How to Save Money on Your Next Family Vacation

Tips to maximize your vacation savings, destination advice, flight deals, and more!

This month, I had the opportunity to sit down, interview-style, with Travel Advisor, Sarah Allen, and get all the secrets on how to save money on your next family vacation. She shares some amaaazzing tips that will help you decide how to choose your destination, the best way to book flights, how timing can play an impact, and more. Keep reading and by the end of this, you’ll be packing your bags!

//

L: Sarah - how in the world does a travel addict decide on their destination? Give us all the tips!

S: There are a few things to consider when choosing a travel destination. Time of year and weather may help guide your decision. Would it be too hot to enjoy hiking in Sedona in July? Christmas at Disney is beautiful but it will be very busy so if you don’t like crowds you should go during an off-season time.

You should also consider the age of your children. Are they too young for long hikes? Would they enjoy the museums in a large city? I suggest making a bucket list of all the trips you’d like to take. Then decide how much money you have to put towards travel each year.

Next, plot these ideas in a calendar based upon your budget and life stage.

L: Okay, so once a destination is decided, how far in advance should someone start planning?

S: It really depends on where you are going, how flexible your dates are, and if you need time to save up for your trip. Cruise lines and major theme parks release dates over a year ahead of time and if you book when those dates are released you will have the best chance of booking the resort and room category you are looking for. Prices will likely be the lowest when dates are released and a good Travel Agent will watch for promotions that can be applied to your stay if money can be saved.

If you are traveling at a busy time of year like Christmas or Spring break or even summer break I would suggest booking at least 6 months ahead of time. Trips can be booked last minute but there may not be as many choices if you wait too long.

I have always enjoyed the anticipation of the trip almost as much as the trip itself so we tend to book early. This gives us plenty of time to save up the money we need and plan all of the details!

L: Let’s talk about the specifics: what are the benefits of booking your trip early? Would there ever be a benefit to booking late?

S: There are benefits to booking your trips early. You will have the most choices for accommodations and room categories if you book when dates are released. It is also a great way to save money on trips to places like Disney, Universal, and for cruises. If you book when dates are released you will likely get the best price available. If you use a Travel Agent they will watch for promotions that might save you money and can call in and modify your reservation for you at any time. Booking early also gives you time to save up for your trip, do your research, and anticipate all the fun you will have.

Conversely, you can sometimes find an amazing deal last minute. These don’t leave a lot of time for planning or saving money but if your life situation allows you to pick up and go at any moment it is definitely a budget-friendly way to travel.

L: Speaking of timing, are there certain times of the week or year to avoid OR take advantage of when it comes to airfare? Other secrets on how someone can save dollars on flights?

S: There are a couple of ways to save money on flights. Airlines generally release their flights about 6 months before your trip. I start off looking at sites like Kayak and Google flights to get an idea of what is available and then to the Hopper app to see the best time to book. Setting an alert on these services will let you know when prices drop.

If your dates are flexible you could also use a flexible date search tool and easily find the cheapest days to fly out.

My last tip is to look at all of the area airports. You might be able to fly out of a smaller airport nearby for less money or on a more convenient day. When it comes to booking the flight I suggest to do so directly with the airline.

L: Are there pros and/or cons to using booking sites like Kayak, Expedia, etc.?

S: I love using sites like Expedia and Kayak for research and sometimes they can save you money. It’s a great tool to get an idea of what hotels are available and I love the map feature! With a quick glance, you can discern the hotels with the locations you desire.

There are a few downsides. Often the rates on their hotel rooms are non-refundable. If I learned anything in the last 2 years it's that things don’t always go as planned and lately I am much more comfortable booking a room that I can cancel. Weigh your options and definitely check the cost of booking directly with hotels for the most flexibility.

If you book a flight with any of these third-party sites it is much more complicated to reschedule a canceled or delayed flight. When there is bad weather or staffing issues and 1000’s of people need to rebook, the airlines will rebook the customers who booked directly with them first. This could leave you stuck at an airport longer.

In this current climate, I suggest booking directly with the vendor.

L: What about travel insurance? Do you typically recommend this to your clients?

S: This is a timely question. Pre-covid, my family rarely thought about purchasing travel insurance. Life was fairly predictable and canceling a trip just wasn’t something you heard about very often. Since covid, my family has had to cancel or reschedule a number of trips. Some we had travel insurance for and some we did not.

I am not an insurance agent so my advice before buying a policy would be to read through the details closely. What does it cover? Consider the cancellation policy where you are going before purchasing additional insurance. If they will let you reschedule for another time, maybe you don’t need travel insurance.

Another thing to think about when buying travel insurance is your health and healthcare coverage. Are you older and traveling abroad? Maybe it would be a good idea to get a plan that would cover an unforeseen medical emergency.

L: Cruise vacations are all the hype. Is there value in them? Why would someone choose a cruise for their next vacay?

S: Cruising is a great option for families, couples, or singles to see and experience different cultures from the comfort and elegance of a massive ship. These boats are floating cities with luxurious amenities. The best thing about a cruise is that food and entertainment are included in the price of the cruise and both will be top-notch.

We went on our first cruise after renting a beach house for spring break. Shopping for and cooking 3 meals a day for my family wasn’t quite the vacation I had in mind. Sitting on the beach and watching ship after ship left got us thinking about other ways to vacation. We were surprised at how affordable a cruise was and no cooking!

Drink packages and excursion options will be an additional cost but you could stick to free beverages or you can stay on the ship and enjoy a quiet day to save money. Many ships also offer kids’ clubs and fun activities which will give parents some time to relax kid-free.

L: Okay, SUCH good info on cruises. What about another popular vacation destination - Orlando theme parks? Share with us your top budget-friendly tips!

S: 1. I had a friend help me plan our family’s very first trip to Disney World. I had been many times as a child but my family always stayed nearby with my grandparents and we only did one park per trip. I really didn’t think we could afford to stay on the property for a week. Then she told me about Disney’s value resorts! I had no idea we could stay at a Disney World property for those prices. The value resorts at Disney are not fancy but they are clean and have very fun theming.

2. When we travel to Disney or Universal we always bring simple breakfast foods with us or order groceries to be delivered to our resort. Having a quick, simple breakfast in our rooms saves us money and time. The resorts do have breakfast options available but it is often crowded and the cost of that for a family definitely adds up.

3. Brunch for lunch is a great way to save money on a more expensive meal like character dining. Sometimes we will book a reservation for a late breakfast and consider that our lunch and sit-down meal for the day, choosing a less expensive option for dinner.

4. It’s important to stay hydrated in the Florida sun but buying bottled water in the parks is expensive. Bringing in your own water bottles can save you money. I love the stainless steel Brita filter water bottle because you can fill it with ice and then water from any sink. You can also ask for free water at any quick service or snack location.

5. Souvenirs - set a budget ahead of time and communicate that plan to your kids or let them pick one thing in the parks. Have them save their money ahead of time for other things they may want while you are away. It’s good for your kids to learn the value of money and planning at a young age.

6. Purchase things ahead of time - PLAN AHEAD! Things like ponchos and sunscreen are expensive in the parks. We also buy themed shirts at Target, Kohls, or Amazon for our trip versus in the park.

7. Chase Disney Visa - we have had this card for years and earned 1000’s of Disney dollars to spend in the park. You can also use points toward flights. We have all of our recurring bills on this card and charge all of our purchases throughout the month. Please only consider this option if you plan on paying your full balance each month.

8. Disney gift cards - You can purchase packs of Disney gift cards at warehouse clubs like Sam’s and Costco. This is a great way to save up for your trip as you can use them to pay your balance or in the parks for food and souvenirs. Buying a pack or two a month will ensure you don’t spend that cash on other items. They will usually go on sale around Black Friday and you will be able to purchase them for less than their face value.

L: I’m taking notes! So good. Alright, Sarah, if you had to leave the readers with your TOP 3 tips on how to save money on their next family vacation, what would they be?

S: Number one: Book early with a Travel Agent - not only will you likely get the best price your agent will watch to see if there are any sales and can apply the sale price to your trip. This also gives you lots of time to save and anticipate!

