Surviving Your First Market Crash

Picture this: you’re young, living life, killing it at your first “adulting” job, putting those dollars away for retirement, finally making some good money, and then boom - the market crashes. Social media blows up, politics get even more heated, your invested savings drop lower and lower, and you can’t seem to escape the dark shadow of worry. Sound familiar? Well, hang in there, because you're about to get all the deets on how to survive your first market crash.

First, let’s start with the technical definition of a market crash. A market crash is when the market falls 20% or more from the very top. Crashes can take longer to recover from and may last years. They also are often accompanied by a recession and usually are a result of some systematic failure or other reasoning. Okay, so now you know how to identify a market crash. Now, let’s talk about how you can gear up and weather a storm when it comes.

Don’t Stop Investing

Wait, you’re telling me to continue putting my money into the thing that feels like it’s going to collapse at any second? Yep. If you’re a client of mine, you know we are all about the long-term mindset. Markets go up and down throughout your lifetime and you are feeling the pain of your first major market downturn. Pain isn’t easy. It stings. It can be lingering. But the amazing thing is pain can be healed and can go away with time. And guess what! You have the time. Retirement is more than likely 3 to 4 decades away for you. Market downturns are a part of investing and will happen again in your lifetime. Author, Carl Richards, puts it best in his sketch below. Days can feel painful, all over the place, and scary. But zoom out and take a look at the big picture.

By continuing to invest, you can take advantage of the market downturns and investments being less expensive. Not only that but get in on the downside and you are fully prepared to ride the wave back up when the time comes (aka you are making money). If you wait until the market is “looking good” again, you might miss the opportunity for growth. Now, I’m not saying to time the market. But what I am saying is investing at regular intervals regardless of the market performance is a healthy habit to have (dollar cost averaging, my friends).

Tune Out the Noise

Remember that pain I was talking about? You’re not the only one feeling it. So is your boss, your parents, your neighbor down the road, and your local grocery store. It’s everywhere when there is a market crash. So naturally, that is what’s going to be flooding your social media timelines. I’m here to tell you to shut it off. Tune out the noise of your Twitter’s worry and your Facebook’s advice. If you find yourself constantly logging into your IRA and 401k accounts to check the balance - don’t. Trust me, it will help you feel less of that temporary pain. From our previous conversation above, you know you have time. Focus on the decades, not the days. Temporarily unfollowing some select individuals and deleting your investment apps might just help you forget the pain is there.

Make Sure Your Financial Advisor is Doing Their Job

When you go through your first market crash, I want you to pay close attention to your advisor. I’m not talking about performance (because let’s be real, if the market crashed, more than likely your accounts will have dropped no matter who your advisor is). I want you to pay close attention to their communication and education. Are you hearing from them? Are they checking in and educating during a market crash? A good advisor communicates with their clients especially when the market is a little wobbly. If you are a client of mine, you know I send quarterly newsletters to educate you with what’s going on in the market. Not only that, but you can expect communication from me when turmoil in the market comes. How does your financial advisor communicate with you? Will they listen to your concerns? Will they educate and help set your focus on what matters? Remember - you hired them.

Crashes will be inevitable in your lifetime. Knowing what to do when they come will play a huge role in your long-term financial success. So keep making strides in your career and keep building up those savings. Pain is temporary and if you focus on the right things, the pain might just start to feel like opportunity. Gear up and don’t just survive in a market crash - thrive in it.

Fiduciary Financial Advisors, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Investments involve risk and are not guaranteed. Be sure to consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.

Here, at Fiduciary Financial Advisors, we take our fiduciary oath seriously. We hold these five principles:

I will always put your best interests first

I will avoid conflicts of interest

I will act with prudence; that is, with the skill, care, diligence, and good judgment of a professional

I will not mislead you, and I will provide conspicuous, full, and fair disclosure of all important facts.

I will fully disclose, and fairly manage, in your favor, any unavoidable conflicts

How to Beat Inflation

What is Inflation?

Recently, inflation has been a hot topic, but what exactly is inflation and why does it matter so much? Inflation is the rate of increase in prices over a given period of time caused by an increase in the money supply. Since this causes more money to chase after the same amount of goods and services in our economy, prices increase. Our money then has less purchasing power because we end up paying more for things than before. Inflation is not a new phenomenon, but it hasn’t been a big issue since the early 1980s.

