Financial Wellness Isn't Optional, It's Foundational

You track your steps. You hit the gym. You meal prep. You've mastered the wellness routines that optimize your physical and mental health. But there's one dimension of wellness you might be overlooking.

The Hidden Health Crisis No One Talks About

Money is the leading factor negatively affecting Americans' mental health, ahead of politics, world news, climate change, and even physical health concerns.4 Let that sink in for a moment.

The statistics paint a sobering picture:

Nearly 70% of Americans say financial uncertainty has made them feel depressed and anxious, an 8-percentage point increase from just two years ago 9

Over 50% of Americans feel stressed or anxious about their finances multiple times per week, with overall financial stress intensity rated at 3.2 out of 5 2

83% of Americans report financial stress driven by inflation, rising living costs, and recession concerns7

56% say financial stress affects their sleep, 55% their mental health, 50% their self-esteem, 44% their physical health, and 40% their relationships at home 5

Perhaps most troubling: 60% of people have avoided seeking mental health care due to financial constraints. 7 The very stress that's damaging their wellbeing prevents them from getting help.

This isn't just about feeling worried. Nearly 4 in 10 Gen Z and Millennials report feeling depressed and anxious on at least a weekly basis due to financial uncertainty. 9 Financial stress has become a chronic condition, one that compounds over time if left untreated.

Why Financial Wellness Gets Left Behind

You probably wouldn't hesitate to invest in a gym membership, therapy, or organic groceries. These feel productive, healthy, empowering (right?). But financial planning? Why does that feel overwhelming, complicated, shameful, or uncomfortable?

Here's the reality: We often learn our money mindset from our families. You likely absorbed attitudes, fears, and behaviors about money long before you understood what money actually was. Many of those patterns may not be serving you anymore, but they could still be running in the background, influencing your financial decisions. (These are sometimes called "money scripts," a whole topic we could explore another time.)

And unlike organizing your closet or meal prepping for the week, you may not see the results of financial planning immediately. There's no before-and-after photo. No dopamine hit from a perfectly labeled container.

That's probably why only 48% of Americans have emergency funds that would cover three months of expenses, even though this is considered the baseline for financial security.3 It may also explain why nearly 1 in 4 households lived paycheck to paycheck in 2025, despite total household debt reaching $18.59 trillion.6

What True Financial Wellness Actually Looks Like

Financial wellness isn't about making as much money as possible. It's about using money as a tool to make your overall life better.

It means:

Financial security - The ability to handle an emergency without panic

Strategic debt management - A manageable debt load skewed toward "good" debt like a mortgage, not high-interest credit cards crushing your monthly budget

Aligned spending - Money flowing to the right places at the right times, supporting what matters most to you

Freedom from anxiety - Confidence that you're making sound decisions, not constant worry about what you might be missing

This isn't about restriction. It's about abundance. Making conscious choices that create the life you actually want to live.