Number two: Travel in the off-season - if you choose to go to Florida in September right after school starts or January when it may be cooler you will find the off-season rates apply. It will also be less busy.

Number three: Drive to your destination if it’s close enough and time allows. Buying airfare for our family of 5 adds up quickly. We look forward to our drive each spring break and even with gas, food, and a hotel stop we still end up saving about $1000 plus then we don’t need a rental car when we get there. A bonus is your kids get to see a lot of places while you are on the road.

L: Last but not least, Sarah: If someone wants to work with you, what does that look like? How can you help them plan their dream vacation?

S: I specialize in Disney trips, Universal trips, cruises, and all-inclusive resorts and have completed certification in each of these areas of expertise. When you book a trip with Fairytale Journeys by Sarah Allen you get my years of experience, planning, services, and support for free. Travel agents are compensated through commissions that hospitality companies include in their packages whether you use a travel agent or not.

We will start the process by talking about what you want your vacation to be like and then I will curate a trip just for you based upon your family's unique budget, wants, and needs. My job is to wade through all of the options, availability, dates, and insider knowledge and present you with choices that work best for you and your family.

Once the trip is booked I help families with the details of the trip, such as transportation, dining plans, theme park information, things to bring, etc. I’ve spent years acquiring this information through travel and research so you don’t have to! Things don’t always go as planned and when you need help on a trip it’s nice to know you have a friend and expert available to help!

Time is money and using a travel agent will not only save you time it will save you from being overwhelmed and frustrated.

//

Tips from Leanne:

Check out the latest travel credit cards. Many companies offer incentives for opening a new credit card that could earn you free flights, money off your travels, cashback on gas, and more! Utilize credit wisely by not spending what you don’t have. Bonuses and freebies are great but what’s even better is not getting crushed by the weight of credit card debt.

Another great way to have your money work for you is by utilizing high-interest-earning checking accounts. Think Lake Michigan Credit Union, Consumers Credit Union, and others. Right now, you can find some credit unions and banks with checking accounts earning 3-4%. Use those earnings to bump up your vacation savings fund.

Speaking of your vacation savings fund, be intentional about it. Know you want to spend $5,000 on travel each year? Calculate what that equates to on a monthly basis and set it aside each month. This will encourage intentionality and lower the temptation to just “put it on the credit card” without actually having the cash to pay for it.

Have the cash but don’t know where you want to go yet or have longer than a 3-month timespan before you voyage off? Investing in a low-risk fixed-income vehicle might be an option for you. With the potential for rates being greater than your high-interest-earning checking account, this might be the perfect route to make your future vacation dollars work for you in your sleep (literally). Spark your interest? Leanne can chat with you to decide if this is a good move for you.

//

Do you have your suitcase out yet? I tried to warn you your travel fever will be ignited by the end of this. Sarah Allen is your new go-to for all things travel. Keep these tips in your back pocket, right next to your passport.

Fiduciary Financial Advisors, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Investments involve risk and are not guaranteed. Be sure to consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.

About Sarah…

Sarah Allen is a Travel Advisor with Fairytale Journeys specializing in Disney vacations, Universal Studios, cruises, and some all-inclusive resorts. Helping families plan a trip that fits their needs and budget is her passion. She loves helping others make lifelong memories with their families. She, of course, loves to travel herself, and sometimes planning trips is as much fun as going on the trip itself.

Married for 22 years, Sarah and her husband have 3 teenagers and 2 Goldendoodles. Her family has been traveling since her kids were very young and she has passed on the love of exploration to them all.

W: https://www.facebook.com/ftjbysarahallen

P: 269-929-0055

About Leanne…

Leanne Rahn is a Fiduciary Financial Advisor working with clients all over the US. If you don’t know what a Fiduciary is, Leanne encourages you to look it up (or even better - check out her website!). She swears you won’t regret it. Women entrepreneurs, newlyweds & engaged couples, and families who have special needs children are Leanne's specialties.

She loves a good glass of merlot, spending time with her hubs and baby boy, and all things Lake Michigan. She could listen to the band Elevation Worship all day long and is a sucker for live music.

Here, at Fiduciary Financial Advisors, we take our fiduciary oath seriously. We hold these five principles:

I will always put your best interests first

I will avoid conflicts of interest

I will act with prudence; that is, with the skill, care, diligence, and good judgment of a professional

I will not mislead you, and I will provide conspicuous, full, and fair disclosure of all important facts.

I will fully disclose, and fairly manage, in your favor, any unavoidable conflicts

Mega-Backdoor Roths Aren't Just For "Rich" People

There are many examples of situations where mega-backdoor roth contributions can be unexpectedly relevant but there are some overarching themes:

When the amount of money coming in during a year is significantly higher than usual

When your expenses are significantly lower than usual but your income hasn’t changed

When you’ve built up more savings than you need for your emergency fund and short-term goals

When one spouse has access to a 401k and the other working spouse does not

When many people learn about mega-backdoor Roth 401k contributions, they think to themselves, “this sounds like a great strategy for “rich” people”. Sure, it can be a lot easier for someone with a very high income to afford a $60,000 or $70,000 contribution every year and high earners are definitely a group that can benefit hugely from the mega-backdoor. But, there are two things I’d like to point out:

A lot of income doesn’t necessarily translate into a lot of disposable income or savings. Without the right money habits, people tend to spend more as they earn more and can even end up feeling like they have less of a cushion than they did when they earned less.

Income is just one part of a larger financial picture. Too many people never think beyond income and their basic 401k contribution to consider ways their savings, assets, debt, and expenses interact with and can complement those basic building blocks.

You could write an entire book on point #1 but I want to focus on point #2 with five examples of relatively common situations where, when you look at the whole picture, mega-backdoor contributions are attainable and can make a lot of sense, at least in a given year or time period. If you don’t have a clear idea of what your “whole financial picture” looks like, please reach out, that’s exactly what I’m here for.

You have a self-employed spouse. While there are several retirement account types available to self-employed individuals (we set these up often for new clients), many people either aren’t aware of them or feel it will be too complicated to set them up. In this situation it makes sense to think about your combined income and turn the spouse who does have access to a 401k into the super-saver of the family. If one spouse has no account to save for retirement, it can be pretty feasible for the other to be able to max out their 401k contribution and then use the mega-backdoor to boost savings even further.

You have extra cash after selling a home. With the massive increase in home prices some people are finding they’ve accumulated enough equity to have cash left over, even after making their down payment on a new home. Often people are unsure what to do with this cash and will let it sit in the bank earning nothing. Some may at least take the step of investing it so it can grow. But, that growth will be taxed. In this situation, maxing out a 401k and then making a mega-backdoor roth contribution is an ideal way to essentially shift that money into a tax-free account where it can grow and never be taxed again!

You have more in the bank than you need for your emergency fund. This could be a sign that you’ve been under-saving for retirement. If so, maxing out your 401k for a year or two and making extra mega-backdoor contributions is a great way to catch up, get that money growing, and avoid tax on that growth. If you have been saving enough and are still in this boat, layering on mega-backdoor contributions could help get you to retirement or financial independence sooner than you thought possible.

You had a windfall or unusually high compensation this year. Most people don’t win the lottery so more often this could be an inheritance, a gift from a family member, an unusually large bonus at work, a stock grant, or an unusually “good year” for commission-compensated workers. Often in these situations the income is unexpected and therefore not already “spoken for”. If you want to avoid the temptation of spending it just because it’s there, a mega-backdoor contribution is a great way to essentially shift this money to an account where it can grow tax-free.

You moved or made a life change that has reduced your expenses dramatically. As remote work exploded during the pandemic, some people have been able to keep jobs with “big city” or “coastal” pay while moving to areas of the country with a much lower cost of living. Others may have moved in with aging parents to help care for them and have seen their living costs plummet as a result. Maybe kids moved out or finished college that you were paying for. While maxing out your 401k may have been unobtainable before, it may now be a very real option to consider along with going even further and making mega-backdoor contributions.

There are many more examples of situations where mega-backdoor roth contributions can be unexpectedly relevant but there are some overarching themes:

When the amount of money coming in during a year is significantly higher than usual.

When your expenses are significantly lower than usual but your income hasn’t changed.

