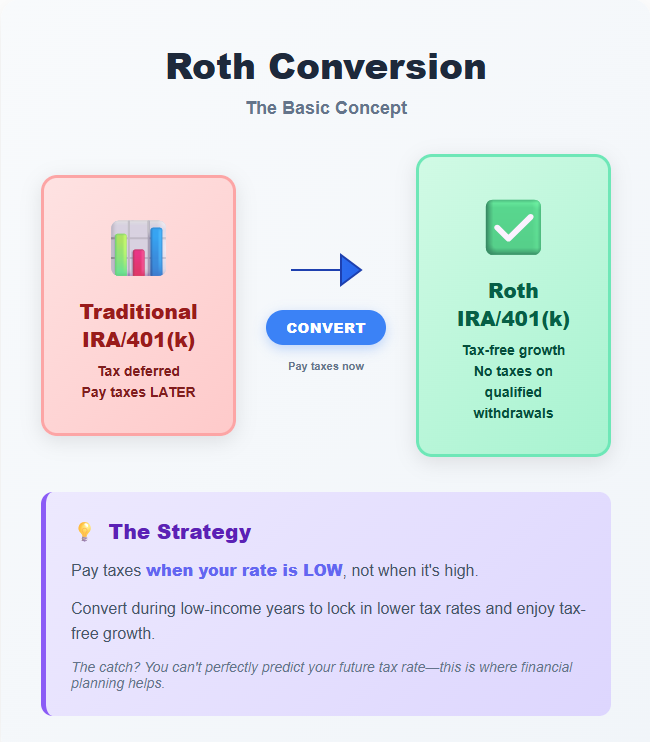

Asset location works best as part of a broader tax-planning framework. Two strategies that pair naturally with it are tax-loss harvesting and Roth conversions.

Tax-loss harvesting involves strategically selling investments that have declined in value to realize a loss that may offset capital gains elsewhere in the portfolio, or up to $3,000 of ordinary income per year. Because harvesting plays out in taxable accounts, the composition of that account matters. A well-located taxable account holding tax-efficient equities tends to create more harvesting opportunities over time, since equity positions are more likely to experience periodic declines that may be harvested without significantly disrupting the overall strategy.

Roth conversions involve deliberately moving pre-tax dollars from a traditional IRA or 401(k) into a Roth account and paying taxes at today’s rate. Done systematically, particularly in lower-income years before RMDs begin, conversions may grow the pool of tax-free space available for higher-growth assets. These strategies may also reinforce each other: harvested losses in a taxable account can sometimes offset the income generated by a Roth conversion in the same year, potentially reducing the net tax cost of both.

I’ve written in more detail about Roth conversion strategies and the value of coordinated investment planning if either is useful context for how asset location fits in the bigger picture.

A Few Practical Caveats

Asset location tends to add the most value when you have solid balances across multiple account types. If your retirement savings are concentrated entirely in one type of account, there’s limited ability to optimize placement. The more diversity you have across taxable, traditional, and Roth accounts, the more flexibility you have to apply these principles.

Asset location is a portfolio-level strategy, not an account-level one. Each individual account will hold a different mix of investments and will likely perform differently in any given year. A bond-heavy traditional IRA will look very different from a Roth IRA holding primarily equities. If you evaluate each account in isolation, this may feel disorienting. The right lens is how all of your accounts perform together.

Related to that: these decisions don’t exist in a vacuum. Asset location works best when considered alongside your broader accumulation strategy (how you’re building assets across different account types over time), your distribution strategy (which accounts you plan to draw from first in retirement and in what sequence), and your anticipated cash flow needs in both the near and longer term. A placement decision that looks optimal on paper may be less so if it creates friction with how you plan to access the money, triggers unnecessary taxes when you need liquidity, or conflicts with a Roth conversion strategy you’re running in parallel.

As a practical example: it may make sense to hold a sizable bond position in a taxable account for a period of time if those funds are earmarked for a specific near-term purpose, but the time horizon is still longer than a savings account would warrant. That’s not a failure of the strategy; it’s a reasonable acknowledgment that liquidity needs and optimal placement don’t always line up perfectly. The framework is directional guidance, and real financial lives require flexibility.

Rebalancing also requires some coordination. When the overall portfolio drifts from its target allocation, getting it back on track ideally involves trades that don’t create unnecessary taxable events.

And finally: tax law changes. The favorable treatment of qualified dividends and the REIT pass-through deduction under the TCJA have already evolved, and may continue to. A solid asset location strategy is worth reviewing periodically rather than treating as a one-time setup.

The Bottom Line

Asset location may add real value, but it works best on top of a solid foundation: a diversified, low-cost portfolio with an asset allocation that fits your goals and time horizon. The strategy is an optimization layer, not a substitute for getting the fundamentals right first.

For investors who have multiple account types and are in higher tax brackets, the potential is worth taking seriously. Done thoughtfully, it generally comes down to intentional placement decisions made when accounts are funded and revisited as part of ongoing planning.

One honest reality: knowing the right strategy and actually implementing it, then continuing to monitor and maintain it over time, are two different things. If you know you’re unlikely to follow through on the mechanics on your own, or that periodic review tends to slip when life gets busy, working with an advisor as an accountability partner is a practical solution. Beyond building the initial plan, an advisor may help ensure that rebalancing, repositioning, and tax-layer decisions like loss harvesting and Roth conversions actually happen when the opportunity is there, rather than sitting on a to-do list indefinitely. I wrote more about that dynamic in Your Finances Called, if that resonates.

This is where personalized analysis tends to matter most, because the right approach depends on your specific account balances, tax situation, investment mix, and time horizon.

Sources

1. Vanguard, “Asset Location Can Lead to Lower Taxes,” Vanguard Investor Education. investor.vanguard.com

2. Sachin Padmawar et al., “Asset Location for Equity,” Vanguard Research, October 2023. corporate.vanguard.com

3. Internal Revenue Code § 223; IRS Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans. Regarding HSA inheritance: IRC § 223(f)(8); upon death, a non-spouse beneficiary must include the fair market value of the HSA in gross income in the year of the account holder’s death.

4. Internal Revenue Code § 199A; Tax Cuts and Jobs Act of 2017 (P.L. 115-97). The 20% deduction on qualified REIT dividends is currently scheduled to expire after December 31, 2025, absent Congressional action.

5. Andrew Bachman, Director of Financial Solutions, Fidelity Investments, as cited in Fidelity Viewpoints, “Asset Location: Investing in the Right Accounts.” fidelity.com

Disclosures

The information contained in this article is intended for educational purposes only and does not constitute tax or investment advice. Asset location strategies depend on individual circumstances including account balances, tax situation, investment mix, and time horizon. Results discussed in this article are illustrative and modeled; they are not guarantees of future performance. Please consult a qualified financial and/or tax professional for guidance specific to your situation. Tax laws are subject to change; the TCJA provisions referenced, including the Section 199A deduction, are subject to Congressional action beyond 2025.

Investment advisory services are offered through Fiduciary Financial Advisors, a registered investment adviser. This article is for informational and educational purposes only and should not be construed as personalized investment, tax, or legal advice. Any references to scheduling a consultation are for general informational purposes and do not create an advisory relationship. Third-party research, statistics, and survey data cited are believed to be reliable but have not been independently verified. All data is subject to change. References to CFP® professionals relate to industry research and do not imply that any specific outcome will be achieved.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

You Left Your CalPERS Employer. Now What?

A plain-language guide to your options when you leave a CalPERS-covered job before you're ready to retire

Maybe you landed a role in the private sector. Maybe you relocated for family reasons. Maybe the job just wasn't the right fit anymore. Whatever happened, you've left your CalPERS-covered employer before retirement, and now you have the question: what actually happens to the benefits you've been building?

The short answer is that CalPERS doesn't disappear from your life. This article walks through those choices in plain language so you can make an informed decision rather than a default one.

What You've Built

When you work for a CalPERS-covered employer, two things are happening in your account at the same time. First, you're making employee contributions, which are a percentage of your salary set by your retirement formula and membership tier. Second, your employer is making its own contributions on your behalf into the broader fund. Only the first bucket (your own contributions plus the interest they've earned) is refundable to you. Employer contributions aren't yours to take with you; they go toward funding pension benefits for current and future retirees across the system.[1]

The pension benefit itself, that lifetime monthly payment you've heard described as "2% at 62" or "2.7% at 57" or some similar formula, isn't funded from a personal account the way a 401(k) is. It's a defined benefit: a promise from CalPERS to pay you a calculated amount for life once you reach eligibility.[2]

Are You Vested?

Your vesting status is the key factor in understanding your options. CalPERS uses a two-part test: you need both sufficient service credit and minimum age to collect.[3]