The Money Mindset Shift That Changes Everything

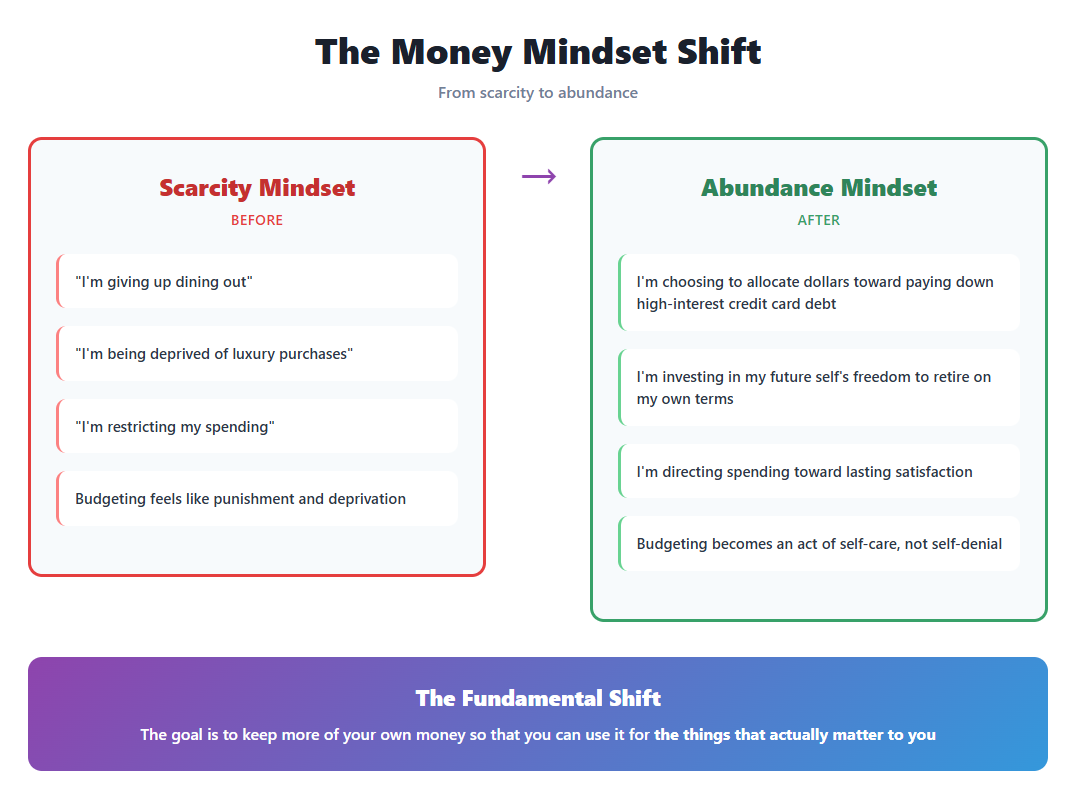

Most people approach budgeting as punishment. A list of things they can't have. A constant reminder of scarcity.

But here's the reframe: Your goal is to spend as much of your money as possible over the course of your life (on the things that actually matter to you).

Budgeting, saving, and investing are simply techniques to smooth out spending across earning years and non-earning years. The purpose isn't deprivation, it's ensuring your lifestyle remains at the level you want, both now and in retirement, while avoiding the trap of high-interest debt that can sabotage your financial future.

This shift from scarcity to abundance mindset transforms everything:

You're not "giving up" dining out. You're choosing to allocate those dollars toward paying down that 21% credit card balance6that's costing you thousands in interest

You're not being "deprived" of luxury purchases. You're investing in your future self's freedom—whether that's eliminating debt, taking a sabbatical, or retiring early

You're not "restricting" your spending. You're directing it toward what brings you lasting satisfaction instead of fleeting dopamine hits that often end up on high-interest credit cards

When you understand this, budgeting becomes an act of self-care, not self-denial.

Breaking the Silence: Why Talking About Money Matters

Money remains one of our last cultural taboos. We'll discuss our relationships, our therapy sessions, our trauma, but our credit card debt? Our salary? Our fear that we're falling behind? Those topics remain off-limits.

This silence keeps you stuck.

The majority of people whose mental health is negatively impacted by money cite inflation and rising prices as the culprit 4, but they're likely suffering alone, convinced everyone else has it figured out.

In relationships, financial silence is toxic. Shame over debt or unequal wealth sabotages progress toward shared goals. One partner quietly panics while the other remains oblivious. Resentment builds. Trust erodes. (An objective third party could help navigate these conversations, right?)

In friend groups, financial transparency creates both reassurance and knowledge. How did they handle that situation? What professionals helped them? What strategies actually worked? This information is invaluable, but only if people are willing to share it.

The irony? 78% of Gen Z say financial responsibility is an important attribute when choosing a significant other, and 66% don't feel pressured by friends to spend beyond their means.8 The younger generation is already normalizing these conversations. It's time the rest of us catch up.

The Six Pillars You Can't Afford to Ignore

Financial wellness isn't about mastering one thing. It's about creating a comprehensive system across six critical areas:

1. Cash Flow & Emergency Planning

Beyond just "spending less than you earn," this means understanding your patterns, optimizing your savings rate, and maintaining 3-6 months of living expenses for true emergencies. Only 20% of lower-income adults report being in excellent or good financial shape currently, 1 but this isn't about income level. It's about having a plan.

2. Strategic Debt Management

The average credit card interest rate crossed 21% in 2025, making high-interest debt incredibly expensive.6 Should you consolidate? Pay down aggressively? Use a home equity loan? The answers depend on your specific situation and goals.