When you’ve built up more savings than you need for your emergency fund and short-term goals.

When one spouse has access to a 401k and the other working spouse does not.

If you need a primer on what a mega-backdoor roth contribution is and how to make one you can check out my summary blog post on this topic: Mega-Backdoor-Roth

2023 Contribution Limit and Tax Adjustments (mostly) Keep Up with Inflation

While the 2023 social security cost-of-living increase of 8.7% grabbed most of the headlines, the IRS also adjusted tax brackets and contribution limits for 2023 to keep pace with the 8.2% annual inflation rate reported in October. While many adjustments kept up (401k contribution limits increased 9.8%, IRA limits by 8.3%), the Feds were stingier with others (tax bracket thresholds increased only 7.1%, the standard family deduction by 6.9%, Roth income limit by 6.9%).

While the 2023 social security cost-of-living increase of 8.7% grabbed most of the headlines, the IRS also adjusted tax brackets and contribution limits for 2023 to keep pace with the 8.2% annual inflation rate reported in October. While many adjustments kept up (401k contribution limits increased 9.8%, IRA limits by 8.3%), the Feds were stingier with others (tax bracket thresholds increased only 7.1%, the standard family deduction by 6.9%, Roth income limit by 6.9%). I’ve summarized the major updates for 2023 below.

If you have any questions about how these changes may impact your saving or financial plan in the coming year feel free to reach out to me at ryan@ffadvisor.com or 616.594.6205.

Retirement Account Updates

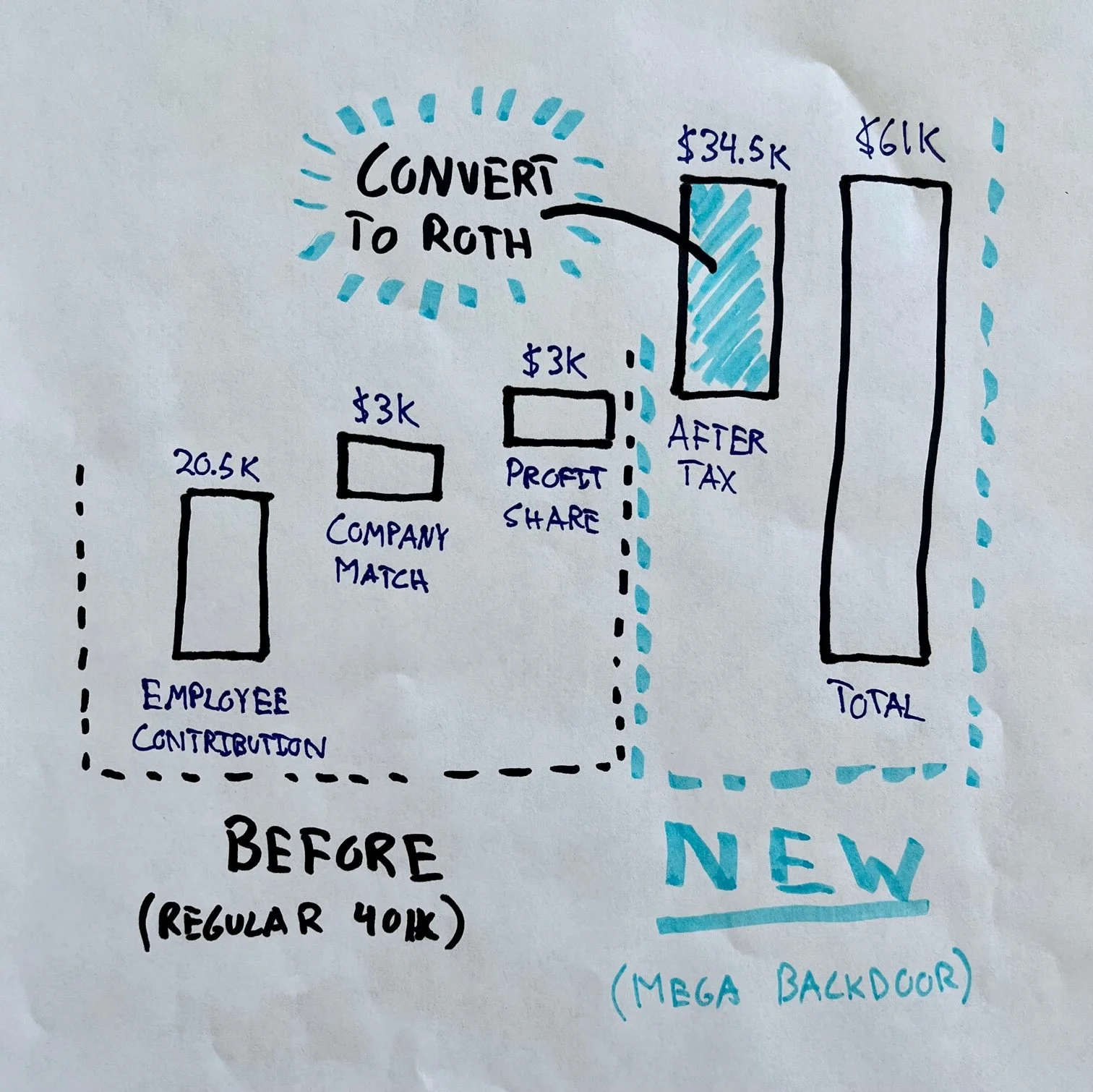

401k contribution limit increased by $2,000 from $20,500 to $22,500

IRA contribution limit increased from $6,000 to $6,500

401k catch-up contributions increased from $6,500 to $7,500

IRA catch up contributions did not increase, they are still $1,000

SIMPLE retirement account contribution limit increased from $14,000 to $15,500

Roth IRA income limit phase-out increased:

Between $138,000 and $153,000 for singles and heads of household

Between $218,000 and $228,000 for married filing jointly

SEP IRA contribution limit increased from $61,000 to $66,000

HSA contribution limit increased from $3,650 to $3,850 for singles. Family coverage increased from $7,300 to $7,750.

Tax Updates

Standard Deduction for 2023: Married filing jointly $27,700 up $1,800 from the prior year. For single taxpayers and married individuals filing separately, the standard deduction rises to $13,850 for 2023, up $900.

Tax Bracket Adjustments for 2023:

35% for incomes over $231,250 ($462,500 for married couples filing jointly);

32% for incomes over $182,100 ($364,200 for married couples filing jointly);

24% for incomes over $95,375 ($190,750 for married couples filing jointly);

22% for incomes over $44,725 ($89,450 for married couples filing jointly);

12% for incomes over $11,000 ($22,000 for married couples filing jointly).

For tax year 2023, the foreign earned income exclusion is $120,000 up from $112,000 for tax year 2022.

Estates of decedents who die during 2023 have a basic exclusion amount of $12,920,000, up from a total of $12,060,000 for estates of decedents who died in 2022.

The annual exclusion for gifts increases to $17,000 for calendar year 2023, up from $16,000 for calendar year 2022.

Social Security Updates

COLA Increase for 2023 will be 8.7%

Earnings limit for social security benefit adjustment for workers younger than full retirement age: $21,240

Fiduciary Financial is not a tax advisor, these figures are provided for informational purposes only.

Mega-Backdoor Roth - The Hidden 401k Feature that can Supercharge Your Retirement Saving

Saying that the Mega-Backdoor Roth strategy can supercharge your retirement saving is not a hyperbole. In most situations, maximizing this feature MORE THAN DOUBLES the amount you can save to Roth accounts each year. Once those savings are invested in a Roth account, they can grow tax free for years or decades and be withdrawn tax free* in retirement.

The “mega-backdoor” can have mega tax impacts

A quick example illustrates just how powerful those tax savings can be:

Each year for 20 years, “normal 401k Charlie” maxes out his Roth 401k with $20,500 and invests an additional $40,500 in a taxable investment account. Both accounts grow at 6% per year. At the end of 20 years, Charlie has $1,497,169 in his taxable account and $757,826 in his 401k; $2,254,995 in total. While Charlie’s Roth 401k savings can be withdrawn tax free in retirement, he will owe capital gains tax on the $687,169 of his investment gains in the taxable account. At long term capital gains rate of 15% that would be $103,075 in taxes! This doesn’t even include taxes he would likely have paid on dividends in the taxable account over 20 years.