The Service Credit Side

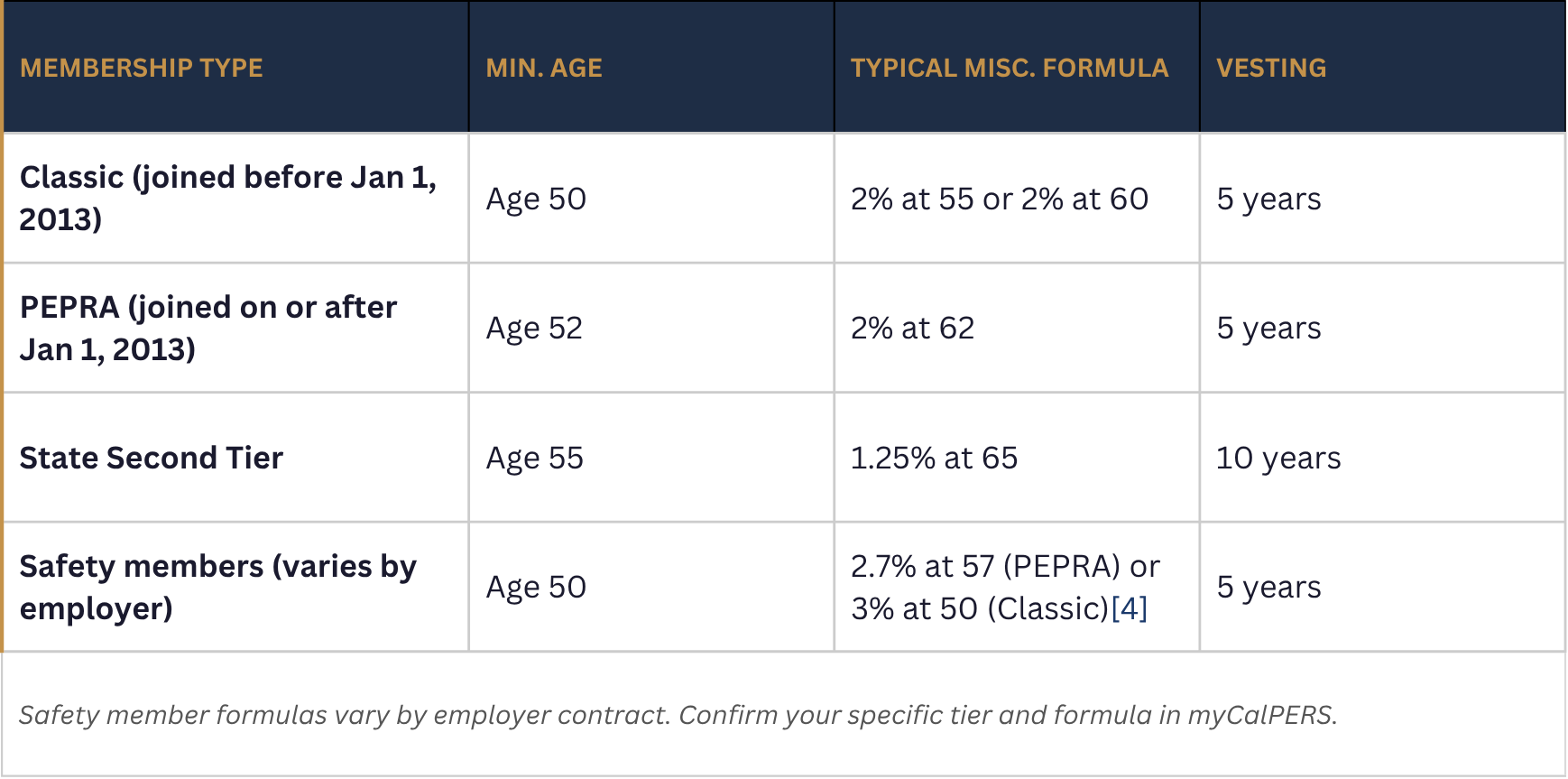

For most CalPERS members, the vesting threshold is five years of CalPERS-credited service. There are some exceptions, most notably for State of California Second Tier employees, who generally need 10 years, but the five-year mark applies to the large majority of members working for state agencies, cities, counties, etc.[3]

If you've crossed that five-year threshold, you're considered vested in the pension side of things, meaning the right to a future benefit is locked in regardless of where you work next. If you haven't yet hit five years, you don't have a right to a future pension unless you return to CalPERS-covered employment, use reciprocity with another qualifying public retirement system, or had part-time status that qualifies under a specific exception.

The Age Side

Vesting in the service credit sense doesn't mean you can start collecting tomorrow. You also have to reach the minimum retirement age for your formula, which varies depending on when you became a CalPERS member:[4]

So, for example, if you're a 38-year-old Classic miscellaneous member with eight years of service credit and you leave your employer today, you're vested in the service credit sense, but you can't collect until you reach at least age 50. That gap, between your separation date and your earliest retirement eligibility date, is what makes the decisions below so consequential.

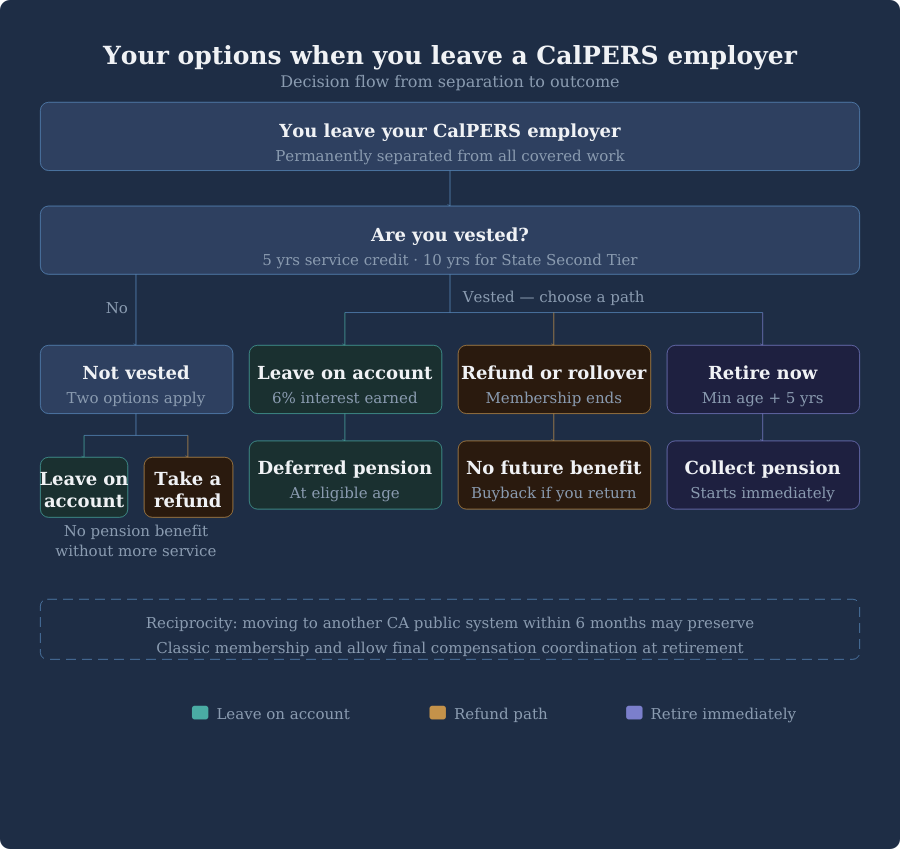

Your Three Main Options at Separation

Once you've permanently left all CalPERS-covered employment, CalPERS will mail you a document called Options at Separation. It lays out what comes next. In practice, you have three paths.[5]

Option 1: Leave Your Contributions on Account

You can leave your employee contributions exactly where they are, earning interest, until you reach minimum retirement age and choose to retire. CalPERS credits accounts left on deposit with interest at a rate of 6% per year, and your membership and service credit remain fully intact.[6]

If you're vested, this approach preserves your right to a lifetime pension payment starting at minimum retirement age. The pension amount you'd eventually receive is based on your service credit at separation, your final compensation, and your age when you actually retire. You won't earn additional CalPERS service credit during the years you're working elsewhere, but the credit you built doesn't evaporate.

One thing to know about this option: under federal Required Minimum Distribution rules, if you haven't retired or refunded your account, CalPERS will eventually require a distribution. The age threshold depends on your birth year: age 73 for those born between 1951 and 1959, and age 75 for those born in 1960 or later.[7] If you're leaving public employment mid-career, that deadline is likely far enough away to not be a factor in the initial decision.

Option 2: Take a Refund or Roll Over Your Contributions

You can request a refund of your employee contributions and the interest they've earned. This terminates your CalPERS membership. Once you choose this path, you forfeit your right to any future pension benefit, disability retirement, or survivor benefits under CalPERS.[8]

The refund is taxable as ordinary income unless you roll it over into a qualified retirement account (an IRA or an eligible employer plan that accepts rollovers). If you receive the money directly, CalPERS is required to withhold 20% for federal income tax, and you may face an additional 10% early withdrawal penalty if you're under 59½ and don't roll the funds over.[9]

If you later return to CalPERS-covered employment and want to buy back your prior service credit, you can do so, but the cost is typically higher than what you were originally refunded, and it increases over time as interest accrues.[8]

Option 3: Retire Immediately (If You're Eligible)

If you've reached minimum retirement age and have at least five years of service credit, you may be eligible to apply for retirement now rather than deferring it.[4] This tends to come up most often for members who've spent a longer career in public service, or who are separating later in their working years.

Retiring at the minimum age typically means accepting a lower benefit factor than if you waited, since most CalPERS formulas are structured to reward retiring later. It also means your CalPERS health benefits question comes into focus immediately (more on that below). For many people, the timing question of when to start CalPERS benefits involves a breakeven analysis that intersects with Social Security timing, other savings, and healthcare coverage, so it pays to run those numbers before making the call.

Reciprocity With Another Public Retirement System

If you're leaving one public employer and heading to another, or you're considering it, CalPERS has reciprocal agreements with most other California public retirement systems. Reciprocity allows you to coordinate benefits between systems in a way that tends to be more favorable than treating them as entirely separate.[14]

The mechanics work like this: there's no transfer of funds or service credit between systems. Instead, when you retire from both systems simultaneously (using the same retirement date), your highest final compensation from either system can be used to calculate the pension from each. You draw separate retirement payments from each system.[14]

To establish reciprocity, the main rule to know is the six-month window: you need to move from one reciprocal system to the next within six months, without a gap in active membership.[15] If you take more than six months off before joining a new public employer, reciprocity likely won't apply.

Reciprocity also affects your CalPERS membership tier. Classic members who move to another CalPERS-covered employer within six months typically retain their Classic membership status, which matters quite a bit given the more generous formulas Classic tiers carry relative to PEPRA.[16]

Reciprocal systems include, but are not limited to Other CalPERS-covered employers (which automatically share membership); CalSTRS (California State Teachers’ Retirement System); County “1937 Act” systems such as LACERA, SCERS, and others; San Francisco Employees’ Retirement System (SFERS); and various other qualifying California public retirement systems. If you’re moving to a position under one of these systems, ask both systems about reciprocity before your start date.

What to Think Through Before You Decide

The options at separation aren't equally consequential for everyone. Here is what you should think through:

• Are you vested? If you haven't hit five years of service credit, your options look different than if you have. A non-vested member taking a refund isn't forfeiting a pension they'd otherwise have. A vested member doing the same often is.[3]

• How long until minimum retirement age? The longer the runway, the more you want to think carefully about whether leaving contributions on account makes sense.[4]

• Will you return to public sector work? If there's any realistic chance you'll come back to a CalPERS employer, keeping your membership intact is probably the better decision. Service credit is additive, and buying it back later is expensive.[8]

• What's the reciprocity picture? If you're heading to another California public employer, verify the six-month window and establish reciprocity before your start date. This is one of the decisions that's easy to get right.[15]

• What does your retirement income picture look like overall? CalPERS pension income, if it's eventually payable, is one piece of a broader picture that often includes Social Security, your Savings Plus Program (which is comprised of a 457(b) and 401(k) plan), or other deferred compensation balance, and non-retirement savings. The refund decision looks different depending on what else is in that picture.

• What's the tax impact of a refund? If you're taking a refund in a year with high other income, the tax drag can add up. If you're in a lower-income year, the impact is more manageable. Rolling into an IRA avoids current taxation but still closes the CalPERS door.[9]

Don't Lose Track of Your Account

CalPERS will send you an Annual Member Statement every fall, but those go to the address on file. Keep your contact information current in myCalPERS, and check your account periodically, especially as you approach your eligible retirement window.[17]

This is where it gets personal.

The choice between leaving contributions on account, taking a refund, and establishing reciprocity intersects with your tax situation, your other retirement savings, your career plans, and how you model lifetime income. The right answer depends on the details of your situation. If you've recently left a CalPERS-covered employer and want to think through your specific numbers, I'm happy to help you work through it.