3. Investment Strategy

Your portfolio should reflect your timeline, goals, and risk tolerance, not last quarter's hot stock. Are you properly diversified? Are tax implications part of your strategy? Research from major financial institutions consistently shows that diversification across asset classes reduces portfolio volatility and risk without necessarily sacrificing returns.12

4. Multi-Year Tax Planning

This isn't about filing your return. It's about maximizing tax-advantaged accounts, planning for retirement distributions, and, if you're a business owner, structuring your affairs for maximum efficiency. While the tax code is complex, strategic planning could help optimize your tax situation.

5. Comprehensive Risk Management

Health insurance, life insurance, disability coverage, umbrella policies, and long-term care: each serves a different purpose. 27% of adults had trouble paying for medical care in the past year.3 The right insurance protects you from catastrophic financial loss.

6. Estate Planning

Who cares for your children if something happens to you? Who makes healthcare decisions? How do your assets transfer, and what are the tax implications? These aren't comfortable conversations, but they're essential ones.

Why Going It Alone Isn't Working

You likely know much of this intellectually. You probably understand you should have a budget, pay down debt, invest for retirement, get proper insurance, and create an estate plan.

But here's what the research shows about people who try to do it themselves:

They make expensive mistakes. Behavioral mistakes may reduce wealth significantly.15 Common errors include market timing, panic selling during downturns, chasing performance, and failing to rebalance portfolios systematically.

They let emotions drive decisions. Behavioral mistakes may reduce wealth significantly.15 When markets drop, panic sets in. When they soar, greed takes over. Both can undermine long-term returns.

They don't know what they don't know. Tax strategies, estate planning nuances, insurance gaps, investment allocation. These are complex domains where missteps can have long-term consequences.

They run out of time and energy. U.S. employees 56% spend 3 or more work hours per week dealing with personal financial issues.5

The Measurable Value of Professional Guidance

The financial advice industry has been rigorously studied. The data is clear and consistent:

Leading research from Vanguard, Morningstar, and Russell Investments has examined the potential value professional advisors may add through their "Advisor's Alpha" and "Gamma" frameworks.10,17,13These studies explore how tax optimization, behavioral coaching, strategic asset location, disciplined rebalancing, and comprehensive planning could contribute meaningful value over time by supporting better decision-making and helping clients avoid costly mistakes.

Beyond portfolio optimization:

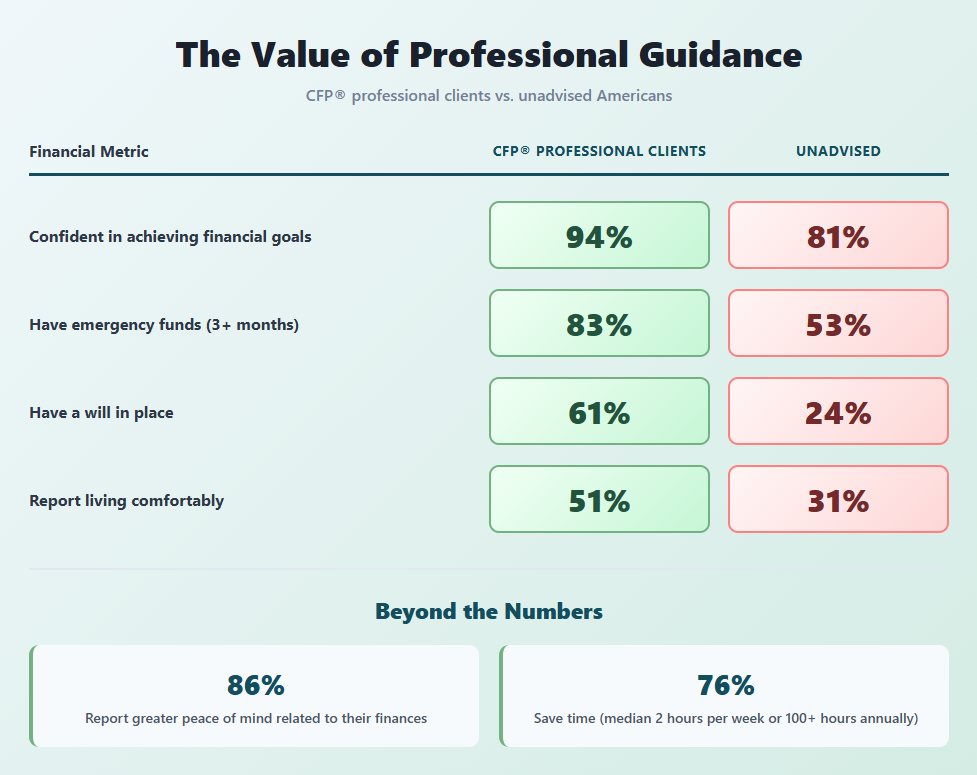

94% of households advised by CFP® professionals feel confident in their ability to achieve their financial goals, compared to 85% of those working with other advisors and 81% of unadvised Americans.11

CFP® professional clients are significantly more prepared: 83% maintain emergency funds covering three months of expenses (versus 68% with other advisors and 53% unadvised), and 61% have a will in place (versus 46% with other advisors and 24% unadvised).11

Half (51%) of people who work with a CFP® professional report living comfortably, compared to 40% with other advisors and 31% of unadvised households.11

Advised investors report greater peace of mind related to their finances: 86% feel more peace of mind, with 60% experiencing less anxiety, worry, sadness, and disappointment, and instead feeling more confident, satisfied, secure, and proud.16

Working with an advisor may also save time: 76% report time savings, with a median of two hours per week (over 100 hours annually) that can be redirected toward activities like leisure, time with family, and exercise.16

The Emotional ROI You Can't Ignore

Over half of consumers who work with CFP® professionals report that financial advice positively impacted their mental health and family life.11 Given the financial stress we discussed earlier, consider what addressing it might mean: the potential for better sleep, less anxiety, improved relationships, greater confidence, and more time with your family.

Research also shows that clients of CFP® professionals report higher quality of life scores compared to those who work with other financial planning professionals or manage finances independently.11 Investors with human advisors perceive meaningful progress toward their financial goals compared to managing finances on their own.14

This isn't just about money. It's about reclaiming your mental bandwidth, your emotional energy, and your time.

Can you quantify peace of mind? Can you put a price on knowing you've made sound decisions that keep your goals on track? Can you measure the value of not lying awake at 3 AM worrying about money?