“Mega-backdoor Bettie” on the other hand maxes out her normal $20,500 Roth 401k contribution and is able to invest an additional $40,500 into her Roth 401k through the Mega-backdoor strategy. After 20 years, with the same investment return as Charlie, Bettie has the same total savings of $2,254,995. However, Bettie can withdraw that full amount tax free in retirement.

In this example the Mega-backdoor saved Bettie $103,075 on taxes! She also didn’t pay tax on any dividends along the way.

How to implement the Mega-Backdoor strategy

Hopefully this example helps illustrate that the Mega-Backdoor Roth can be a powerful tax-saving strategy, but how does it work? By making after-tax 401k contributions and in-plan Roth conversions. Let’s break those two steps down:

1) Allowing after tax 401k contributions increases the maximum amount employees can contribute from $20,500 in 2022 to $61,000* (or $67,500* if you’re over 50). After-tax contributions don’t reduce your taxable income or tax bill today, but this is where the in-plan Roth conversion is key.

2) Through an in-plan conversion you can easily take those huge after-tax contributions and convert them to Roth funds within your 401k (or through rollover conversions to a Roth IRA). Once converted, your savings grow tax-free and can be withdrawn tax free in retirement just like normal Roth 401k or Roth IRA contributions.

This is the power of the mega-backdoor, it allows you to quickly build a much bigger tax-free* retirement nest egg than you could with a typical 401k and Roth IRA alone. And, unlike a Roth IRA where households over the income limit aren’t allowed to contribute, anyone in the plan can contribute with no income cap. This means even high earning households can mega-backdoor. It’s actually this group that can benefit the most!

Some 401k plans don’t support the Mega Backdoor and some require an extra step

Unfortunately, many 401k plans don’t allow allow for employees to make after tax contributions. Sadly, there’s not even a good reason for this other than perhaps some added administrative difficulty. That said, it is becoming more and more common and will likely continue to grow in popularity. Some plans allow for after tax contributions but don’t have a program set up for in-plan conversions to Roth. This is where a second step is needed to see if the plan does allow for “in service distributions” so that employees can roll over their after tax contributions to an IRA and convert them to Roth. If you’re unsure what you’re plan allows or how to execute this step please reach out, I’m happy to help.

The Mega Backdoor isn’t right for everyone

Let’s be honest, making mega-backdoor Roth contributions isn’t realistic for a lot of people. Maxing out a $20,500 annual contribution is already a lot! In fact, it may already be more than enough for your situation and retirement goals. That said, there are a lot of unique situations where a mega backdoor strategy can become unexpectedly relevant, I’ve written about several of them here: Mega-Backdoor Roths Aren’t Just for Rich People.

Like any large money decision, mega-backdoor Roth contributions should be part of a bigger financial and tax strategy built around your needs, your timeline, and your goals. If you’d like help building a strategy tailored to your timeline and goals (or figuring out if your employer allows the mega-backdoor), feel free to reach out, I’d love to see if I can help or direct you to someone who can. You can reach me by email at ryan@ffadvisor.com or cel phone: 616.594.6205.

Footnotes:

*Roth savings grow tax-free. Contributions can be withdrawn without tax or penalty at any time and investment gains can be withdrawn tax and penalty-free after age 59-½ (or 55 if the “rule of 55” applies to you).

*$61,000 and $67,500 are the 2022 limits for employee contributions, employer matches, and profit sharing contributions combined. Your max contribution = $61,000 or $67,500 - employer match - profit sharing contribution.

A Few Logical Questions During a Time of Malaise

A few logical questions during a time of malaise

Bear markets beg critical questions that shake the foundation of long-term investing. We seek to answer these questions to stay the course and build for the long-term.

A few logical questions during a time of malaise

Bear markets are defined as a 20% decline from a high-water mark in a security or index. I believe that a bear market is better defined by feelings of pessimism and fear. I would sum these feelings up with one word: malaise. By the ladder definition we have been feeling malaise since roughly February in financial markets. This feeling begs a few natural questions that I will offer opinion around.

When does the malaise end?

Many will guess and some will get lucky, appearing to be seers of future events (you can always test their accuracy by asking for past predictive accuracy). The point remains that no serious market participant knows for certain when this will end. We could be days, weeks, or months away from this point. I believe the key variable to break this market pessimism is the Fed (Federal Reserve). It won’t occur the day the Fed says or signals that they are done raising rates, the turn will occur before that in anticipation of said occurrence. Keep in mind, I believe the Fed is the key variable but not the only variable. There are a litany of additional variables that could change the market’s course thus making clean predictions around the course of a future market a risky endeavor. We will entirely avoid said endeavor.

What will it look like when the market turns?

Again, no serious market participant knows. We could have a rapid move higher if the Fed is able to pivot from increasing rates to holding or cutting rates while peace pervades in Ukraine and the US/world avoids damaging recessions. Consequently, we had a dry run of what the market would look like if there was a swift recovery. From a low on June 16th, we watch the S&P 500 rally back north of 17% in roughly a two-month period. This could be called a “V” shaped recovery given the shape created on a graph of a quick drop and quick recovery. This is one probable outcome while another, readers of my early piece “Fear of Flatness” know this outcome, is a choppy, directionless market. This outcome could already be showing as the afore mentioned rally has largely dissipated (as of this 9/22/22 writing) to leave us sitting near the mid-June lows. We must prepare for different potential recoveries from the lows in the market.

What should be done in these markets?

An absence of action can constitute a purposeful choice. Simply put, making huge changes in volatile times can often substitute short-term relief for slow, long-term pain. Not making moves is a decision in and of itself.

Having the confidence to believe we or anyone we follow can confidently call the bottom and subsequent invest accordingly is not the course we choose. Helping our clients maintain the best asset allocation for their given situation based on financial planning and the ability to absorb various market outcomes is the chosen path. There is a saying that “you are rewarded for time in the market not timing the market”.

We favor small, incremental changes based on high probability outcomes. For example, increasing portfolio exposure last year and the beginning of this year to dividend paying stocks can help ride through a down or choppy market because of the organic portfolio cash-flow created by these dividends. The investment saying here is “a bird in the hand is worth two in the bush”. In times of stress, you want to know what you are holding not what you are fantasying about holding.

Fine, I understand all of this, but is there any silver lining?

Yes, yes, a thousand times yes. Money now has a cost and that is, very probably, good for long-term economic health. Simply, if you or a company borrows funds to fuel a purchase or capital project, the project must now produce larger or more certain returns than it would have a year prior. This leads the market to cull weak capital investment ideas in favor of strong, sustainable projects.

Furthermore, savers are now rewarded exponentially more on a nominal basis than they were just twelve months ago. For example, if you had bought a 1-year treasury bond last September it would have yielded under 0.10%. Today a new 1-year treasury yields over 4.00% (as of 9/22/22). Over a 40x increase in yield. While this punishes borrowers and slows economic activity in the short-run, we are of the opinion that a more balanced cost of borrowing/reward for savings can act as a catalyst for the next, multi-year economic and equity market expansion.

To enjoy the wealth creating benefits of our free-market, capitalist system we must have periods of reset where weak, over leveraged borrowers are punished in the short-run and the strong, prudent capital allocators are rewarded in the long-run.

Final thoughts

Risk assets are on sale. If you accept the thesis about the in-ability to peg the bottom of the market, you can still rest assured that mathematically the average stock is anywhere from 10-30% lower than it started the year. If you look at the index level like the S&P 500, you are buying at a roughly 20% lower price than the start of the year. This doesn’t guarantee huge returns; however, historic precedence would indicate you have a higher probability of better future returns than had you purchased at the beginning of the year.

This year has not been fun nor rewarding in almost any asset market. Keep in mind that the decisions of today determine the returns of tomorrow. We keep today’s decisions, with high conviction, focused on the long-run, resisting short-term needs for catharsis, and take advantage of small, tactical moves for long-run success. This malaise too shall pass.

As always, I am available for questions, feedback, commentary, or just to chat by cell 248.982.8190 or email rob@ffadvisor.com. Be well and focus on the long-term!