Sources

1. CalPERS. "Refund Member Contributions." calpers.ca.gov/page/active-members/retirement-benefits/refund-member-contributions

2. CalPERS. "Service & Disability Retirement." calpers.ca.gov/members/retirement-benefits/service-disability-retirement

3. CalPERS PERSpective. "CalPERS 101: Your Pension and the Vesting System." news.calpers.ca.gov/your-calpers-pension-is-on-a-vesting-system-heres-what-that-means

4. CalPERS. "Options at Separation" (PDF). calpers.ca.gov/documents/options-at-separation/download

5. CalPERS. "Options at Separation" letter (PDF). calpers.ca.gov/documents/options-at-separation/download

6. CalPERS. "A Benefits Guide for Public Agency Members" (PDF). calpers.ca.gov/documents/new-member-public-agency-guide/download

7. SECURE 2.0 Act of 2022; IRS Final Regulations on Required Minimum Distributions (89 Federal Register 58886, eff. Jan. 1, 2025). federalregister.gov/documents/2024/07/19/2024-14542/required-minimum-distributions

8. CalPERS. "Refund Member Contributions." calpers.ca.gov/page/active-members/retirement-benefits/refund-member-contributions

9. CalPERS. "Refund Election Form Packet — Special Tax Notice: Your Rollover Options" (PDF). calpers.ca.gov/documents/refund-election-form-packet/download

10. CalPERS. "Eligibility & Enrollment (Active Members)." calpers.ca.gov/members/health-benefits/eligibility-and-enrollment

11. CalPERS. "COBRA Coverage." calpers.ca.gov/members/health-benefits/eligibility-and-enrollment/cobra

12. CalPERS. "Eligibility & Enrollment (Retirees)." calpers.ca.gov/retirees/health-and-medicare/eligibility-and-enrollment

13. CalPERS PERSpective. "Health Vesting 101." news.calpers.ca.gov/health-vesting-101/

14. CalPERS. "Reciprocity (Linking Retirement Systems)." calpers.ca.gov/members/retirement-benefits/reciprocity

15. CalPERS PERSpective. "What You Need to Know About Reciprocity." news.calpers.ca.gov/what-you-need-to-know-about-reciprocity-2/

16. CalPERS. "Public Employees' Pension Reform Act (PEPRA)." calpers.ca.gov/page/about/laws-legislation-regulations/public-employees-pension-reform-act

17. CalPERS. "A Benefits Guide for Public Agency Members" (PDF). calpers.ca.gov/documents/new-member-public-agency-guide/download

Disclosures

Fiduciary Financial Advisors does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action. Before investing, consider investment objectives, risks, fees, and expenses. Investments in securities involve the risk of loss, including loss of principal. Past performance is no guarantee of future returns. The views and opinions reflected in the content are subject to change at any time without notice. The content speaks only as of the date indicated. Some information was obtained from external sources. The information is believed to be accurate, but there is no guarantee that it is.

This content is for educational purposes only and does not constitute personalized tax, legal, or investment advice. Consult a qualified CFP®, CPA, or attorney before taking action.

Fiduciary Financial Advisors is a registered investment adviser. Nothing here constitutes individualized investment advice. Examples are illustrative only and not recommendations. No guarantee of future results. Third-party data is not independently verified.

CFP® and CERTIFIED FINANCIAL PLANNER® are certification marks owned by the CFP Board.

Market Commentary: Midyear 2026

Four Themes Shaping the First Half of 2026

In the first half of 2026, there was plenty of news, but a few different themes in particular stand out to me: a war in the Middle East that unsettled energy markets for months, a new Federal Reserve chair who took a more cautious stance than expected (given the current administration’s pressure), and growing scrutiny of the artificial intelligence (AI) theme that has driven so much of the market's recent gains, both in how AI is being used inside companies and how AI-related revenue is being generated among the largest technology firms.

Through it all, the Standard & Poor's 500 (S&P 500) finished the first half up 10.21% on a price basis[1], a number that hides how uneven the path to get there actually was. This commentary walks through these threads that influenced the first six months of the year and may continue to shape the second.

Federal Reserve and Interest Rates

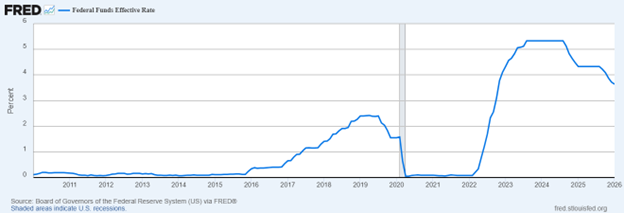

Jerome Powell's term as Fed chair ended on May 15. Kevin Warsh, confirmed by the Senate in a 54-45 vote, was sworn in on May 22.[2] He was widely viewed as the more rate-cut-friendly, reform-minded choice, having criticized the Fed's communication habits, argued for a smaller balance sheet, and suggested AI would help bring inflation down over time[3]. Though it's notable that Powell remains on the board as a voting member, a dynamic that adds another layer of uncertainty to how policy debates may unfold in the second half.

On June 17, the Federal Open Market Committee (FOMC) held rates steady at 3.50% to 3.75% for a fourth consecutive meeting. Warsh shortened the post-meeting statement, removed language signaling the Fed's future intentions, and declined to submit his own interest rate forecast, consistent with his stated skepticism of the exercise.[4] The other eighteen participants, however, leaned more strongly toward keeping rates higher than expected, with several now projecting at least one rate hike by year-end, a reversal from the rate cut the median projection had implied as recently as March.[5] The reasoning: inflation has proven stickier than hoped, with the Consumer Price Index (CPI) running 3.8% year over year in April, the highest since 2023, and the core Personal Consumption Expenditures (PCE) index, the Fed's preferred inflation gauge, moving from 3.0% to 3.3% over the same stretch.[6] (This is still nowhere near the 9.1% peak CPI hit in June 2022, the highest reading in roughly 40 years, which triggered the Fed to raise rates from near zero to over 5% in just about a year and a half.[22]) Energy prices tied to the Iran war are a sizable part of that story, layered on top of a labor market still adding jobs at a pace that gives the Fed little urgency to ease.

A practical note for rate watchers: for those who have been waiting on a rate drop to refinance and lower your monthly payment, that wait could run longer than expected. A mortgage recast is an option for anyone sitting on a lump sum in the interim, since it doesn't depend on rates moving at all. It keeps your existing rate and loan term but applies a sizable principal payment to the balance, then recalculates the monthly payment based on what's left owed, all without the appraisal, credit check, or closing costs of a full refinance. It's typically only available on conventional loans and usually carries a modest processing fee.

Middle East Conflict and Market Impact

On February 28, the United States and Israel launched a joint operation against Iran that killed Supreme Leader Ali Khamenei and opened a regional war that also reignited the Israel-Hezbollah conflict in Lebanon.[7] Iran responded in part by closing the Strait of Hormuz, the waterway carrying roughly 20% of the world's seaborne oil and liquefied natural gas (LNG). Shipping traffic fell more than 90% in the weeks that followed.[8]

Energy markets bore the brunt of it. Brent crude jumped from about $71 to $77 a barrel within days of the first strikes, eventually breaking $100, while West Texas Intermediate (WTI) crude peaked near $113 in April. By mid-June, prices had retreated toward the high $70s as ceasefire talks progressed, though Hormuz traffic still has not returned to pre-war levels, and full normalization isn't expected until 2027 even under an optimistic scenario.[9]

Equity markets moved in step with the headlines, selling off through much of March as the conflict widened, then surging when a ceasefire was first announced on April 8, with the Dow gaining over 1,300 points and the S&P 500 up 2.5% that day alone.[10] The United States and Iran signed an agreement on June 17 that paused large-scale hostilities, but it has been tested repeatedly since: a drone strike on a cargo ship on June 25, a U.S. response the next day, Iranian missiles and drones aimed at U.S. bases in Kuwait and Bahrain, and a second ship hit and a second night of U.S. strikes on June 27.[11]

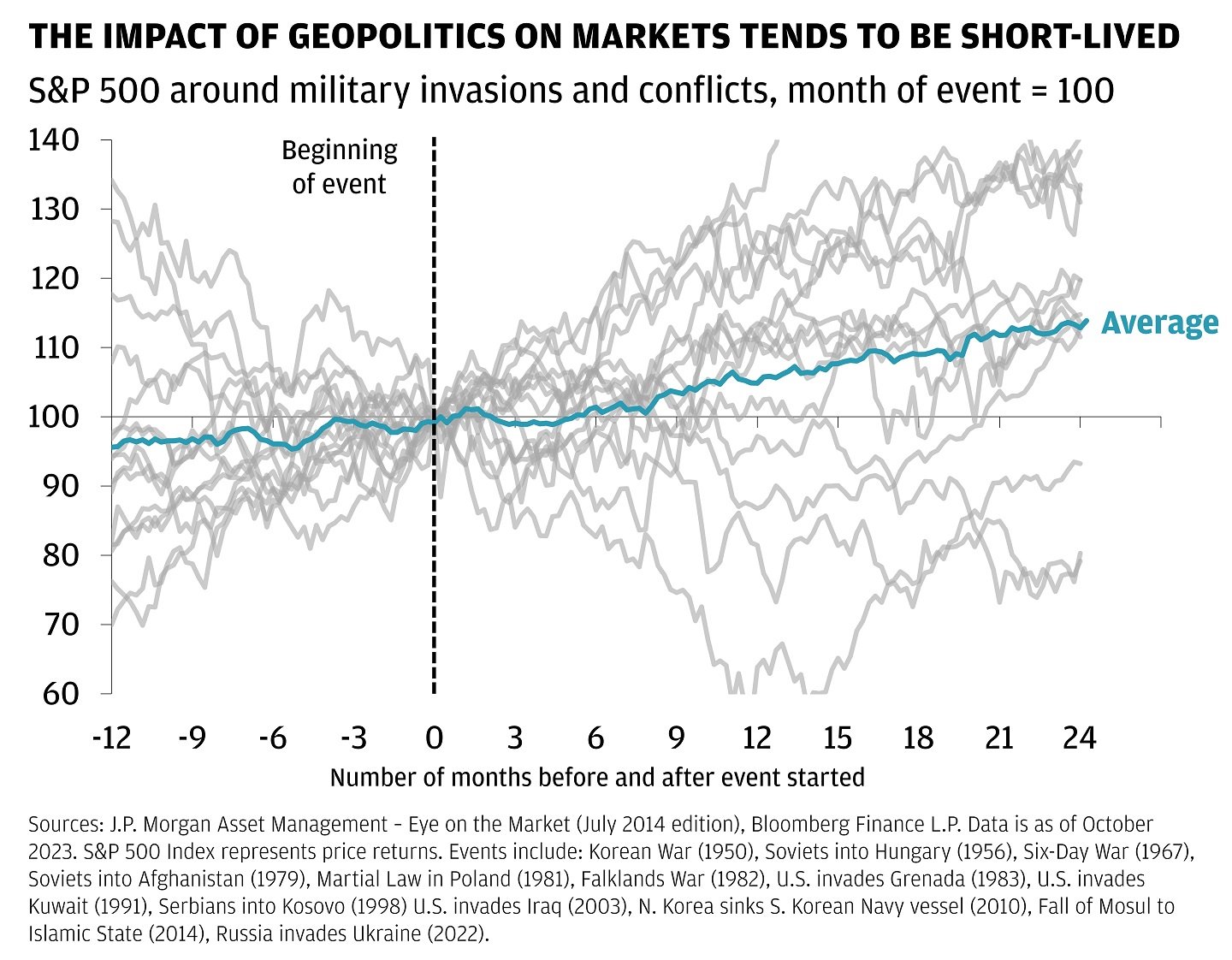

This is the second time in just over a year that an Iran-related conflict has rattled markets, which makes it a useful moment to revisit how markets have historically absorbed military shocks. The two charts illustrate the longer-term picture.