If we look at the M2 money supply data below, which is how the Federal Reserve broadly measures the money supply, you will notice the large increase that happened during the COVID pandemic to try and help stimulate the economy. People can debate back and forth if that was the right or wrong thing for politicians and the Federal Reserve to do. I would like to instead focus on some practical tips to help weather the “inflation storm” and potentially come out on the other side unscathed or even better than before!

Have an Emergency Fund!

Having money sitting in an emergency fund is not the most exciting tip, and inflation will indeed decrease that purchasing power. However, the purpose of an emergency fund is not to make a high return. It is to have a liquid supply of money available in an emergency. Going without one could lead to more serious financial issues if something unexpected happens and you don’t have enough cash to cover it. Since the Federal Reserve has started to increase interest rates, we should see that translate into higher yields on savings accounts soon!

Typically, I’d recommend 3-6 months of living expenses in your emergency fund, but you may want more or less depending on your situation.

Are you single?

Do you have children?

Are you a one-income or two-income household?

Is your job in a high-demand sector?

Could you easily find another job quickly if needed?

These are some questions you should consider when deciding how much money you should keep in your emergency fund.

Own Assets!

Owning assets that produce income could help during high inflation and protect your purchasing power. As inflation increases, these income-producing assets should be able to increase their rates to help soften the blow felt by inflation. Real estate properties can command higher rents as inflation increases. If you can’t afford to purchase an entire property then REITs (Real Estate Investment Trusts) are the other potential option to gain access to that asset class with smaller capital amounts.

Owning businesses is similar. The money the business receives as income may become less valuable due to inflation. If the business can increase the prices charged for goods and services, then the greater amount of income could offset the money being worth less. If you can’t afford to purchase an entire business, then consider owning parts of businesses through stocks, mutual funds, or index funds.

Own Debt?

I wouldn’t encourage anyone to go out and accumulate more debt. If you already have a fixed low-interest debt such as a mortgage, it may make sense to delay paying it off early. If inflation remains high, the money you use to pay back that debt will be worth a lot less in the future than the money you originally received. Using that money to invest in other assets could be a much better option.

Review Your Expenses

With inflation running high, it’s the perfect time to look at your expenses. Review what you are spending your money on to figure out if it aligns with your long-term goals. Do you need five different streaming services? Is it time to stop eating out as often and start cooking more at home? Is it time to start carpooling to save on gas prices? Incorporating some of these ideas to help reduce your expenses is another potential way to decrease the effect felt by high inflation.

Invest in Yourself

I saved the best for last! Investing in yourself is one of the best ways to deal with inflation. Learn a new skill, read a new book, take a new class/certification program, and grow your knowledge base. By making yourself more marketable to your current/future employer and providing more value for them, you should be able to command a higher salary. That can help make inflation not sting quite as much. Even though things will cost you more, earning more money to help offset those costs can be a difference-maker.

James Clear, the author of Atomic Habits, shared a powerful principle: a 1% improvement every day leads to you being 37x better at the end of the year. And I’m confident you can get 1% better at something every day! Inflation does not prevent you from improving yourself.

“Whatever abilities you have can’t be taken away from you. They can’t actually be inflated away from you. The best investment by far is anything that develops yourself, and it’s not taxed at all.”

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

Is it too late to start living like a Millionaire?

Do you want to become a millionaire? Do you want to live like a millionaire? It might not be what you envision. One author spent over a decade researching, investigating, and interviewing millionaires to explore how the average millionaire lives. Here are his insights from Thomas Stanley’s book, The Millionaire Next Door.

They live well below their means

The average millionaire doesn’t spend more than they earn. They don't buy fancy clothes; they shop for clothes at places like Target, Meijer, and Wal-Mart. They don't drive fancy car brands like Porsche, Ferrari, and Lamborghini. They drive cars made by Toyota, Honda, and General Motors. They don't live in mansions overlooking the ocean. They live in a well-taken-care-of home next door to you, which explains the title of the book.

True millionaires allocate their time, energy, and money efficiently, in ways conducive to building wealth.