Are Your Financial Passwords Leaked On The Dark Web?

Advice From A Cyber Security Expert

Andrew Rathbun is a cyber security professional with seven years of experience between local/federal Law Enforcement and the Private Sector. Andrew has spent the last 2.5 years responding to ransomware incidents for businesses at every scale. Andrew is heavily involved in the Digital Forensics and Incident Response (DFIR) community. He enjoys writing blog posts, sharing research, contributing to open source projects, publishing books, and learning from and collaborating with other professionals in the field. Below are Andrew’s answers to a few questions I had for him regarding online financial accounts.

1. What are the biggest threats to keeping online financial accounts secure?

The biggest threat is when people use the same passwords that have long since been compromised in numerous hacks. You should make sure your current passwords aren’t in the infamous “RockYou” password leak, which can be found here. This is a commonly used password list by hackers when they want to attempt brute forcing (trying many passwords to see if one will work) accounts to gain access and carry out their goal of stealing all your money!

Additionally, some financial institutions do not have multi-factor authentication (MFA). My credit union doesn’t currently, which is crazy to me! Email/Password combinations used for some of the most important accounts people own are floating about on the dark web. You should use multi-factor authentication for every financial account if possible.

2. What is the best way to create a secure online password?

Using a random password generator is the best thing you can do. This can make it difficult to remember all of the random passwords though. So once the random password is generated, you then have to decide the best way to store/remember it. For examples of strong passwords, use a site like this one to create a password that is difficult to crack.

3. What is the safest way to save/store these secure passwords?

It is vital to use a password manager. I use 1Password as my password manager. I like it because I can use my email and an easy-to-remember password to access my password vault, which contains ALL of my passwords for every login I have. What makes it secure is that not only do you need the typical email/password combination to log in, but you also need a secret key that is unique to your account. If you use a password that has long since been leaked as associated with your email, a hacker will need to know your secret key, which is a random string of numbers and letters, before they can log in to your password vault.

Within my 1Password vault, I don’t know any of my passwords by heart. They are often 20+ characters and include lowercase characters, uppercase characters, symbols, numbers, and other special characters. There’s no way I could remember one let alone hundreds of different passwords. On some of my most valuable accounts, I have 50+ character passwords! I use 1Password on my phone and computer to log in to my accounts, so I don’t have to remember those passwords because they are simply too secure to remember. If ever they get leaked and therefore associated with my email account, I’ll just regenerate a new 20+ character password and replace it in my vault with the one that was compromised.

4. Any password managers that you would recommend that are free?

I’ve personally not used any free password managers, but one free password manager I would not recommend is your web browser. Obtaining your saved passwords from a browser like Firefox or Chrome is trivial for a motivated bad actor, and frankly, I could download a free tool right now and obtain the passwords stored in my web browser without much effort.

If I had to choose a free password manager, the first I would consider looking into would be BitWarden on account of the program being open-source. What does this mean? That means the source code that makes it work is completely transparent to the public. If there are vulnerabilities, those who have the knowledge can identify them and suggest changes to the program to make it more secure so everyone benefits. For those not in the cyber security industry, this is a very common occurrence where a tool is free and open-source where improvements, bug fixes, and any other feature requests are encouraged.

5. What is a VPN, how does it work, and should the everyday person use one?

A virtual private network (VPN) is something that people can use to make their internet traffic secure from people who are trying to steal their data. VPNs are secure but they can be very slow. Without a VPN, if you go to a website, data travels from your computer directly to the website’s servers. With a VPN, the data travels from your computer, to Israel, to Switzerland, to Brazil, and then to the website you’re trying to go to. Therefore, the website will load much slower than without a VPN.

The everyday person should strongly consider using a VPN when connecting to public Wi-Fi, such as the airport or a local diner. Unsecured Wi-Fi networks allow bad actors to easily sniff for packets of your data going to and from your computer, including but not limited to your email/password combinations when you’re logging into your bank account on said public Wi-Fi network.

6. Any good VPN services that you would recommend?

If you care about privacy, then you want to use a VPN that’s based out of a country with favorable privacy laws. Switzerland is widely considered to have the most robust laws on privacy when it comes to consumer data. ProtonMail, a privacy-focused email provider based out of Switzerland, has a VPN service called ProtonVPN. I use it and I very much recommend it. The philosophy of Proton is admirable and the fact it’s based out of Switzerland is a huge plus for privacy. Proton also embraces the open-source mindset that I admire about BitWarden and many other projects within my field of work.

7. Any other best practice recommendations?

Use a password manager, enable multi-factor authentication (MFA) on every account that provides that as an option, and change any passwords that you’ve been using since high school!

Remember if something is free and you are not paying for it, then you are the product. Your data, your interests, your everything is being sold by advertisers like Google for profit. It’s not that any of us have anything to hide, but there’s a reason why we all don’t have 24/7 freely accessible streaming cameras in our bedrooms for all the world to see.

Also, if you try to sell something on Facebook like I did tonight for the first time in a few years, and multiple accounts message you asking if the item is available within a minute of the posting, they are very likely bots. Sure enough, the first 4 accounts that asked me if the item was available ALL asked if they could call me with their second message. In the next message after I said “no, I don’t give out my phone number” they asked if I could post my phone number so they could call me. I immediately blocked them at that point. You have to take a moment, slow down, and not be in such a hurry to make the sale and ensure your data’s privacy is maintained as much as possible. Why would this person want my phone so badly? I thought they were interested in the mattress I’m trying to sell. Truthfully, my phone number is more valuable to them than the mattress, and they know I want to sell the item badly enough because otherwise why would I be posting about it on Facebook where there are tens of thousands of people on each of these 10+ groups I posted the item in? Much like the term innocent until proven guilty, nowadays I see things as scams until proven otherwise.

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

Is This Jar Full? Is Your Life Full?

After watching this video, take a minute to reflect on what your current “golf balls” are in your life. If they aren’t what you want them to be then make a plan to change your priorities and start allocating your time differently!

“When you create a difference in someone’s life, you not only impact their life, you impact everyone influenced by them throughout their entire lifetime. No act is ever too small. One by one, this is how to make an ocean rise.”

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

5 Ways to Fight Inflation as a Business Owner

Fiduciary Financial Advisors, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Investments involve risk and are not guaranteed. Be sure to consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.

Surviving Your First Market Crash

Picture this: you’re young, living life, killing it at your first “adulting” job, putting those dollars away for retirement, finally making some good money, and then boom - the market crashes. Social media blows up, politics get even more heated, your invested savings drop lower and lower, and you can’t seem to escape the dark shadow of worry. Sound familiar? Well, hang in there, because you're about to get all the deets on how to survive your first market crash.

First, let’s start with the technical definition of a market crash. A market crash is when the market falls 20% or more from the very top. Crashes can take longer to recover from and may last years. They also are often accompanied by a recession and usually are a result of some systematic failure or other reasoning. Okay, so now you know how to identify a market crash. Now, let’s talk about how you can gear up and weather a storm when it comes.

Don’t Stop Investing

Wait, you’re telling me to continue putting my money into the thing that feels like it’s going to collapse at any second? Yep. If you’re a client of mine, you know we are all about the long-term mindset. Markets go up and down throughout your lifetime and you are feeling the pain of your first major market downturn. Pain isn’t easy. It stings. It can be lingering. But the amazing thing is pain can be healed and can go away with time. And guess what! You have the time. Retirement is more than likely 3 to 4 decades away for you. Market downturns are a part of investing and will happen again in your lifetime. Author, Carl Richards, puts it best in his sketch below. Days can feel painful, all over the place, and scary. But zoom out and take a look at the big picture.

By continuing to invest, you can take advantage of the market downturns and investments being less expensive. Not only that but get in on the downside and you are fully prepared to ride the wave back up when the time comes (aka you are making money). If you wait until the market is “looking good” again, you might miss the opportunity for growth. Now, I’m not saying to time the market. But what I am saying is investing at regular intervals regardless of the market performance is a healthy habit to have (dollar cost averaging, my friends).