In addition to the charts shown from JP Morgan and Dimensional Fund Advisors, research from LPL and Hartford Funds, looking across dozens of post-World War II shocks, finds an average decline of roughly 5% following a geopolitical event, with markets typically bottoming within about three weeks and recovering within one to two months, and the S&P 500 historically higher a year out about 70% of the time. J.P. Morgan's research group found a similar pattern across seventeen modern conflicts dating back to the Korean War: the S&P 500 sat modestly below its pre-conflict level a year out, then stood roughly 14% above the conflict-month level two years later.[12] The 2026 episode has tracked that pattern reasonably well so far, even though the International Energy Agency has described the disruption to oil markets as the largest in the industry's history.[13]

S&P 500 around military conflicts (month of event = 100)

Artificial Intelligence and Productivity

A widely discussed report from Glean, the Work AI Index 2026, surfaced interesting findings. By the survey's count, 87% of knowledge workers now use AI at work, 73% say it makes them more productive, and the average reported time savings comes to 13 hours a week. Those are individual self-assessments, however. When it comes to actual organizational outcomes, only 13% of those same workers say their organization is performing better as a result, suggesting that individual time savings are not automatically translating into measurable business improvements.[14] Glean's head of Work Innovation, Rebecca Hinds, has a name for part of the gap: “bot sitting,” the roughly 6.4 hours a week employees spend feeding context to AI systems, correcting their output, and cleaning up after them, invisible labor that eats into the time AI was supposed to free up. Sixty-nine percent of workers admit they have shipped AI-generated work they could not explain or defend if asked, a pattern the report labels “bot slop.”[15]

The dynamic is showing up in corporate budgets, too. Uber reportedly exhausted its 2026 AI tools budget well ahead of schedule due to higher than anticipated costs, and one technology executive noted that at some companies, the cost of the compute now runs ahead of the cost of the employees it was meant to support.[16] For investors, the relevant question isn't whether AI tools are useful; it's whether the productivity gains baked into AI-related earnings and capital spending assumptions are translating as cleanly as advertised. If a sizable share of “time saved” is being reallocated to managing the tools rather than higher-value work, the payback period on enterprise AI spending may run longer, and less predictably, than current stock market valuations assume.

AI Earnings Concentration Risk

A small group of companies, Nvidia, Microsoft, OpenAI, Oracle, Advanced Micro Devices (AMD), and CoreWeave among them, have built an increasingly interconnected web of investments and purchase commitments, where a sizable share of one company's revenue traces back to another company's investment in it.[17] Nvidia has committed up to $100 billion to OpenAI, which in turn uses Nvidia chips to build out data centers. Microsoft's roughly $13 billion stake in OpenAI has been delivered largely as Azure cloud credit, which OpenAI spends back with Microsoft. Oracle's $300 billion infrastructure agreement with OpenAI is filled mostly with Nvidia hardware, and Nvidia holds a stake in CoreWeave while supplying it chips, even as OpenAI holds its own stake in CoreWeave while buying its cloud capacity.[18]

Supporters call this a strategic necessity given how capital-intensive AI infrastructure has become and how scarce advanced chips remain.[19] Critics see something closer to the vendor financing arrangements of the dot-com era, in which companies effectively funded their own customers' purchases to inflate the appearance of organic demand. Investor Michael Burry, whose early, contrarian bet against the 2008 housing market was dramatized in the film The Big Short (one of my favorites if you haven't seen it), began shorting Nvidia and Palantir in late 2025 on similar grounds, and reiterated the comparison again in May.[20] Tech sector bond issuance reached roughly $428 billion in 2025, the cost of insuring against default by Oracle and Microsoft has nearly doubled since last fall, and Goldman Sachs recently raised its 2026 AI capital spending estimate to about $527 billion.[21] Whether this amounts to a bubble likely comes down to whether external, organic demand for AI products catches up to the revenue being generated inside this closed loop. If it does, the arrangement looks like ordinary supply chain financing. If it doesn't, the unwind could be sharp, given how concentrated these companies have become within major indexes.

Index Returns

Index / Indicator YTD Returns Through 6/30/2026

S&P 500 Index +10.21%

Russell 2000 Index (small caps) +22.57%

MSCI All Country World ex USA (international stocks) +13.05%

MSCI Emerging Markets Index +23.85%

Bloomberg U.S. Aggregate Bond Index +1.15%

Bloomberg Municipal Bond Index +2.32%

Dow Jones Global Select REIT Index (real estate) +13.32%

Index returns sourced from Dimensional Fund Advisors Periodic Performance Report, 1/1/2026 – 6/30/2026.

Treasury Yields as of July 1, 2026

Yields (as of 7/1/2026)

Fed Funds Target Rate 3.75%

3-Month Treasury 3.85%

6-Month Treasury 4.00%

2-Year Treasury 4.17%

5-Year Treasury 4.24%

10-Year Treasury 4.48%

30-Year Treasury 4.97%

Treasury yields sourced from U.S. Department of the Treasury via Charles Schwab, as of July 1, 2026. Index returns are for illustrative purposes and do not reflect the returns of any actual investment. Past performance is not indicative of future results.

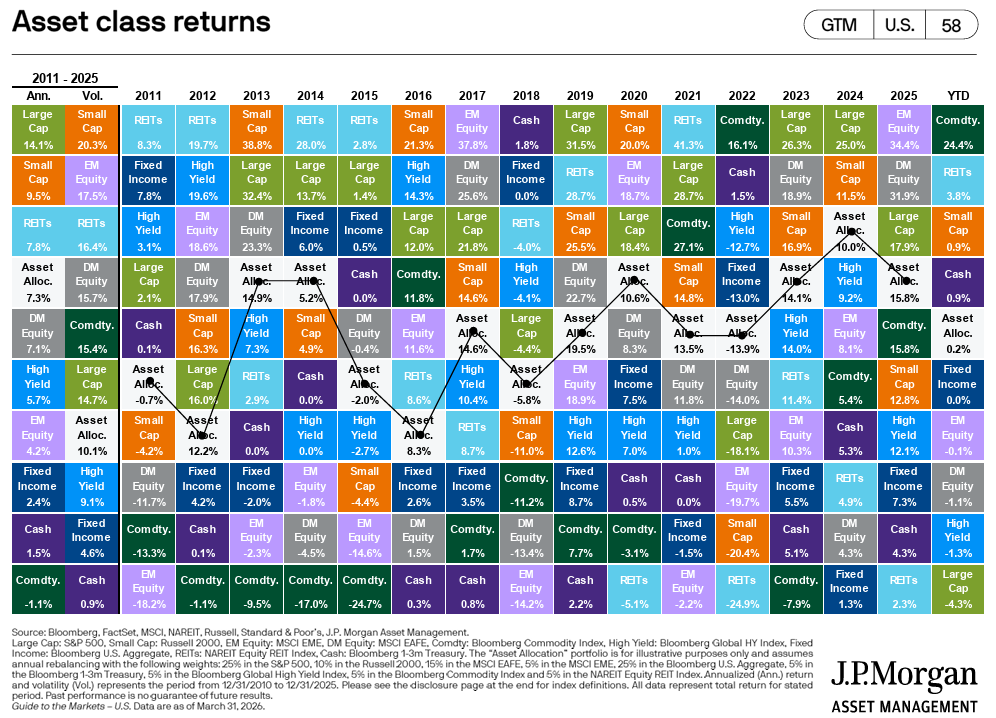

The S&P 500 finished the first half of the year up 10.21%, but the broader return picture tells a more interesting story. Emerging markets (+23.85%), small-cap U.S. stocks via the Russell 2000 (+22.57%), and international developed stocks (+13.05%) all outpaced the S&P 500 by a wide margin, a theme covered in more depth in my recent article, Is the S&P 500 Really All You Need?. Bonds were positive but modest, with the Bloomberg U.S. Aggregate returning 1.15%. On the yield side, the 2-year Treasury at 4.17% sitting above the Fed Funds rate of 3.75%, and the 30-year rate approaching 5% signals a more normal-looking yield curve compared to recent years, when shorter-term rates were running even with or above long-term rates.

Portfolio Considerations

None of these stories are reason for alarm for a diversified investor, nor are they the whole story (I didn’t even touch on SpaceX's record IPO, which the initial stock prices arguably imply that its newer AI and computing bets pay off years down the line.) However, they raise a few questions worth considering:

1. How much of my equity exposure rides on a small number of mega-cap technology companies, and am I comfortable with that level of concentration if AI-related earnings growth slows?

2. Does my fixed income allocation account for a higher-for-longer, and possibly higher-still, rate environment, rather than the rate cuts that looked likely at the start of the year?

3. Has my time horizon or risk tolerance shifted in a way my portfolio hasn't caught up to yet?

4. If markets got bumpy over the next year or two, do I have enough in liquid reserves (keeping in mind that a diversified fixed income allocation can serve as a longer-term buffer) that I wouldn’t need to sell equity holdings to cover an unexpected expense or income disruption?

These are exactly the kinds of questions to work through together, in the context of a full financial picture rather than headline by headline.

Sources

1. Dimensional Fund Advisors, Periodic Performance Report, Monthly: 1/1/2026 – 6/30/2026, as of June 30, 2026. Index returns are for illustrative purposes and do not reflect the performance of any actual investment.

2. NPR, "Senate confirms Kevin Warsh as next chair of the Federal Reserve," May 13, 2026; Federal Reserve Board press release, May 15, 2026; Brookings, "Who has to leave the Federal Reserve next?"

3. CNN Business, "Kevin Warsh nominated by Trump to be the next Federal Reserve chair," January 30, 2026; CCN, "Kevin Warsh Officially Replaces Fed Chair Jerome Powell," May 17, 2026.