The Real Cost of Waiting

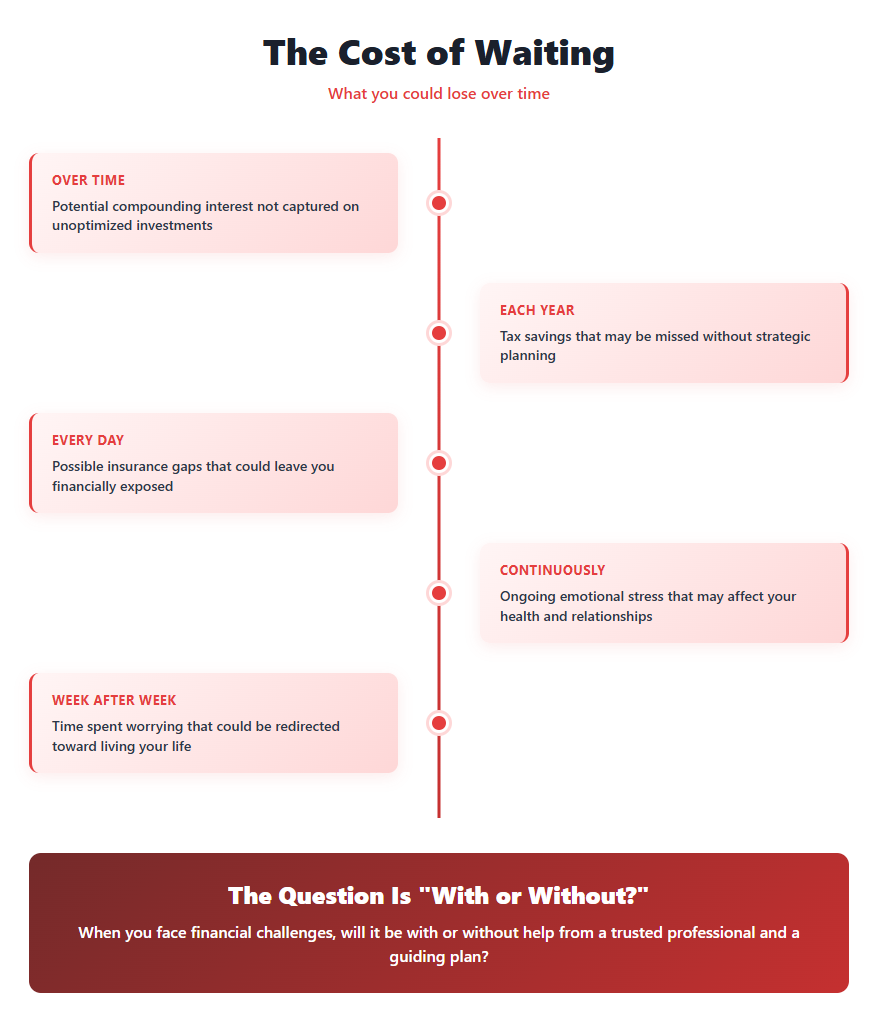

Each month without a comprehensive financial plan may mean:

Potential compounding interest not captured

Tax savings that may be missed

Possible insurance gaps that could leave you exposed

Ongoing emotional stress that may affect your health and relationships

Time spent worrying that could be redirected toward living your life

Near the end of 2024, only 73% of adults reported doing okay financially or living comfortably, down from 78% in 2021.1 The trend suggests challenges for many Americans.

Meanwhile, 28% of adults expect their financial situation to be worse a year from now, up significantly from 16% who said this in 2024.3

The environment presents ongoing challenges: inflation, rising costs, economic uncertainty. The question is whether you'll face them with a plan or without one.

What Makes Financial Wellness Different From Every Other Form of Organization

When you organize your closet, you feel satisfied for a few weeks. Then life happens, and you're back to chaos.

When you establish financial wellness with a competent advisor, you create a system that:

Compounds over time with ongoing adjustments rather than constant upkeep

Adapts to your life instead of becoming obsolete

Streamlines future decisions rather than adding complexity

Builds on itself instead of needing to start from scratch

A good financial advisor should quarterback your entire financial life, not just help you create a budget. This means coordinating your investments, taxes, insurance, and estate plan. Working with your CPA and attorney to ensure nothing falls through the cracks. Monitoring and adjusting as markets change, laws change, and your life changes.

If your current advisor isn't providing this level of comprehensive guidance, it may be worth considering whether you're getting the value you deserve.

Most importantly, the right advisor should transform financial planning from a source of anxiety into a source of confidence.

From Overwhelmed to In Control: What Working Together Looks Like

If you're thinking, "I need to do something about this," here's what taking action actually involves:

Step 1: An Honest Conversation

No judgment, no sales pressure. Just a candid discussion about where you are, where you want to be, and what's standing in your way. Many people find this conversation provides helpful clarity as a starting point.

Step 2: Comprehensive Assessment

We examine all six pillars of financial wellness together. Where are the opportunities? Where are the vulnerabilities? What's working, and what's quietly undermining your goals?

Step 3: Your Customized Plan

Not a template. Not generic advice. A written financial plan that addresses your specific circumstances, values, and goals, with clear action steps and realistic timelines.

Step 4: Implementation & Ongoing Partnership

You don't get a binder to put on a shelf. Your advisor helps you execute the plan, automate what can be automated, and adapt as your life evolves (by the way, this is how I work with clients). Regular check-ins ensure you stay on track and adjust course when needed.

This is what financial wellness actually looks like: not perfect budgets that fail after two weeks, but sustainable systems that support the life you want to live.

The Bottom Line: Financial Wellness Is Wellness

You can't exercise your way out of financial stress. You can't hydrate your way to retirement security. You can't sleep your way to financial freedom (especially if you're stressed about your finances 5). And ignoring it won't make it disappear.

Physical health, mental health, and financial health are interconnected. 73% of clients who work with CFP® professionals generally feel they can cope well with any health issues compared to 64% of unadvised consumers.11 Financial wellness doesn't just reduce money stress: it makes you more resilient across all areas of life.