Tune Out the Noise

Remember that pain I was talking about? You’re not the only one feeling it. So is your boss, your parents, your neighbor down the road, and your local grocery store. It’s everywhere when there is a market crash. So naturally, that is what’s going to be flooding your social media timelines. I’m here to tell you to shut it off. Tune out the noise of your Twitter’s worry and your Facebook’s advice. If you find yourself constantly logging into your IRA and 401k accounts to check the balance - don’t. Trust me, it will help you feel less of that temporary pain. From our previous conversation above, you know you have time. Focus on the decades, not the days. Temporarily unfollowing some select individuals and deleting your investment apps might just help you forget the pain is there.

Make Sure Your Financial Advisor is Doing Their Job

When you go through your first market crash, I want you to pay close attention to your advisor. I’m not talking about performance (because let’s be real, if the market crashed, more than likely your accounts will have dropped no matter who your advisor is). I want you to pay close attention to their communication and education. Are you hearing from them? Are they checking in and educating during a market crash? A good advisor communicates with their clients especially when the market is a little wobbly. If you are a client of mine, you know I send quarterly newsletters to educate you with what’s going on in the market. Not only that, but you can expect communication from me when turmoil in the market comes. How does your financial advisor communicate with you? Will they listen to your concerns? Will they educate and help set your focus on what matters? Remember - you hired them.

Crashes will be inevitable in your lifetime. Knowing what to do when they come will play a huge role in your long-term financial success. So keep making strides in your career and keep building up those savings. Pain is temporary and if you focus on the right things, the pain might just start to feel like opportunity. Gear up and don’t just survive in a market crash - thrive in it.

Fiduciary Financial Advisors, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Investments involve risk and are not guaranteed. Be sure to consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.

Here, at Fiduciary Financial Advisors, we take our fiduciary oath seriously. We hold these five principles:

I will always put your best interests first

I will avoid conflicts of interest

I will act with prudence; that is, with the skill, care, diligence, and good judgment of a professional

I will not mislead you, and I will provide conspicuous, full, and fair disclosure of all important facts.

I will fully disclose, and fairly manage, in your favor, any unavoidable conflicts

5 Ways to Prepare Your Business For a Recession

Recessions, hard times, and slow growth are all things no small business owner wants to hear. But the reality is you will have times like these in your business. How do you prepare as a business owner? What can you do right now to go confidently through a natural phase of your business life? Let’s jump into five ways you can prepare your business for a recession:

1. Build That Emergency Fund

We often talk about emergency funds on the personal side but we can’t forget about the business side. Set a goal to build a business emergency fund that would cover 3-6 months’ worth of business expenses (things like office supplies, payroll, rent, software subscriptions, etc.). There is always going to be something else you’d rather spend your business dollars on, but trust me when a recession hits you will feel so much better knowing your business essentials are taken care of.

2. Pay Down Debt

Do you have a business credit card or a business loan that has reoccurring balances? Now’s the time to try and minimize that debt - especially debts with a high-interest rate. Being tied to a lender is never a good feeling and it’s even more challenging when business is hurting due to the economic surroundings. Once you have an established business emergency fund, chip away at that debt. Your future self will thank you.

3. Look Ahead

All businesses have some seasons that are slower than others. Look ahead at your expected business activity in the months to come. Are they usually slower or perhaps you're coming up on your busiest time of the year? Taking a glance forward will help you know what to prepare in the now. If you know the slow months are quickly approaching, it might be time to build that extra cash reserve (maybe even slightly larger than normal) to tackle the slow months and weather a recession.

4. Revisit Your Marketing Plan

It’s always a good idea to review your current marketing plan every so often to know what’s working and what’s not. Both your time and your potential leads are valuable - we want those two things to complement each other. Carve out an hour or two out of your time to do a deep dive into your marketing streams. Where are you getting most of your business? How much are you spending and are the dollars coming back to you in the form of new business? What type of marketing takes the most of your time and is it worth it? Are there new streams you could be taking advantage of? If and when a recession comes, you can confidently know your marketing strategy is at its best.

5. Review Your Current Expenses

With subscriptions being at the click of a button nowadays, it can be easy to forget what services you are paying for and how much you are actually paying. There are some expenses that definitely are worth paying for and help your business tremendously but it’s a good habit to often review your current expenses to decipher that. Clean up your business budget and make the most of your business dollars by staying on top of your monthly costs. On the other hand, is there a service or product that, if purchased, will increase your productivity/your time/your leads/your quality/etc.? Then click that “checkout” button! This tip isn’t just to cut back on all your expenses but to help your business and your revenue be the most efficient possible.

As I mentioned at the beginning of this conversation, talk of recession is never something a small business owner wants to hear. But coming to terms with this natural economic wave and knowing how you can prepare will allow you to ride the wave with ease. So get to work on building your emergency fund, minimizing business debt, looking ahead at your business activity, revisiting your marketing plan, and reviewing your current expenses. The storm is a lot less fearful when you have shelter and an umbrella in hand.

Fiduciary Financial Advisors, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Investments involve risk and are not guaranteed. Be sure to consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.

How to Beat Inflation

What is Inflation?

Recently, inflation has been a hot topic, but what exactly is inflation and why does it matter so much? Inflation is the rate of increase in prices over a given period of time caused by an increase in the money supply. Since this causes more money to chase after the same amount of goods and services in our economy, prices increase. Our money then has less purchasing power because we end up paying more for things than before. Inflation is not a new phenomenon, but it hasn’t been a big issue since the early 1980s.

If we look at the M2 money supply data below, which is how the Federal Reserve broadly measures the money supply, you will notice the large increase that happened during the COVID pandemic to try and help stimulate the economy. People can debate back and forth if that was the right or wrong thing for politicians and the Federal Reserve to do. I would like to instead focus on some practical tips to help weather the “inflation storm” and potentially come out on the other side unscathed or even better than before!

Have an Emergency Fund!

Having money sitting in an emergency fund is not the most exciting tip, and inflation will indeed decrease that purchasing power. However, the purpose of an emergency fund is not to make a high return. It is to have a liquid supply of money available in an emergency. Going without one could lead to more serious financial issues if something unexpected happens and you don’t have enough cash to cover it. Since the Federal Reserve has started to increase interest rates, we should see that translate into higher yields on savings accounts soon!

Typically, I’d recommend 3-6 months of living expenses in your emergency fund, but you may want more or less depending on your situation.

Are you single?

Do you have children?

Are you a one-income or two-income household?

Is your job in a high-demand sector?

Could you easily find another job quickly if needed?

These are some questions you should consider when deciding how much money you should keep in your emergency fund.

Own Assets!

Owning assets that produce income could help during high inflation and protect your purchasing power. As inflation increases, these income-producing assets should be able to increase their rates to help soften the blow felt by inflation. Real estate properties can command higher rents as inflation increases. If you can’t afford to purchase an entire property then REITs (Real Estate Investment Trusts) are the other potential option to gain access to that asset class with smaller capital amounts.

Owning businesses is similar. The money the business receives as income may become less valuable due to inflation. If the business can increase the prices charged for goods and services, then the greater amount of income could offset the money being worth less. If you can’t afford to purchase an entire business, then consider owning parts of businesses through stocks, mutual funds, or index funds.

Own Debt?

I wouldn’t encourage anyone to go out and accumulate more debt. If you already have a fixed low-interest debt such as a mortgage, it may make sense to delay paying it off early. If inflation remains high, the money you use to pay back that debt will be worth a lot less in the future than the money you originally received. Using that money to invest in other assets could be a much better option.

Review Your Expenses

With inflation running high, it’s the perfect time to look at your expenses. Review what you are spending your money on to figure out if it aligns with your long-term goals. Do you need five different streaming services? Is it time to stop eating out as often and start cooking more at home? Is it time to start carpooling to save on gas prices? Incorporating some of these ideas to help reduce your expenses is another potential way to decrease the effect felt by high inflation.

Invest in Yourself

I saved the best for last! Investing in yourself is one of the best ways to deal with inflation. Learn a new skill, read a new book, take a new class/certification program, and grow your knowledge base. By making yourself more marketable to your current/future employer and providing more value for them, you should be able to command a higher salary. That can help make inflation not sting quite as much. Even though things will cost you more, earning more money to help offset those costs can be a difference-maker.