4. CNBC, "Fed interest rate decision June 2026: Fed holds rates steady," June 17, 2026; Lord Abbett, "June Fed Meeting: Policy Signals from the New Chairman."

5. Lord Abbett, June 2026 FOMC analysis; Bondsavvy, "June 2026 Dot Plot: What It Means for Money Market Yields."

6. U.S. Bureau of Labor Statistics, Consumer Price Index news release, April 2026; U.S. Bureau of Economic Analysis, Personal Income and Outlays, April 2026; U.S. Bank, "Fed holds rates steady as new Chair Kevin Warsh commits to price stability."

7. Britannica, "2026 Iran war"; Wikipedia, "2026 Iran war."

8. House of Commons Library, "Israel/US-Iran conflict 2026: Reopening the Strait of Hormuz"; Congressional Research Service, R45281.

9. CNBC, "Oil prices turn lower as U.S.-Iran ceasefire extension awaits Trump approval," May 28, 2026; CNBC, "Oil drops 20% from 2026 peak," May 29, 2026; House of Commons Library, op. cit.

10. NBC News, "Iran war ceasefire sends oil prices tumbling and stocks soaring," April 9, 2026.

11. CBS News, "U.S. strikes targets in Iran after Iranian drone attack on cargo ship," June 26, 2026; Al Jazeera, "US launches second night of strikes on Iran after ship hit by drone," June 27, 2026; NPR, "U.S. strikes multiple targets in Iran in response to tanker attack," June 27, 2026; CNN, "US launches more strikes on Iranian sites," June 27, 2026.

12. LPL Research and Hartford Funds historical analyses, as summarized in Focus Partners Wealth, "Geopolitical Conflict and Markets: A Brief History Lesson"; J.P. Morgan Wealth Management, "Crisis in the Middle East: Assessing Potential Market Impacts," jpmorgan.com; Seeking Alpha, "Since 1953 This Is How The S&P 500 Has Performed After A Major Geopolitical Shock," April 2026.

13. International Energy Agency, as cited in Wikipedia, "Economic impact of the 2026 Iran war."

14. Glean, Work AI Index 2026, as discussed by Rebecca Hinds on The Cognitive Revolution; summarized in Biggo Finance, "Rebecca Hinds on the 13-Hour AI Lie."

15. Ibid.

16. Fortune, "The AI economy could crash on mounting chip costs," May 30, 2026.

17. Bloomberg, "AI Circular Deals: How Microsoft, OpenAI and Nvidia Keep Paying Each Other," March 11, 2026; Wikipedia, "AI bubble."

18. CraftedCharts, "AI Circular Financing: Nvidia, Microsoft & OpenAI"; Noah Smith, "Should we worry about AI's circular deals?"; Global Finance Magazine, "AI's Financial Circle Game."

19. Noah Smith, op. cit.; Global Finance Magazine, op. cit.

20. Wikipedia, "AI bubble"; Global Finance Magazine, op. cit.

21.Investing.com, "2026: Another Year of AI Bubble Not Bursting?"; Fortune, op. cit.

22. U.S. Bureau of Labor Statistics, "Consumer prices up 9.1 percent over the year ended June 2022, largest increase in 40 years," The Economics Daily, July 13, 2022, bls.gov.

Disclosures

Fiduciary Financial Advisors does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action. Before investing, consider investment objectives, risks, fees, and expenses. Investments in securities involve the risk of loss, including loss of principal. Past performance is no guarantee of future returns. The views and opinions reflected in the content are subject to change at any time without notice. The content speaks only as of the date indicated. Some information was obtained from external sources. The information is believed to be accurate, but there is no guarantee that it is.

This commentary is for informational purposes only and does not constitute investment, tax, or legal advice. The views expressed reflect current conditions and are subject to change without notice.

Fiduciary Financial Advisors is a Registered Investment Adviser. Past performance is not indicative of future results, and there is no guarantee that any forecast or projection discussed will come to pass. Third-party data referenced above has not been independently verified by Fiduciary Financial Advisors.

CFP® and Certified Financial Planner® are certification marks owned by the Certified Financial Planner Board of Standards, Inc., and are awarded to individuals who meet its education, examination, experience, and ethics requirements.

86% of California State Employees Are Handling Their Finances Alone.

Here’s What They May Be Missing.

If you work for the State of California, SMUD, Caltrans, CDCR, or any other CalPERS-covered employer, you have access to a strong retirement benefit package. A defined benefit pension, Savings Plus 401(k) and 457(b) options, and (depending on your role) Social Security coordination that often requires careful planning.

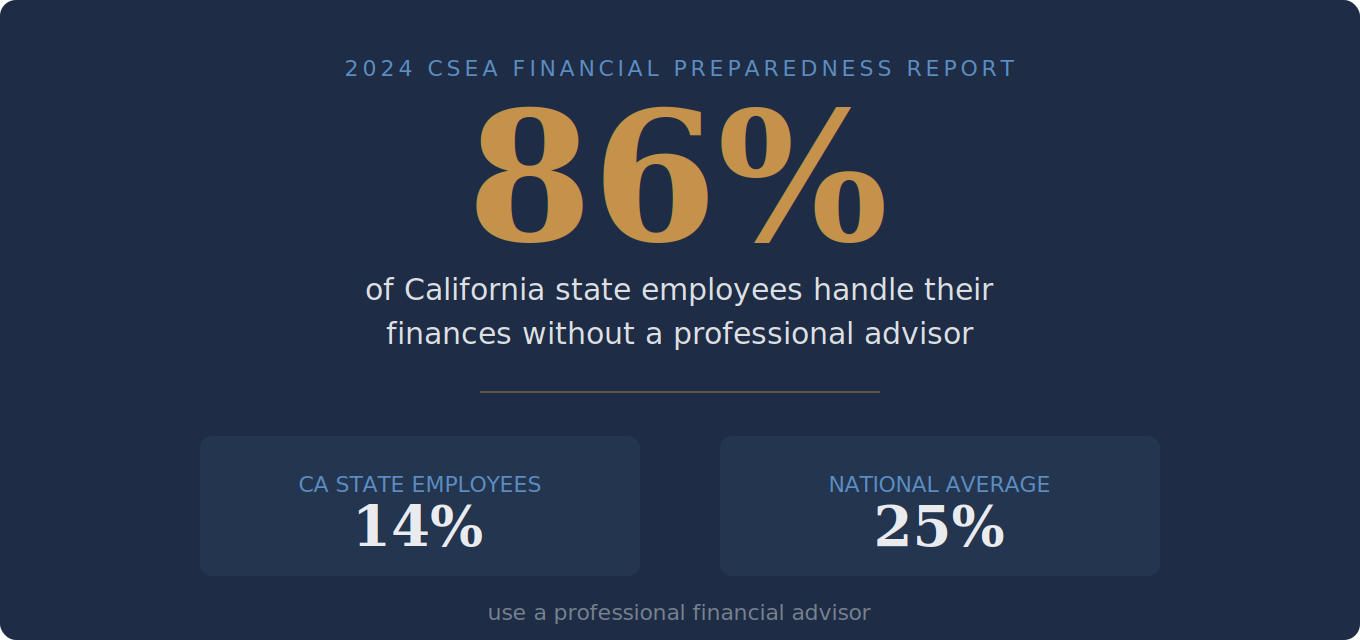

And yet, according to a recent financial preparedness survey of nearly 5,000 California state employees, the overwhelming majority of you are navigating all of that on your own.[1]

That’s not a judgment. It’s a data point. And it’s worth understanding why it matters.

What the Research Actually Says

The 2024 California State Employees Financial Preparedness Report, published by the California State Employees Association (CSEA) and based on a survey of active and retired state workers, found some numbers that are hard to ignore:[1]

86% of California state employees handle their own financial and retirement planning, relying on friends, family, and online resources rather than a professional advisor.

Only 14% use a professional financial advisor, compared to roughly 25% of Americans nationally.

When researchers asked why, the answers were familiar: it costs too much, I don’t have enough saved, I haven’t found someone I trust, or I just don’t think I need one.[1]

Those are all reasonable-sounding explanations. But here’s where the data gets interesting, because the same survey measured how those two groups actually feel about their financial lives.

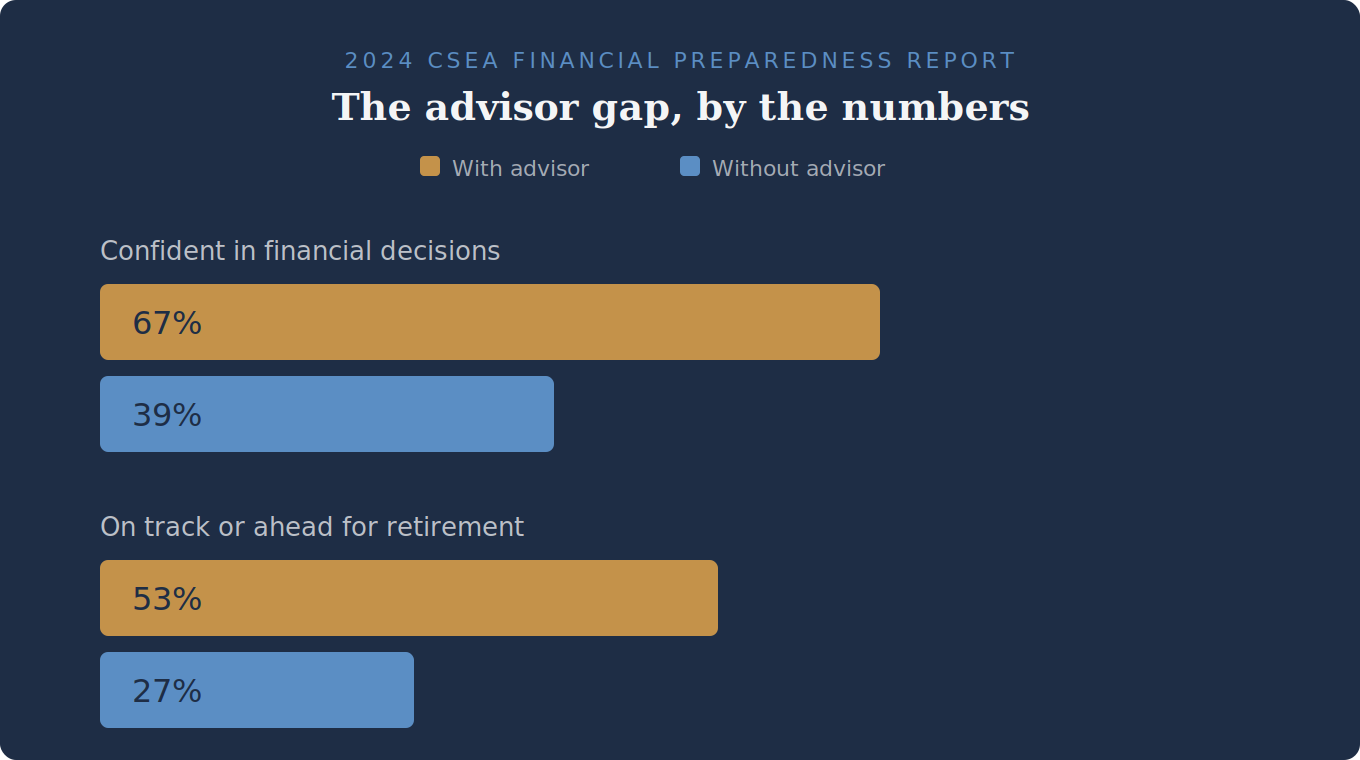

The Confidence Gap You Can Measure

State employees with an advisor: 67% felt confident in their financial decision-making. State employees without an advisor: 39%.