The average millionaire is productive with their time. They spend much more time reading and much less time watching TV than non-millionaires. They don’t waste their money on lottery tickets or get-rich-quick schemes, hoping to become rich. They invest their time and money in improving themselves, learning new skills, starting businesses, and networking with other successful people. They exercise more and eat healthier. They start investing in their tax-advantaged accounts early!

They believe that financial independence is more important than displaying a high social status.

The average millionaire understands that being wealthy isn’t about showing off or one-upping their neighbor. Instead of buying a bigger house or fancier car, they would rather build wealth. They understand that building wealth allows them to gain back control of their time. Being financially independent allows them to spend more time with their family, volunteer more, work at a job they enjoy, and participate in hobbies they love. They understand the difference between appearing rich and being wealthy.

Their parents did not provide economic outpatient care.

The average millionaire did not inherit their wealth as many people assume. While some families do pass down wealth from generation to generation, research shows that the vast majority of millionaires are self-made. They did not receive large inheritances but built their wealth slowly over time.

Their adult children are economically self-sufficient.

The average millionaire is not supporting their adult children. They taught their children the principles of finance, which include delayed gratification and the power of compounding interest. They discussed their family finances early and often. They provided for their children's needs but did not fulfill every want. They taught them to work hard and to work smart. They taught them how to make their money work for them instead of the other way around.

They are proficient in targeting market opportunities.

The average millionaire learns that money is a medium for transferring value. If they provide a product or service to somebody, they receive money, which can then be spent to receive a product or service back. They use this information to stay on the lookout for opportunities where there is a lack of products or services. Then they use their knowledge and resources to provide that need which is in high demand. Improving efficiency is another value-add opportunity the millionaires use to generate wealth. Money flows to wherever value is created.

They chose the right occupation.

The average millionaire has found an occupation that matches their skill set and personality well. They enjoy going to work most days and look forward to being productive. Enjoying their job allows them to excel, which leads to being compensated well.

I encourage you to start implementing these insights in your life. If you enjoyed this overview, I would highly recommend reading the book!

“You will be the same person in five years as you are today except for the people you meet and the books you read”

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

What is a SEP IRA?

A SEP IRA is a great long-term savings vehicle designed for any employer, including self-employed individuals. There are some important factors to know when it comes to deciding if a SEP IRA is right for you and your business.

Want to know more? Click below to be instantly educated on SEP IRAs.

If the stock market is crashing! What should I do?

One of the most important rules when it comes to investing is to buy low and sell high. And yet, some people end up getting nervous when the stock market is “crashing” and end up selling low. Then, after the market recovers, they regain confidence and end up buying high. Letting one’s emotions control investing decisions is a recipe for poor returns.

You may see on the news or social media people claim that they know what the market is going to do in the future. Often people say these things to try and get more viewership and clicks instead of trying to give sound financial advice. But recall the adage that “even a broken clock is right twice a day”. Don’t be surprised when someone’s lucky guess happens to be accurate from time to time. Instead, focus on taking financial advice from a fiduciary, someone who is legally required to act in your best interest and not their own.

So what should you do during a volatile market? Without knowing the details of your financial situation, I can’t provide specific advice. However, I would like to review some data from the past to help you gain a better understanding of the markets and consider a “market crash” as a potential opportunity to buy. This is looking back at previous returns so make sure to note that past performance is no guarantee of future results.

In the world of finance, there are two different types of markets: a bull market and a bear market. A bull market is a time frame when the economy is expanding and stock prices are increasing, while a bear market is when the economy is experiencing a recession and stock prices are decreasing. As you can see from the chart below, bull markets typically last longer than bear markets and produce greater returns compared to the losses of a bear market. The U.S. has been in a bull market for a while so when it transitions to a bear market or recession that will not be out of the norm when looking back in history.

Since bull markets typically last longer than bear markets, the odds that someone makes money investing in the stock market could increase significantly the longer they leave their money invested. The chart below shows the probability of someone having positive returns investing in the S&P 500 index since 1937. If someone only invested for 1 day they had a 53.4% probability of having positive returns but if they stayed invested for 10 years they had a 97.3% probability of having positive returns! I prefer the much higher probability of higher returns by not trying to time the market.