The cultural narrative tells you that needing help with money is a sign of failure. That's backwards.

You wouldn't think twice about hiring a trainer to optimize your physical health or a therapist to support your mental health. Your financial health deserves the same level of professional attention, especially since it impacts other dimensions of your wellbeing.

Your Next Step

Financial wellness isn't about having definitive answers. It's about asking the right questions and working with someone who can help you find answers that fit your life.

The choice isn't between managing everything yourself or delegating everything to someone else. It's between struggling alone with uncertainty or partnering with a professional who can provide clarity, strategy, and peace of mind.

Ready to make financial wellness part of your overall wellbeing?

Schedule your complimentary financial wellness consultation (below)

Let's transform financial stress into financial confidence, together.

Sources and References

Federal Reserve. (2025). Report on the Economic Well-Being of U.S. Households in 2024. https://www.federalreserve.gov/publications/2025-economic-well-being-of-us-households-in-2024-overall-financial-well-being.htm

Motley Fool Money. (2024). Financial Stress, Anxiety, and Mental Health Survey. https://www.fool.com/money/research/financial-stress-anxiety-and-mental-health-survey/

Pew Research Center. (2025). More Americans now say personal finances will be worse a year from now. https://www.pewresearch.org/short-reads/2025/05/07/growing-share-of-us-adults-say-their-personal-finances-will-be-worse-a-year-from-now/

Bankrate. (2025). Money and Mental Health Survey. https://www.bankrate.com/banking/money-and-mental-health-survey/

PwC. (2023). Employee Financial Wellness Survey. https://www.pwc.com/us/en/services/consulting/business-transformation/library/employee-financial-wellness-survey.html

CoinLaw. (2025). Household Financial Stress Statistics 2025. https://coinlaw.io/household-financial-stress-statistics/

LifeStance Health. (2025). 2025 Study: How Financial Stress ("Stressflation") Impacts Americans' Mental Health. https://lifestance.com/insight/financial-stress-impact-mental-health-statistics-2025/

Bank of America. (2025). Better Money Habits Financial Education Study. https://newsroom.bankofamerica.com/content/newsroom/press-releases/2025/07/confronted-with-higher-living-costs--72--of-young-adults-take-ac.html

Northwestern Mutual. (2025). Planning & Progress Study. https://news.northwesternmutual.com/2025-06-03-Nearly-70-of-Americans-Say-Financial-Uncertainty-Has-Made-Them-Feel-Depressed-and-Anxious,-According-to-Northwestern-Mutual-2025-Planning-Progress-Study

Vanguard. Putting a Value on Your Value: Quantifying Vanguard Advisor's Alpha. https://advisors.vanguard.com/advisors-alpha

CFP Board. (2026). Trust. Confidence. Impact: 2025 Financial Planning Longitudinal Study. https://www.cfp.net/news/2026/01/cfp-professional-advised-americans-experience-greater-financial-preparedness

Vanguard. Framework for Constructing Globally Diversified Portfolios. https://investor.vanguard.com/investor-resources-education/portfolio-management/diversifying-your-portfolio

Russell Investments. Value of an Advisor Study. Referenced in multiple industry analyses of advisor value-add through holistic financial planning.

Vanguard. Why Clients Prefer Financial Advisors Over Robo Advisors. https://advisors.vanguard.com/advisors-alpha/advice-that-clients-value

Covenant Wealth Advisors. (2025). The True Value of a Financial Advisor: What You Need to Know. https://www.covenantwealthadvisors.com/post/value-of-a-financial-advisor-what-you-need-to-know

Vanguard. (2025). Advice Pays in Peace of Mind and Time. https://corporate.vanguard.com/content/corporatesite/us/en/corp/who-we-are/pressroom/press-release-advice-pays-in-peace-of-mind-and-time-vanguard-survey-reveals-hidden-value-of-financial-advice-07072025.html

Blanchett, D. and Kaplan, P. (2013). Alpha, Beta, and Now...Gamma. Morningstar. https://www.morningstar.com/financial-advisors/gamma-action

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark in the United States, which it authorizes use of by individuals who successfully complete CFP Board's initial and ongoing certification requirements.