James Clear, the author of Atomic Habits, shared a powerful principle: a 1% improvement every day leads to you being 37x better at the end of the year. And I’m confident you can get 1% better at something every day! Inflation does not prevent you from improving yourself.

“Whatever abilities you have can’t be taken away from you. They can’t actually be inflated away from you. The best investment by far is anything that develops yourself, and it’s not taxed at all.”

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

Is it too late to start living like a Millionaire?

Do you want to become a millionaire? Do you want to live like a millionaire? It might not be what you envision. One author spent over a decade researching, investigating, and interviewing millionaires to explore how the average millionaire lives. Here are his insights from Thomas Stanley’s book, The Millionaire Next Door.

They live well below their means

The average millionaire doesn’t spend more than they earn. They don't buy fancy clothes; they shop for clothes at places like Target, Meijer, and Wal-Mart. They don't drive fancy car brands like Porsche, Ferrari, and Lamborghini. They drive cars made by Toyota, Honda, and General Motors. They don't live in mansions overlooking the ocean. They live in a well-taken-care-of home next door to you, which explains the title of the book.

True millionaires allocate their time, energy, and money efficiently, in ways conducive to building wealth.

The average millionaire is productive with their time. They spend much more time reading and much less time watching TV than non-millionaires. They don’t waste their money on lottery tickets or get-rich-quick schemes, hoping to become rich. They invest their time and money in improving themselves, learning new skills, starting businesses, and networking with other successful people. They exercise more and eat healthier. They start investing in their tax-advantaged accounts early!

They believe that financial independence is more important than displaying a high social status.

The average millionaire understands that being wealthy isn’t about showing off or one-upping their neighbor. Instead of buying a bigger house or fancier car, they would rather build wealth. They understand that building wealth allows them to gain back control of their time. Being financially independent allows them to spend more time with their family, volunteer more, work at a job they enjoy, and participate in hobbies they love. They understand the difference between appearing rich and being wealthy.

Their parents did not provide economic outpatient care.

The average millionaire did not inherit their wealth as many people assume. While some families do pass down wealth from generation to generation, research shows that the vast majority of millionaires are self-made. They did not receive large inheritances but built their wealth slowly over time.

Their adult children are economically self-sufficient.

The average millionaire is not supporting their adult children. They taught their children the principles of finance, which include delayed gratification and the power of compounding interest. They discussed their family finances early and often. They provided for their children's needs but did not fulfill every want. They taught them to work hard and to work smart. They taught them how to make their money work for them instead of the other way around.

They are proficient in targeting market opportunities.

The average millionaire learns that money is a medium for transferring value. If they provide a product or service to somebody, they receive money, which can then be spent to receive a product or service back. They use this information to stay on the lookout for opportunities where there is a lack of products or services. Then they use their knowledge and resources to provide that need which is in high demand. Improving efficiency is another value-add opportunity the millionaires use to generate wealth. Money flows to wherever value is created.

They chose the right occupation.

The average millionaire has found an occupation that matches their skill set and personality well. They enjoy going to work most days and look forward to being productive. Enjoying their job allows them to excel, which leads to being compensated well.

I encourage you to start implementing these insights in your life. If you enjoyed this overview, I would highly recommend reading the book!

“You will be the same person in five years as you are today except for the people you meet and the books you read”

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

What is a SEP IRA?

A SEP IRA is a great long-term savings vehicle designed for any employer, including self-employed individuals. There are some important factors to know when it comes to deciding if a SEP IRA is right for you and your business.

Want to know more? Click below to be instantly educated on SEP IRAs.

Michigan's NEW First Time Home Buyer Savings Account

Have you heard about Michigan's NEW First Time Home Buyer Savings Account???

If you haven't, you'll for sure want to be in the know. In February of this year, Governor Whitmer signed a bill allowing first time home buyers to save and grow their savings TAX-FREE (if used for a qualifying expense)!

You can learn all the deets below. This is an amazing opportunity if you and your spouse are saving for a home or will be in the upcoming years.

If the stock market is crashing! What should I do?

One of the most important rules when it comes to investing is to buy low and sell high. And yet, some people end up getting nervous when the stock market is “crashing” and end up selling low. Then, after the market recovers, they regain confidence and end up buying high. Letting one’s emotions control investing decisions is a recipe for poor returns.

You may see on the news or social media people claim that they know what the market is going to do in the future. Often people say these things to try and get more viewership and clicks instead of trying to give sound financial advice. But recall the adage that “even a broken clock is right twice a day”. Don’t be surprised when someone’s lucky guess happens to be accurate from time to time. Instead, focus on taking financial advice from a fiduciary, someone who is legally required to act in your best interest and not their own.

So what should you do during a volatile market? Without knowing the details of your financial situation, I can’t provide specific advice. However, I would like to review some data from the past to help you gain a better understanding of the markets and consider a “market crash” as a potential opportunity to buy. This is looking back at previous returns so make sure to note that past performance is no guarantee of future results.

In the world of finance, there are two different types of markets: a bull market and a bear market. A bull market is a time frame when the economy is expanding and stock prices are increasing, while a bear market is when the economy is experiencing a recession and stock prices are decreasing. As you can see from the chart below, bull markets typically last longer than bear markets and produce greater returns compared to the losses of a bear market. The U.S. has been in a bull market for a while so when it transitions to a bear market or recession that will not be out of the norm when looking back in history.

Since bull markets typically last longer than bear markets, the odds that someone makes money investing in the stock market could increase significantly the longer they leave their money invested. The chart below shows the probability of someone having positive returns investing in the S&P 500 index since 1937. If someone only invested for 1 day they had a 53.4% probability of having positive returns but if they stayed invested for 10 years they had a 97.3% probability of having positive returns! I prefer the much higher probability of higher returns by not trying to time the market.

The chart below shows the 15 largest single-day percentage losses for the S&P 500 since 1960. If you look at the right side you will see in the one year later column that only one time was the market negative one year post the corresponding single-day percentage loss. That was back in 2008 during the global financial crisis. Instead of becoming nervous about large single-day losses reassure yourself that more than likely the market will recover within one year.

Think about it this way, I LOVE Heath candy bars for obvious reasons. If I bought them as a snack and then Meijer sent me a coupon for 50% off, I wouldn’t get upset that I had just paid full price. I’d go and buy more. Selling stock when the market plummets would be a lot like me selling my Heath candy bars for 50% less than what I paid for them vs. buying more at such a great price!

Hopefully, this has helped you gain a better perspective on making investing decisions. I believe that having a longer-term outlook can help you keep emotions in check and not get as nervous/scared when you see people on the news and social media talking about a stock market crash.

Just like gym workouts are more productive with a trainer, folks often are better able to keep their emotions in check by having a talented financial advisor on their team. If you don’t have a financial plan established now might be as good of a time as any to get that put in place. I would be happy to meet with you to discuss your financial plan.

“We simply attempt to be fearful when others are greedy and to be greedy when others are fearful”

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

THE STEWARDSHIP PODCAST // Stewarding Your Money with Leanne Rahn and Connor McDowell

Stewarding Your Money with Leanne Rahn and Connor McDowell

Episode Description

On this episode I am joined by my friends, colleagues, and fellow financial advisors Leanne Rahn and Connor McDowell. We tackle all things stewarding your money. Don't forget to join the SP community on Facebook.

MONEY SESSIONS // The Power of Reinvesting in Your Business with Mista Caswell

The Power of Reinvesting in Your Business with Mista Caswell

Episode Description

In today's money session, we chat with Mista Caswell - a small business owner and West MI photographer specializing in weddings and engagements, lifestyle, and senior sessions. We chat all about the power of reinvesting in your business. Mista discusses her real-life examples of how prioritizing her business's growth has impacted the quality of work she can provide to her clients. If you are a business owner playing around with the idea of reinvesting into your business, this session is for you!

Traditional vs Roth Retirement Account, Which Is Better?

What is the difference between a traditional account and a Roth account? Which one is better for you? Which one should you invest in? Several factors can affect your decision. I will help you explore concepts to think about to assist when making that decision.