State employees with an advisor: 53% said they were on track or ahead of schedule for retirement. State employees without an advisor: 27%.

That’s not a marginal difference. That’s roughly double the confidence and nearly double the retirement readiness, at least as self-reported.[2]

Now, correlation is not causation (people who seek out advisors may already be more financially engaged). But the gap is wide enough to raise a question worth sitting with: if you’re in the 86% handling your finances without professional guidance, what are the odds there are opportunities you haven’t fully considered?

What DIY Planning May Miss for CalPERS Employees

The reason this matters more for public employees than, say, someone with a basic 401(k) and no pension is that your benefits stack is notably complex. There are moving parts that interact with each other, and because some of those decisions (like your pension option election or retirement date) are difficult or impossible to undo, the cost of a misstep may compound over time.

Here are some of the areas where a qualified advisor tends to help clarify the picture for CalPERS members:

Pension Timing and Retirement Date Optimization

Your CalPERS benefit is calculated using a formula, and the timing of when you retire may significantly affect your monthly benefit for life. Retiring right before versus right after a birthday quarter, for example, may change your benefit factor. Many employees look at their pension estimate and assume that’s the number, without realizing that a few strategic adjustments to timing could increase their monthly income (or overlook the impact that a prior divorce may have if the pension benefit was part of the settlement).

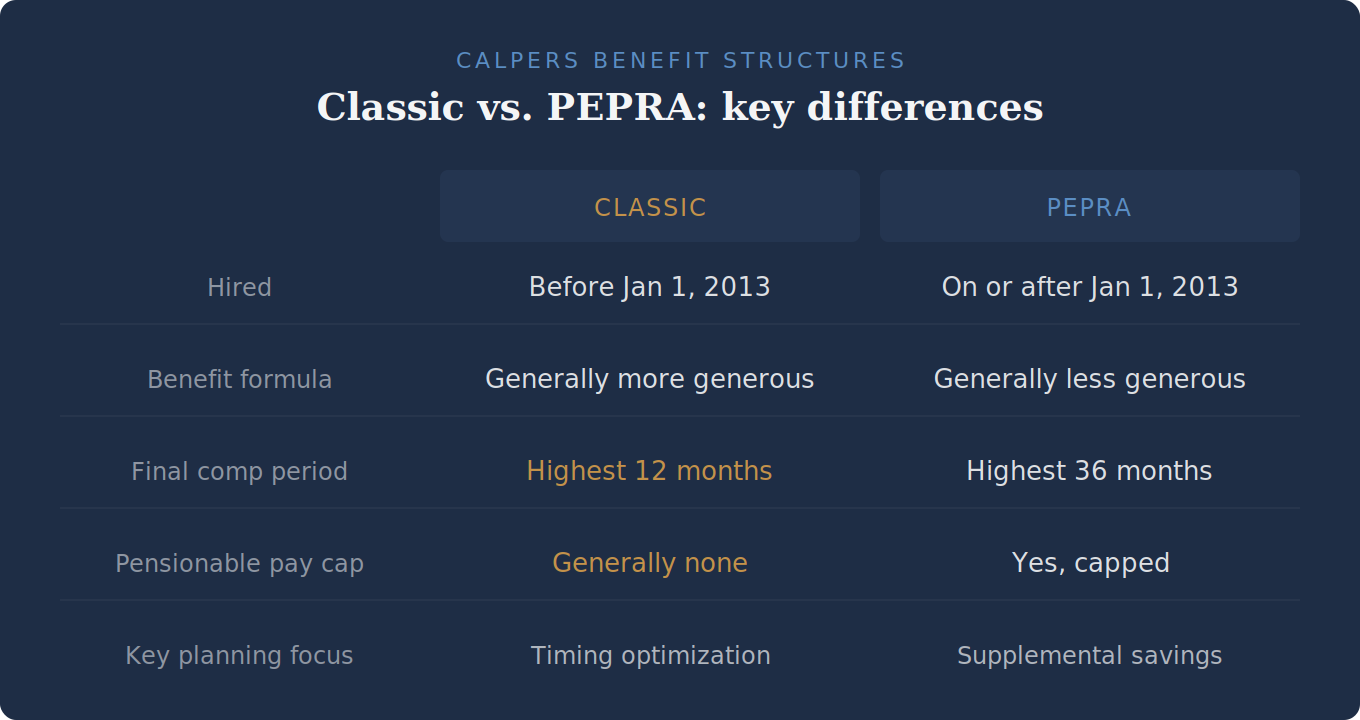

And the stakes here differ depending on when you were hired. If you started with a CalPERS-covered employer before January 1, 2013, you’re a “Classic” member with a generally more generous benefit formula, and your final compensation is based on your highest 12 consecutive months of pay. If you were hired on or after that date, you fall under PEPRA (the Public Employees’ Pension Reform Act), which uses a generally less generous formula, a 36-month final compensation period, and a cap on the salary that counts toward your pension. (For simplicity, this overview focuses on miscellaneous members. Safety members and State Second Tier members have different formulas and benefit structures.)[3]

That’s a significant difference. A Classic member nearing retirement may have a richer benefit, but that also means more complex optimization decisions around timing, final comp windows, and retirement option elections. A PEPRA member, on the other hand, is generally working with a less generous formula, which may make supplemental savings strategy and tax planning that much more important for closing the gap between their pension income and the retirement lifestyle they want. Either way, understanding which set of rules applies to you (and how to work within them) is one of the areas where professional guidance may be worth exploring.

Savings Plus Strategy (the 401(k)/457(b) Decision)

If you’re a state employee, you have access to both a 401(k) and a 457(b) through Savings Plus, which means you may be able to contribute up to $49,000 per year in 2026 (or more if you’re over 50 or nearing retirement and eligible for catch-up provisions).[4] But many employees may not be maximizing both plans, and may not be thinking strategically about whether to use pre-tax, Roth, or a combination. The right answer depends on your current tax bracket, your expected pension income, your other sources of retirement income, and your timeline. This is especially true for PEPRA members, whose pension formula and pensionable pay cap may make supplemental savings through Savings Plus an important lever for building retirement security.

And if you work for an employer like SMUD that offers its deferred compensation through Fidelity rather than the Savings Plus/Nationwide platform, the investment options and fee structures are different, which may matter for how you allocate.

Social Security Coordination

Not every CalPERS member pays into Social Security (it depends on your employer’s specific arrangement).[5] For those who do, coordinating your pension income, Savings Plus distributions, and Social Security claiming strategy may noticeably affect your total after-tax retirement income. For those who don’t, understanding how that gap affects your overall plan may be just as important.

Tax Planning Around Retirement

Your CalPERS pension is fully taxable as ordinary income. So are distributions from your Savings Plus accounts (unless they’re Roth). If you’re retiring in California, where state income tax rates may run above 9% for many retirees, the difference between a tax-aware withdrawal strategy and just taking money as you need it may be larger than you’d think.

This is where Roth conversion planning in the years leading up to retirement tends to be especially valuable, and where DIY planners may not realize what options are available to them.

Why Most People Put This Off

(Even When They Know Better)

If you’ve been meaning to get your financial plan together "someday," you’re in very large company. Financial procrastination isn’t laziness. It’s usually one of a few predictable things:

The complexity feels overwhelming. CalPERS alone has multiple benefit formulas, PEPRA vs. Classic distinctions, reciprocity rules, and different employer contracts. Add in Savings Plus, Social Security, tax planning, and retirement timing decisions, and it’s understandable that many people just default to "I’ll figure it out later."

There’s no forcing function until retirement is close. Unlike a leaky roof or a check engine light, the consequences of not having a plan often don’t show up right away. But by the time they do (often in the form of a tax surprise, a suboptimal pension election, or a realization that you can’t retire when you planned), the window to fix things has narrowed.

Trust is a real barrier. The CSEA survey confirmed this.[1] Many state employees haven’t found an advisor they trust, and that’s an understandable concern. Not every advisor understands CalPERS benefits, Savings Plus options, or the specific planning challenges that come with public sector employment. Working with someone who doesn’t know your benefits package well can sometimes feel worse than doing it yourself.

What to Look for If You’re Considering Working with Someone

If you’re a CalPERS member who’s been thinking about getting professional guidance (even if you’ve been thinking about it for a while), here are a few things that tend to matter most:

Fiduciary standard. Look for an advisor who is legally required to act in your best interest, sometimes referred to as a fiduciary. That’s an important distinction worth understanding when evaluating any advisor relationship.

Familiarity with public sector employees and pension benefits. There’s a difference between a generalist financial planner and one who has experience working with pension benefits and public sector employees. Ask whether they’ve worked through pension optimization, deferred compensation strategy, and retirement tax planning with people whose benefits look like yours. Ask how many clients they serve in similar situations.

A comprehensive approach, not just one piece of the puzzle. A good financial plan for a CalPERS member doesn’t stop at a retirement projection. It connects your pension, your supplemental savings, your tax situation, and your investment strategy into a coordinated approach. Look for someone who ties these pieces together rather than addressing them in isolation.

The Bottom Line

You’ve built a career in public service, and the benefits you’ve earned along the way are valuable. But they’re also complex, and the gap between a good plan and no plan may be wider than you’d expect over the course of a retirement.

If you’re one of the 86% who’s been going it alone, that doesn’t mean you’ve been doing it wrong. It might just mean you haven’t found the right fit yet.

Interested in talking through your CalPERS benefits and how they fit into your bigger financial picture? You can schedule a no-obligation introductory conversation below.

Sources

California State Employees Association (CSEA). “2024 California State Employees Financial Preparedness Report.” Published 2024. Survey of nearly 5,000 active and retired California state employees conducted November 2023. N=3,817 active employees (95% confidence, ±2%), N=1,172 retirees (95% confidence, ±2%). Available at cseabenefitsprogram.com.