The chart below shows the 15 largest single-day percentage losses for the S&P 500 since 1960. If you look at the right side you will see in the one year later column that only one time was the market negative one year post the corresponding single-day percentage loss. That was back in 2008 during the global financial crisis. Instead of becoming nervous about large single-day losses reassure yourself that more than likely the market will recover within one year.

Think about it this way, I LOVE Heath candy bars for obvious reasons. If I bought them as a snack and then Meijer sent me a coupon for 50% off, I wouldn’t get upset that I had just paid full price. I’d go and buy more. Selling stock when the market plummets would be a lot like me selling my Heath candy bars for 50% less than what I paid for them vs. buying more at such a great price!

Hopefully, this has helped you gain a better perspective on making investing decisions. I believe that having a longer-term outlook can help you keep emotions in check and not get as nervous/scared when you see people on the news and social media talking about a stock market crash.

Just like gym workouts are more productive with a trainer, folks often are better able to keep their emotions in check by having a talented financial advisor on their team. If you don’t have a financial plan established now might be as good of a time as any to get that put in place. I would be happy to meet with you to discuss your financial plan.

“We simply attempt to be fearful when others are greedy and to be greedy when others are fearful”

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

Traditional vs Roth Retirement Account, Which Is Better?

What is the difference between a traditional account and a Roth account? Which one is better for you? Which one should you invest in? Several factors can affect your decision. I will help you explore concepts to think about to assist when making that decision.

The main difference between a traditional account and a Roth account is the timing of when you pay taxes on the money. When you make a contribution to a traditional account you normally would be able to deduct that amount from your taxable income, which would reduce your taxable income the year you make the contribution. Then at retirement when you withdraw the money, you would pay taxes on the contributions and growth of the account. This is called tax-deferred money since you are deferring the taxes until later

A Roth account works the opposite way. You do not reduce your taxable income the year you contribute the money, but then when you withdraw the money you do not have to pay taxes since you already paid them on the money contributed. This is called tax-free money since it is tax-free upon withdrawal.

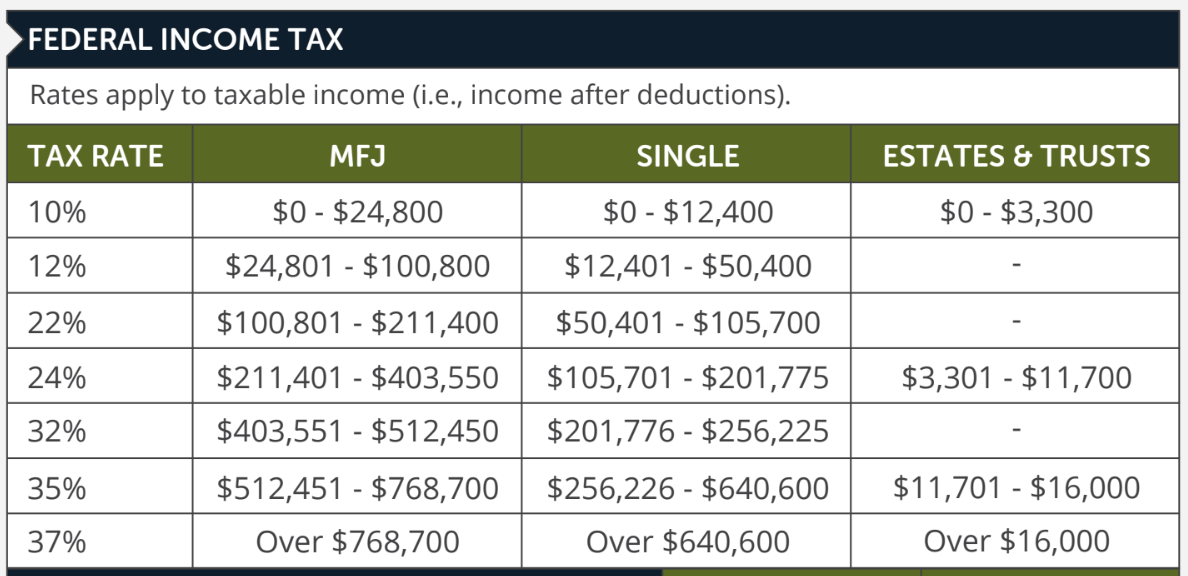

2026 Income Tax Brackets

One of the first things you will want to figure out is what federal income tax bracket you will be in for the current tax year. This is an important part of your decision when deciding if you should contribute to a traditional or a Roth account. Here are the federal income tax brackets for 2026.