The main difference between a traditional account and a Roth account is the timing of when you pay taxes on the money. When you make a contribution to a traditional account you normally would be able to deduct that amount from your taxable income, which would reduce your taxable income the year you make the contribution. Then at retirement when you withdraw the money, you would pay taxes on the contributions and growth of the account. This is called tax-deferred money since you are deferring the taxes until later

A Roth account works the opposite way. You do not reduce your taxable income the year you contribute the money, but then when you withdraw the money you do not have to pay taxes since you already paid them on the money contributed. This is called tax-free money since it is tax-free upon withdrawal.

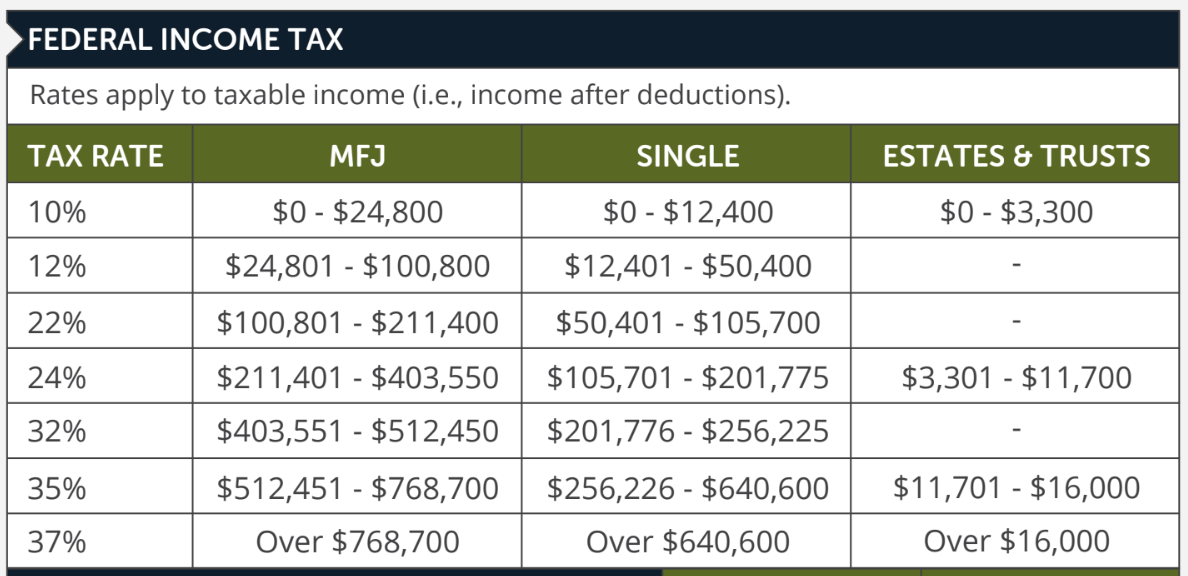

2026 Income Tax Brackets

One of the first things you will want to figure out is what federal income tax bracket you will be in for the current tax year. This is an important part of your decision when deciding if you should contribute to a traditional or a Roth account. Here are the federal income tax brackets for 2026.

If you are in one of the higher income tax brackets (32%, 35%, or 37%) it may make sense to contribute to a traditional instead of a Roth account since you would save more now on taxes than you would if you were in one of the lower income tax brackets (10%, 12%, 22%). If you think you are in a higher tax bracket now and will be in a lower tax bracket at retirement, then it may make sense to contribute to a traditional instead of a Roth account. Keep in mind that politicians have adjusted the tax brackets many times in the past and will probably adjust them again before you reach retirement.

Time Horizon

Time until retirement is another factor to consider when making your decision. Generally, someone who is younger will have a lot more time for their money to earn compound interest and could be better off contributing to a Roth account. This way all of the principal & compound interest they withdraw at retirement would be tax-free, whereas if it was in a traditional account you would owe taxes on that money instead. My brother explains it as “would you rather pay taxes on the seeds or pay taxes on the entire tree once it is fully grown.”

You might be someone who would rather lock in their tax rate now and not have to worry about if it will be higher or lower at retirement. If you are that type of person then you will want to consider contributing to a Roth account. If you are someone who believes your tax rate at retirement will be lower than what it is currently, then you will want to consider contributing to a traditional account.

Required Minimum Distributions

Required Minimum Distributions (RMDs) are another reason why you might decide to contribute to a Roth instead of a traditional account. After a certain age (as of 2022 it is 72) the government requires that you withdraw a specified amount of money every year from your accounts as they want to get their tax money back on that tax-deferred money. If you have that money in a Roth IRA then there are no RMDs, unless it is an inherited Roth IRA. (Source; Fidelity; link below)

Employer Plans

If you participate in a retirement plan at work, most companies offer some type of matching program. If you contribute a certain amount they will contribute a match. Dollar on the dollar or fifty cents on the dollar up to a certain amount appears to be the most common matching contributions. More employers are now offering a Roth option. If you elect to have your contributions go toward the Roth bucket be aware that your employer will more than likely contribute their match into the traditional bucket, so they are able to receive the tax deduction. This may be a good thing as it could help you diversify your risk by having some money tax-deferred and some money tax-free at retirement.

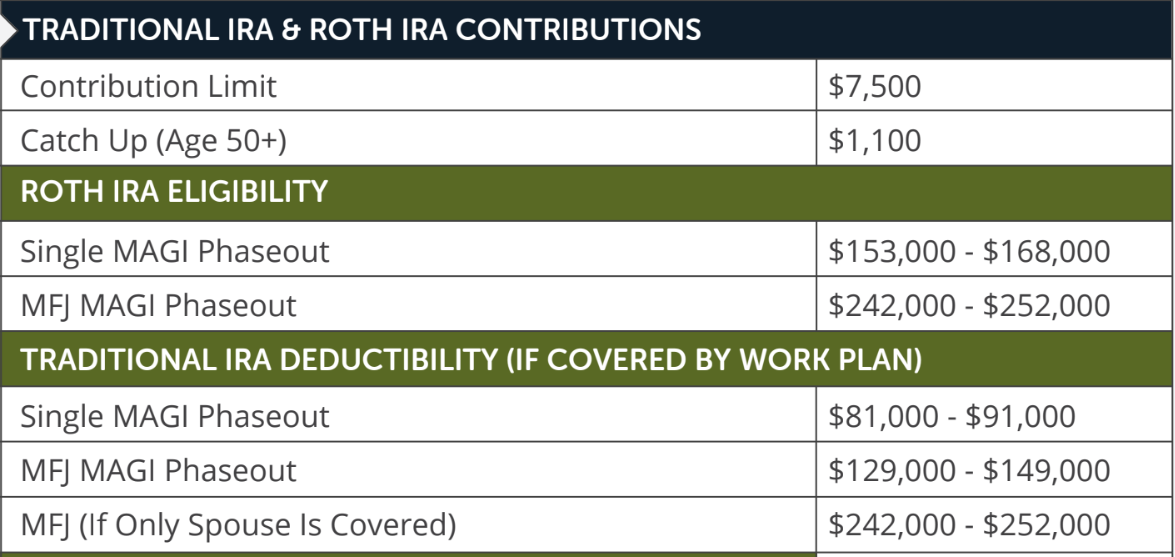

If you are a participant in an employer-sponsored retirement plan at work, then there is a deductibility phase-out for IRAs if your modified adjusted gross income (MAGI) is above a certain amount. In other words, you wouldn’t get the tax deduction by contributing to a traditional IRA plan if your income is over a certain amount and you have a retirement plan at work. For Roth IRA’s there is a phase-out limit. As your MAGI increases, the amount the IRS allows you to contribute decreases until you are no longer allowed to contribute. Here are the limits for the 2026 tax year.

If you have more questions about if you should contribute to a Roth or a traditional account feel free to set up a meeting with me as I am happy to discuss strategies personalized to your situation. If you are looking for the best of both traditional and Roth accounts then click here to learn more about how Health Savings Accounts can be used as a stealth retirement account.

Sources: https://www.kiplinger.com/retirement/retirement-plans/roth-iras

https://www.fidelity.com/building-savings/learn-about-iras/required-minimum-distributions/overview

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.