CSEA. “DIYing Your Own Retirement Savings Plan? Here’s What You Need to Know.” cseabenefitsprogram.com, 2024. National advisor usage estimate (25%) cited from 2022 Harris Poll. Confidence and retirement readiness comparisons derived from the 2024 Financial Preparedness Report.

CalPERS. “Public Employees’ Pension Reform Act (PEPRA).” calpers.ca.gov. PEPRA took effect January 1, 2013, establishing new benefit formulas, final compensation periods, and pensionable compensation caps for members hired on or after that date.

Internal Revenue Service. “401(k) limit increases to $24,500 for 2026; IRA limit increases to $7,500.” irs.gov, November 2025. The 401(k) and governmental 457(b) elective deferral limits are separate, allowing combined contributions of up to $49,000 ($24,500 each) before catch-up provisions.

CalPERS. “Social Security & Your CalPERS Pension.” calpers.ca.gov. Social Security coverage varies by employer arrangement. Non-covered positions (often safety classifications and certain State of California roles) do not withhold Social Security taxes. The Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) were repealed by the Social Security Fairness Act, signed into law January 5, 2025.

Disclosures

This post is for educational purposes only and does not constitute tax, legal, or investment advice. Please consult a qualified financial planner, CPA, and/or attorney before making decisions about your investments.

Investment advisory services are offered through Fiduciary Financial Advisors, a registered investment adviser. This material is for educational and informational purposes only and is not individualized investment, tax, or legal advice. Equity compensation rules are complex and outcomes depend on plan terms, trading windows, holding periods, and individual tax circumstances. Consult your CPA and/or attorney regarding your situation. Any performance shown is historical, for illustrative purposes, and does not indicate future results. Examples are not representative of all securities or outcomes and are not recommendations to buy or sell any security. Data may be obtained from third-party sources believed to be reliable but not independently verified.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

Is the S&P 500 Really All You Need?

Why Concentrating Everything in U.S. Large-Cap Stocks Is a Risk Most Investors Are Not Prepared For

If you spend any time in personal finance communities online, you have probably encountered the “VOO & Chill” crowd. The pitch is seductively simple: buy an S&P 500 index fund, hold forever, ignore everything else, and get rich. Why complicate it? The S&P 500 has crushed pretty much everything over the past 15 years. What more evidence do you need?

Quite a bit, actually.

And while we’re at it: this same crowd tends to be loudly, confidently against paying advisory fees. (More on that another time.)

The “just buy the S&P 500” strategy isn’t wrong because index investing is bad. Broadly diversified, low-cost index investing is one of the best things that happened to retail investors in the last 50 years. It’s wrong because it conflates an index fund with the only index you need. Concentrating everything in U.S. large-cap stocks is a real, identifiable risk. And history has handed us the receipts more than once. (Repeatedly. With interest.)

Let’s walk through it.

1. The Story the Last Decade Tells Is Not the Only Story

First, a quick vocabulary note. When people say “the S&P 500,” they mean an index of roughly 500 of the largest publicly traded companies in the United States, most of them household names: Apple, Microsoft, Amazon, Nvidia, and so on. When you buy a fund that tracks the S&P 500, you essentially own a small slice of all of them at once. It’s a good idea, as far as it goes. The problem is the “as far as it goes” part.

It’s easy to understand why U.S. large caps look unbeatable right now. The S&P 500 delivered extraordinary returns through the 2010s and into the early 2020s, largely driven by a handful of mega-cap technology companies. If you owned an S&P 500 fund from 2010 to 2024, you were richly rewarded. International markets, emerging markets, small caps, and value stocks all lagged by comparison. It felt obvious: why own anything else?

That kind of thinking has a name: recency bias. It’s the tendency to assume that whatever has worked recently may keep working indefinitely. Think of it like driving while staring in the rearview mirror. The road behind you looked great. That says nothing about what’s ahead. In investing, recency bias tends to be one of the most expensive cognitive shortcuts you can make. (And to be clear, everyone makes it. The question is whether you catch yourself before it costs you.)

The historical record tells a more complicated story. According to Morgan Stanley Investment Management, international stocks have outperformed U.S. markets in four separate decades since World War II: the 1950s, the 1970s, the 1980s, and the 2000s. During those cycles, international stocks beat U.S. returns by a median of roughly 4.9% per year.[1] The current stretch of U.S. dominance is not the rule. It’s the exception. (An unusually long one, which is kind of the point.)

“The four most dangerous words in investing are: this time it’s different.” — Sir John Templeton

2. The Lost Decade: A Preview of What Concentration Can Cost You

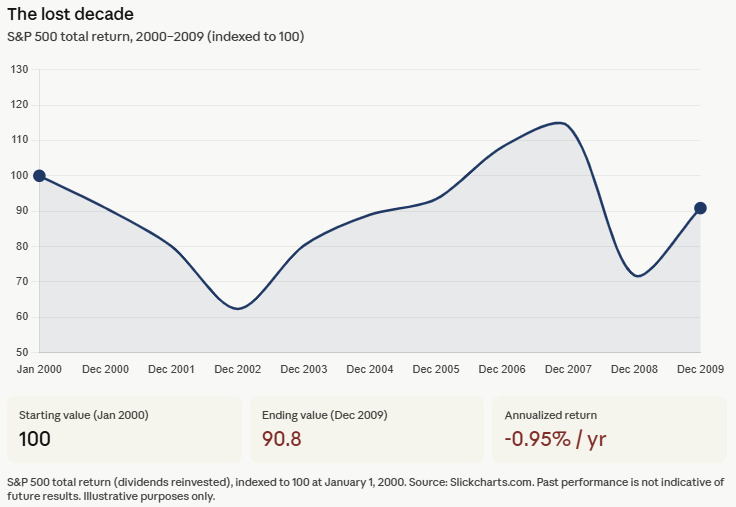

The most recent example of what happens when U.S. large caps hit a wall is the 2000s, a period frequently called the “lost decade” for U.S. investors. The S&P 500 ended 2009 at roughly the same level it started in 2000. Zero price growth across an entire decade. When you factor in inflation, meaning the rising cost of everything around you, investors who went all-in on the index lost real purchasing power over that stretch.

What happened? Two brutal crashes. The dot-com crash starting in 2000 wiped out a wave of massively overvalued technology companies. Then the financial crisis of 2008 hit. The S&P 500 dropped roughly 49% from peak to bottom in the first crash, and roughly 57% in the second. (To put that in perspective: a 49% drop means you need a roughly 98% gain just to get back to where you started. And that’s before the second crash hit.) Investors who had loaded up on U.S. large and mega-cap growth stocks heading into 2000 got hit especially hard, because those were the most overvalued sectors going in. Sound familiar?

Meanwhile, investors who held international developed markets and emerging market stocks fared considerably better. International developed markets outpaced the S&P 500 for much of the decade, and emerging markets, those of countries like Brazil, India, China, and South Korea, performed even more strongly during parts of that period.[2] The diversified investor wasn’t celebrating, but they weren’t devastated either.

This is not ancient history. Anyone who retired in 2000 with a portfolio concentrated in U.S. large caps experienced what’s called sequence-of-returns risk at its most punishing: they were pulling money out of a portfolio that was falling hard in the early years of their retirement, which may permanently affect long-term financial security. And they didn’t get a warning. Nobody does.

3. Japan: The Cautionary Tale That Never Gets Old

For those who think extreme single-country concentration is only a theoretical concern, I give you Japan.

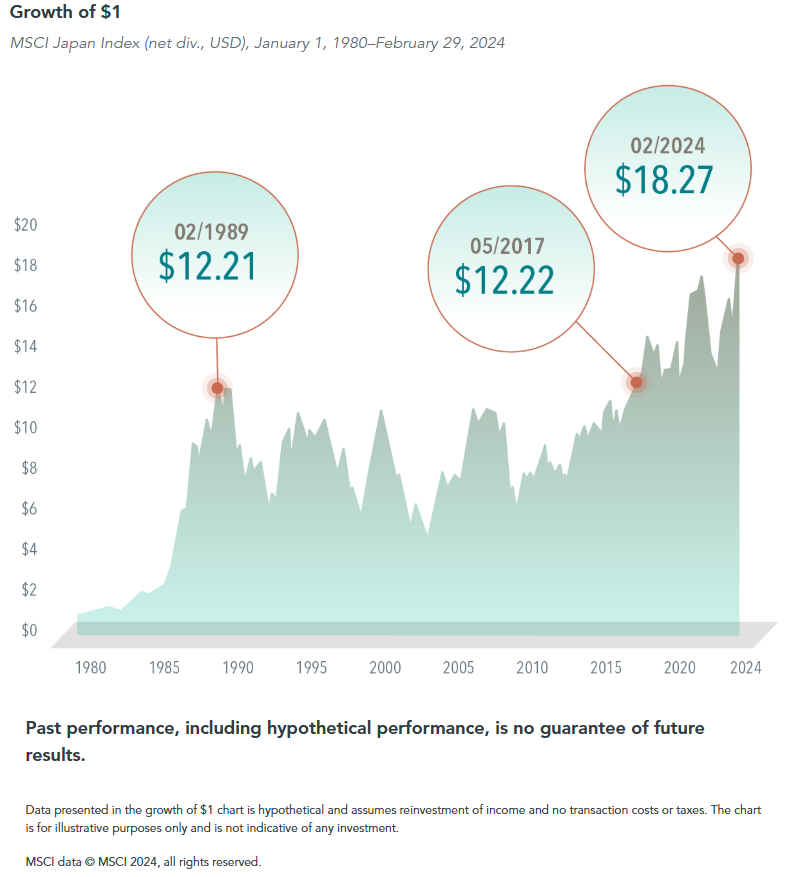

In the late 1980s, Japan was the investing world’s darling. Its economy had expanded at a remarkable pace for three decades. Japanese companies were buying American landmarks. The Nikkei 225, Japan’s rough equivalent of the S&P 500, gained more than 224% between 1985 and 1989 alone.[3] By late 1989, eight of the world’s top ten companies by market value were Japanese. Tokyo real estate had become so inflated that the grounds of the Imperial Palace were reportedly worth more than all of California. The general feeling, as one writer put it, was that the Japanese economic takeover of the world was inevitable.

You can probably guess where this is going.

The Nikkei peaked at 38,915 on December 29, 1989. It then fell nearly 80% from that peak over the following years and did not recover to that same level until 2024. That’s 34 years.[4] For most of that stretch, a Japanese investor who had put money into the Nikkei earned approximately 1.1% per year, and all of it came from dividends. The price of the index itself was essentially flat for three and a half decades.[5] Entire careers. Entire retirements. Flat.

The valuation context matters here. At the Nikkei’s 1989 peak, investors were paying roughly 60 to 70 times the annual earnings of those companies to own them. The global average at the time was around 15 to 16 times earnings.[6] Japanese stocks were priced at roughly four times what stocks elsewhere in the world cost, relative to what those companies actually earned. (Any of this sounding familiar yet?)