If you are in one of the higher income tax brackets (32%, 35%, or 37%) it may make sense to contribute to a traditional instead of a Roth account since you would save more now on taxes than you would if you were in one of the lower income tax brackets (10%, 12%, 22%). If you think you are in a higher tax bracket now and will be in a lower tax bracket at retirement, then it may make sense to contribute to a traditional instead of a Roth account. Keep in mind that politicians have adjusted the tax brackets many times in the past and will probably adjust them again before you reach retirement.

Time Horizon

Time until retirement is another factor to consider when making your decision. Generally, someone who is younger will have a lot more time for their money to earn compound interest and could be better off contributing to a Roth account. This way all of the principal & compound interest they withdraw at retirement would be tax-free, whereas if it was in a traditional account you would owe taxes on that money instead. My brother explains it as “would you rather pay taxes on the seeds or pay taxes on the entire tree once it is fully grown.”

You might be someone who would rather lock in their tax rate now and not have to worry about if it will be higher or lower at retirement. If you are that type of person then you will want to consider contributing to a Roth account. If you are someone who believes your tax rate at retirement will be lower than what it is currently, then you will want to consider contributing to a traditional account.

Required Minimum Distributions

Required Minimum Distributions (RMDs) are another reason why you might decide to contribute to a Roth instead of a traditional account. After a certain age (as of 2022 it is 72) the government requires that you withdraw a specified amount of money every year from your accounts as they want to get their tax money back on that tax-deferred money. If you have that money in a Roth IRA then there are no RMDs, unless it is an inherited Roth IRA. (Source; Fidelity; link below)

Employer Plans

If you participate in a retirement plan at work, most companies offer some type of matching program. If you contribute a certain amount they will contribute a match. Dollar on the dollar or fifty cents on the dollar up to a certain amount appears to be the most common matching contributions. More employers are now offering a Roth option. If you elect to have your contributions go toward the Roth bucket be aware that your employer will more than likely contribute their match into the traditional bucket, so they are able to receive the tax deduction. This may be a good thing as it could help you diversify your risk by having some money tax-deferred and some money tax-free at retirement.

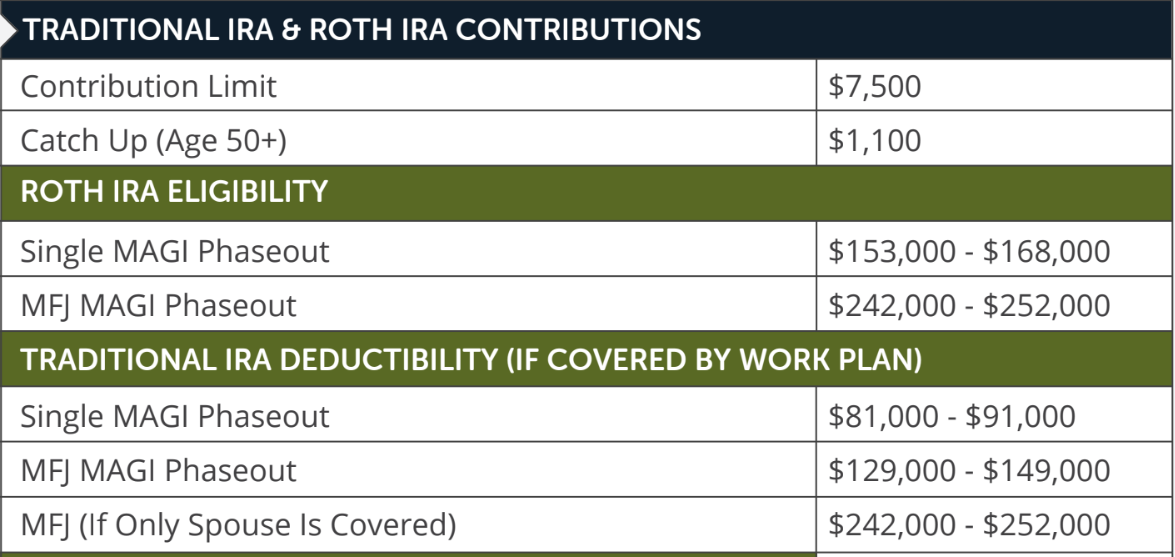

If you are a participant in an employer-sponsored retirement plan at work, then there is a deductibility phase-out for IRAs if your modified adjusted gross income (MAGI) is above a certain amount. In other words, you wouldn’t get the tax deduction by contributing to a traditional IRA plan if your income is over a certain amount and you have a retirement plan at work. For Roth IRA’s there is a phase-out limit. As your MAGI increases, the amount the IRS allows you to contribute decreases until you are no longer allowed to contribute. Here are the limits for the 2026 tax year.

If you have more questions about if you should contribute to a Roth or a traditional account feel free to set up a meeting with me as I am happy to discuss strategies personalized to your situation. If you are looking for the best of both traditional and Roth accounts then click here to learn more about how Health Savings Accounts can be used as a stealth retirement account.

Sources: https://www.kiplinger.com/retirement/retirement-plans/roth-iras

https://www.fidelity.com/building-savings/learn-about-iras/required-minimum-distributions/overview

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

What Should I Do With A Large Lump Sum Of Money

Did you just win the lottery, receive a large inheritance, or win a lawsuit settlement? If you just won the lottery I would recommend being wise with that money since 70% of lotto winners lose or spend all their money in five years or less (Source: Reader’s Digest; link below). Being smart with an inheritance or lawsuit settlement is just as important. Here are some steps you may want to consider when deciding what to do with your newfound wealth.

Don’t Do Anything

You might want to buy a fancy new car, go on an expensive vacation, or be generous by sharing the money with friends and family. There will be plenty of time for those things, but you should take a month to let everything settle first. Carefully consider who you are going to tell about the money. Don’t quit your job. Don’t go around bragging or posting about it on social media. Don’t put all of it into the hot stock of the month based on a Reddit forum. Continue living your life as if you never received the money. You will make better decisions once your endorphin levels have settled back to baseline.

Contact a Certified Public Accountant (CPA)

The IRS loves when people receive large sums of money, and you can bet that they want a piece of the pie. Often, that piece ends up being much larger than you’d prefer, so finding a CPA that specializes in taxes should be a top priority. They could help you strategize a plan to reduce the tax burden and leave more money available for other things.

Contact an Attorney

An attorney is able to explain the benefits of having a will, a trust, and a DPOA for finances & healthcare. They should be able to help you complete these if needed for your particular situation. If you already have these in place, this might be a great time to review and update any if needed. Having these in place will save your family many headaches when you eventually pass away.

Contact a Financial Advisor

A financial advisor is able to help create a written plan for your money. This could include paying off high-interest debt, opening and/or maxing out retirement accounts, funding a brokerage account, evaluating the need for term life insurance, building out a net worth statement, starting a donor-advised fund, and determining your risk tolerance to create your ideal asset allocation. When searching for a financial advisor you want to make sure they:

Are a Fiduciary: Which means they have to put your best interests first!

Are a Fee-Only Advisor: This means they do not have a conflict of interest with potentially selling you certain investments to get a large commission.

Have a Clear Investment Strategy: Do they have an investment strategy that can be clearly explained to you and matches your investment philosophy?

I am proud to say that I check all 3 of these boxes in my financial advising practice.

Implement Your Plan

While creating your financial plan might sound like the hardest part, implementing your plan may be more difficult. A written financial plan of how you want to direct your money is great but if you don’t take steps to implement that plan then it was all for nothing. When implementing your plan keep in mind:

Not to let emotions control your financial decisions.

Don’t let the news media tempt you into making quick, spur-of-the-moment decisions during periods of market volatility (Remember the main goal of news media is to attract viewers, not to give solid financial advice).

Stay consistent and reach out for help if needed. Investing is a marathon, not a sprint.

A patient going for physical therapy could perform all their therapy on their own if they knew the correct exercises. Having a physical therapist guide which exercises will be the most effective and support/encourage the patient in completing them, could help the outcome tremendously. Partnering with an excellent financial advisor is similar.