The lesson from Japan is not that this is likely to happen to the U.S. It is that it has happened, that it can happen, and that investors who assumed their home market was permanently exceptional paid an enormous price for that assumption.

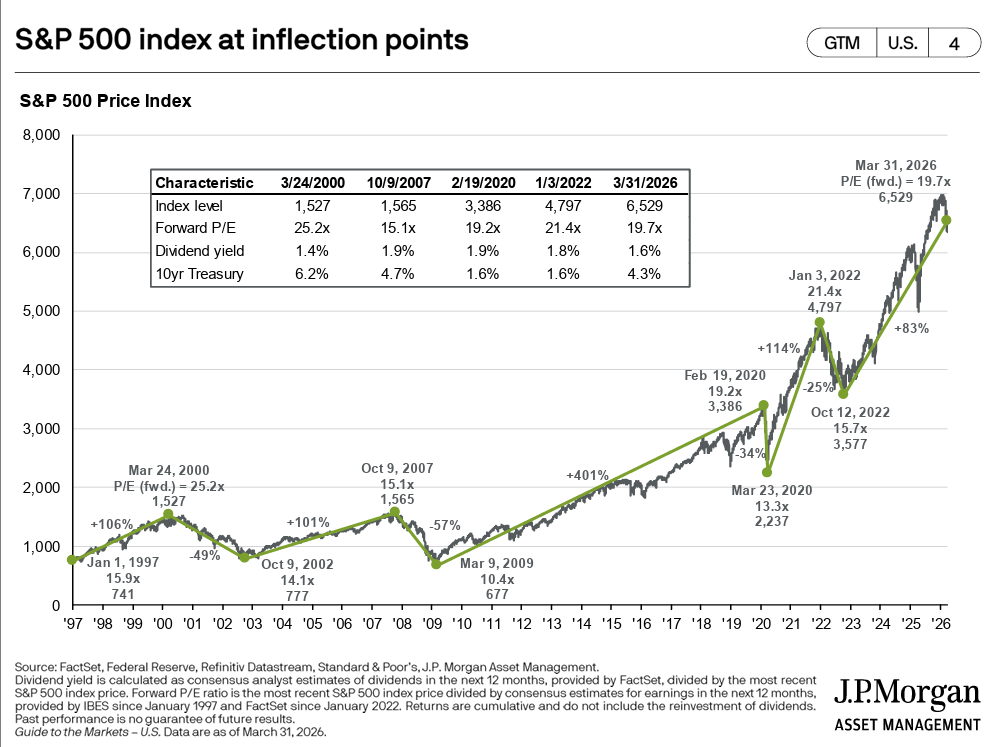

4. Current U.S. Valuations Are Not Exactly a Bargain

Speaking of how much investors are paying relative to what companies earn.

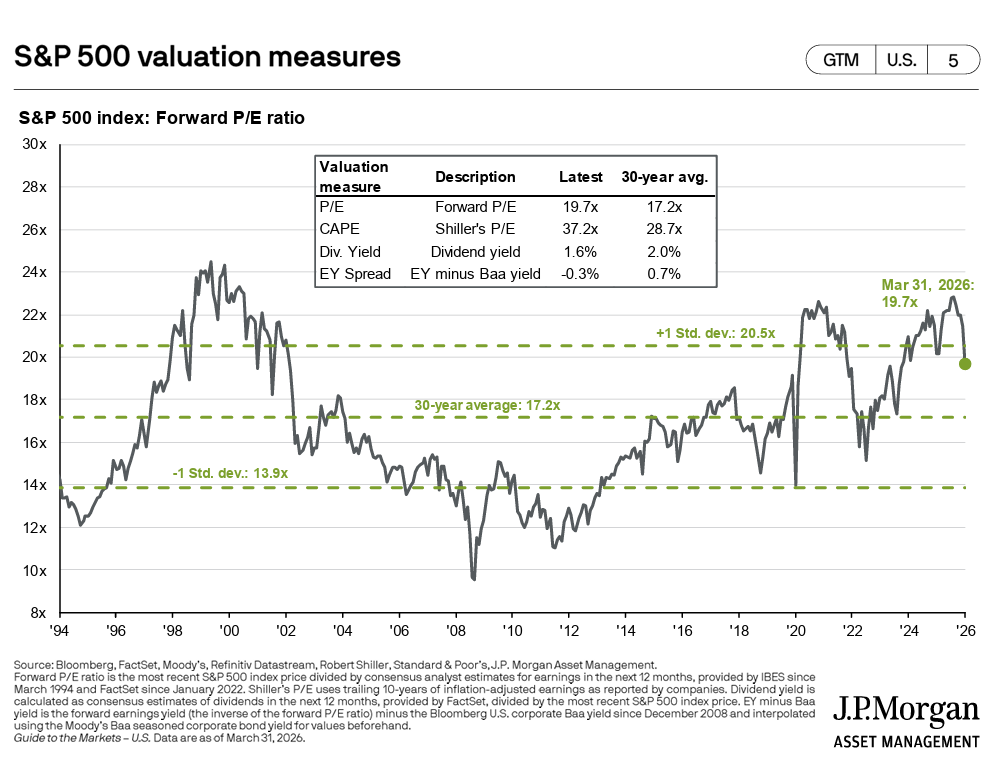

One of the most widely used long-term valuation measures is something called the Shiller CAPE ratio. (CAPE stands for Cyclically Adjusted Price-to-Earnings. It’s a mouthful, so most people just call it the CAPE.) Instead of just looking at one year of earnings, it averages ten years of inflation-adjusted earnings to smooth out the natural ups and downs of the business cycle. The idea is to get a cleaner read on whether stocks are historically expensive or cheap.

According to J.P. Morgan Asset Management’s Guide to the Markets, as of March 31, 2026, the S&P 500’s Shiller CAPE ratio sits at 37.2x. The 30-year average for that same measure is 28.7x.[7] In other words, by this measure the market is trading at a roughly 30% premium to its own three-decade norm. The forward P/E ratio, which looks at expected earnings over the next twelve months rather than a historical average, sits at 19.7x versus a 30-year average of 17.2x. It currently sits just below the upper one standard deviation band of 20.5x, and was recently above it.7 (That matters: the market has only spent a relatively small portion of the last 30 years above that line.)

To be clear: elevated valuations don’t predict exactly when things may change or by how much. They are notoriously poor short-term timing tools. But research spanning decades of market data suggests that starting valuations are among the stronger predictors of what returns may look like over the next ten years. Higher starting valuations have historically corresponded with more modest returns over the decade that followed.[8] (Not doom and gloom. Just math.)

And by comparison? International developed market stocks were trading at a roughly 40% discount to U.S. stocks at the end of 2024, when you look at the same valuation measures. International small-cap stocks were nearly 30% below their own 20-year average and at an all-time low valuation relative to U.S. large caps. Emerging market stocks sat at a steep discount too.[9] In other words: all of the asset classes that the VOO & Chill crowd tends to skip were, at this particular moment in time, considerably cheaper than what they were choosing to concentrate in. (Worth noting.)

5. You Are Leaving Real Return Drivers on the Table

Here’s something that often gets lost in the “just buy the S&P 500” conversation: the S&P 500 is not a neutral, comprehensive exposure to stocks. It’s a specific bet on large and mega-cap U.S. companies, heavily weighted toward technology and growth. By owning only that, you are actively excluding return drivers that decades of academic research suggest are real and persistent.

In 1992, economists Eugene Fama and Kenneth French published research showing that two additional characteristics beyond just “own stocks” explain a large chunk of why some portfolios have outperformed others over time.[10] The first is size: smaller companies have historically outperformed larger ones over long periods. The second is value: companies that are cheap relative to what they actually own or earn have historically outperformed more expensive, high-flying “growth” companies. Later research added a third factor, profitability: companies with strong, durable profits have tended to outperform weaker ones. (Fama won the Nobel Prize in Economics in 2013, partially for this work. It’s not a fringe idea.)

In plain English: history suggests that owning smaller, cheaper, more profitable companies alongside large ones has tended to produce stronger long-term results than owning only the biggest, most expensive ones. The S&P 500 is almost entirely the biggest, most expensive companies in one country. It’s roughly the opposite of what the research points toward.

The size premium, meaning the extra return small-cap stocks have historically delivered over large caps, has averaged roughly 1.5% to 3.5% per year going back to 1926 in U.S. data. The value premium has averaged roughly 3% to 5% per year.[11] These don’t show up every year. But over decades, they tend to compound. Ignoring them entirely isn’t a neutral choice. It’s a bet against them.

Dimensional Fund Advisors has built its entire investment approach around systematically tilting toward these kinds of companies, while staying broadly diversified. Over the 20 years ending December 31, 2022, more than 92% of their funds outperformed their benchmark indexes, compared to roughly 30% of the broader fund industry.[12] That difference is not a coincidence.

The investor concentrated entirely in U.S. large caps isn’t just ignoring other countries. They’re actively betting against decades of research by concentrating in the largest, most expensive companies in one market. (And the fee savings from skipping an advisor to get there don’t exactly cover that tradeoff.)

6. You Cannot Rebalance What You Do Not Have

One of the underrated advantages of holding multiple asset classes is what diversification lets you do during volatile markets: rebalance.

Rebalancing just means periodically trimming the parts of your portfolio that have grown and adding to the parts that have fallen. If your international stocks drop 20% while your U.S. stocks hold steady, rebalancing means shifting some money from U.S. stocks into international, buying more of what got cheaper. It sounds obvious. In practice, it’s psychologically brutal because it requires buying the thing that just fell, which feels terrible. That’s exactly why it tends to add value: most people won’t do it.

When international stocks were getting crushed in 2011 and 2012, an investor with a diversified portfolio could systematically shift money toward them at lower prices. When U.S. small caps lagged badly in the early 2000s, the diversified investor was buying them on sale. Both positions eventually recovered and then some.

An investor who only owns an S&P 500 fund has nothing to rebalance into. There’s no other bucket to draw from, and no underperforming asset class to add to at a discount. Every market swing is just a passive ride. You eliminate one of the few systematic, evidence-based advantages available to long-term investors. (And then potentially panic sell at the bottom. Which is its own expensive problem.)

The concept is simple: the less your asset classes move in lockstep with each other, the more rebalancing may benefit you. U.S. stocks, international stocks, small companies, value companies, and emerging markets each tend to respond differently to different economic environments. That’s a feature. Not a bug.

7. The “All You Need” Narrative Already Has Cracks in It

One of the most persistent arguments for the S&P 500-only approach is that it’s simply worked. And for the last 15 years, that’s been largely true. But zoom out even a little, and the narrative starts to look shakier than the Reddit threads suggest.