Finally, Treat Yo Self!

If you have made it to this point and are implementing a well-thought-out financial plan, you should congratulate yourself. You did the hard work and made the tough decisions to set yourself up for success. Now might be the time for you to use a small portion of that money to Treat Yo Self as a reward!

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

The Stealth Retirement Account That Most Americans Don't Use

Are you trying to find more ways to save for retirement so you will be able to retire early? Let me explain how you can use a Health Savings Account (HSA) as a stealth retirement account by investing inside of it. Currently, only 4% of Americans who have HSAs unlock this powerful potential. (Source: Devenir 2019 study; link below)

First, you have to be covered under a High-Deductible Health Plan (HDHP) before you are allowed to contribute to an HSA. If you are covered under an HDHP, the maximum you are allowed to contribute in 2026 is $4,400/single or $8,750/family (an additional $1,000 if you are over 55 years old). You do not pay taxes on money contributed to your HSA, and if the money is withdrawn for eligible healthcare expenses, the funds are not subject to any penalty or taxes. Most people use their HSAs this way. The money goes in…then it comes right back out to pay for medical expenses. This is a great way to save money on taxes for eligible healthcare expenses, but it is not utilizing the full potential of your HSA.

With a few simple adjustments, you could turn your HSA into a stealth retirement account.

Pay Out-of-pocket for Medical Expenses

This allows you to accumulate more money inside your HSA every year instead of depleting the account every time you have an eligible medical expense. The longer you are able to keep the money in your HSA, the more time you are able to let it grow and compound.

Save your Eligible Healthcare Receipts

If you choose to use your HSA as a stealth retirement account, make sure you save your eligible healthcare receipts. This would then allow you to withdraw money from your HSA to reimburse yourself for the past eligible medical expenses that you paid out-of-pocket earlier. Currently, the IRS doesn't have a time frame for when you are allowed to reimburse yourself. This means you could spend $500 out-of-pocket today and submit it for reimbursement years later. The medical expenses have to have occurred while you were covered under an HDHP though!

Invest the Money

Investing your HSA money could allow it to grow into a significant amount, depending on what the time frame is and what return percentage you are able to achieve. Below are examples of someone investing their HSA money for 30 years with an annual return of 7%. Your numbers will be different depending on the length of investment and returns. (Source: Calculator.net; link below)

“Because of the effects of inflation, a 50-year-old couple in 2019 planning to retire at age 65 can expect to spend about $405,000 on health care in retirement. A 40-year-old couple faces $455,000 in expenses...” (Source: Annuity.org; link below)

These three things would allow someone to take full advantage of using their HSA as a stealth retirement account. HSAs allow investing in a triple tax advantage account. The money contributed reduces your taxable income while the qualified withdrawals and investment growth are tax-free. If the withdrawals are not qualified, this becomes tax-deferred growth.

Other Things to Consider

If you withdraw money from your HSA for non-medical expenses, you have to pay taxes and a 20% penalty. After you turn 65, the 20% penalty goes away. This allows you to optimize your tax efficiency by choosing which accounts to withdraw money from instead of having to fully depend on Social Security and Medicare. Additionally, most investors are in a lower tax bracket in retirement since they are no longer working, so there may even be another benefit to delaying the tax until later in life.

Not all HSAs are equal. Some charge high fees, some limit the amount of money you can invest, some limit your investment options, and others don’t allow investing at all. Your employer usually chooses which institution they use for HSA contributions, but once the money is in the account, you have full control of what happens with the money. Check to make sure it is a good one. If not, you may be able to move your HSA money to a better institution. If you would like assistance in moving over your HSA, deciding what investment options to invest in inside your HSA, or any other HSA-related questions, contact me and I would be happy to help.

Sources:

https://www.devenir.com/research/2019-midyear-devenir-hsa-research-report/

https://www.calculator.net/future-value-calculator.html

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

Intro to Planning for Widows

Some of my most meaningful client relationships have been with widows. There are many reasons behind this, but widows face a different set of circumstances than couples do.

Whether a recent widow or a soon-to-be widow, a partnership has or is in the process of ending. You may have made financial decisions with your spouse or maybe these decisions were made separately, but now you are forced to make these decisions on your own. In a best-case scenario, you already have a good relationship with a financial advisor. But if not, you should look for someone who has been down this path before and understands what you are facing. You have so many decisions to make with a new set of facts and having the right financial team in place could really reduce the stress of these decisions.

With so many financial decisions looming, the list of considerations can be daunting. Income taxes, estate planning, investment advice, cash flow planning, long term care planning, electing Social Security…Any of these on their own is difficult. But so many of these are interrelated and one decision in one area has impacts in others as well.

Many people don’t NEED someone else to help them make a decision, but they prefer to have someone to work with through tough decisions. When the decisions are now all in your hands, this may seem off and you may want to bounce your thoughts and ideas off someone else before making the final choices.

When you are overwhelmed, it is more difficult to make tough decisions. Having an experienced advisor on your side can make the mountain of choices seem much more manageable. Not all decisions have to be made immediately and a professional can help you prioritize. Often, we make a list of what needs to be addressed with a corresponding timeline for each item.

The fog will eventually lift, but the decisions you make in the meantime are incredibly important. With so many different thoughts coming your way and a range of emotions, it pays to have a reliable partner to guide you through this period and beyond.

FOYER CHATS PODCAST // Financial Planning for Your Business AND Your Life with Leanne Rahn

Financial Planning for Your Business AND Your Life with Leanne Rahn

Episode Description

Today's episode we chat with Leanne Rahn - a fiduciary financial advisor specializing in helping new business owners and newlyweds! What is a fiduciary you ask?! Well we will ask that question for you ;). Leanne shares all about financial planning for your business AND your life. Take away tactical tips and tools to create a killer financial plan JUST RIGHT FOR YOU! Leanne makes talking about organizing the back end of your business and setting those big financial goals SO much fun, we already know you'll love her!

3 Reasons Business Owners Should Consider Rolling Over Their 401k to an IRA

So you took the leap and started a business. Whether that was recently or years ago, to you I say congrats! What an accomplishment to leave your old employer to begin a passion-driven career that you design. With all the excitement your new business brings, it can be easy to forget about that old 401k you had with your previous employer. Here are three reasons why you should consider rolling over your 401k to an IRA:

More Investment Options

Typically, 401ks have a set list of investment options you can choose from. This limits you to what’s on the paper in front of you. Yes, there is a chance you could have a great list of investment options, but there is a chance it could be the other way around too.

IRAs open up many other investment opportunities. Instead of potentially only having a few mutual fund options, you can choose from a variety of different mutual funds, ETFs, individual stock, bonds, and more. IRAs have more choices to fit a whole range of different needs. Who doesn’t love more customization?

Lower Fees

With more choices, may come lower fees. Management fees, administrative fees, and fund expense ratios can have a big impact on your retirement savings. This will look different for every 401k plan, but it is worth looking into.

If your plan has costly mutual fund options, IRAs could open a door to potential savings by choosing lower-cost investments. By rolling your old employer plan over to an IRA, you could be getting more money back in your pocket come retirement.

Better Communication

Your old 401k may be sitting at an investment firm that may have long hold times, poor communication, and more pains in your side. It may be harder to get information on your plan than if you were a current employee.

With an IRA and working with a Fiduciary Financial Advisor, you can have direct access to me and the company your IRA is held at. Instead of being an old employee, you are my client - a relationship I take seriously. No long hold times or lack of communication. Instead, one-on-one communication, questions answered, and your best interests first.

Don’t let your old 401k be a nagging concern as you continue to drive a pathway in your business. Let’s look at your old 401k together and figure out the best option for you. More investment options, lower fees, and better communication may be in your future. Sounds like a pretty good future to me.

Here, at Fiduciary Financial Advisors, we take our fiduciary oath seriously. We hold these five principles:

I will always put your best interests first

I will avoid conflicts of interest

I will act with prudence; that is, with the skill, care, diligence, and good judgment of a professional

I will not mislead you, and I will provide conspicuous, full, and fair disclosure of all important facts.

I will fully disclose, and fairly manage, in your favor, any unavoidable conflicts

Action Point Financial Planning, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Investments involve risk and are not guaranteed. Be sure to consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.