The True Value of Professional Investment Management: Why It's Not About Beating the Market

TL;DR

Professional investment management isn't about beating the market, it's about making better decisions consistently. Research suggests advisors may add value over time through areas such as implementation, rebalancing, behavioral coaching, tax considerations, and withdrawal planning; the magnitude and timing of any benefit varies by investor and market conditions. The biggest value? Preventing costly emotional mistakes during market extremes. Even capable DIY investors often benefit from professional guidance while freeing time for what they actually enjoy.

Interested in exploring whether professional management might add value? Let's discuss your goals, current approach, and whether we might work well together.

Note: "bps" = basis points. See explanation below.

What Actually Motivates People to Hire Advisors?

Dimensional Fund Advisors research identified four reasons families hire advisors:¹

"I need help, I don't know what I'm doing." Financial management is complex.

"I need accountability." Humans make expensive mistakes during market extremes.

"I don't want to spend time on this." Even capable people prefer allocating time elsewhere.

"I want my spouse involved in our financial decisions." Equal partnership in money matters is critical.

Notice what's missing? "I want someone who can beat the market."

"I Don't Want to Spend Time on This"

Even if you possess every skill needed to manage investments effectively, you might reasonably prefer not to. Your time and mental energy may be better spent elsewhere.

Investment management might rank between "tedious chore" and "necessary evil" on your preferred activities list. Your calendar already bursts with obligations. Or perhaps having one partner shoulder the entire investment burden creates uncomfortable dynamics.

What if you could build a relationship with a trusted financial professional and simply know it's handled competently?

While you might be capable of DIY investing, choosing not to is valid.

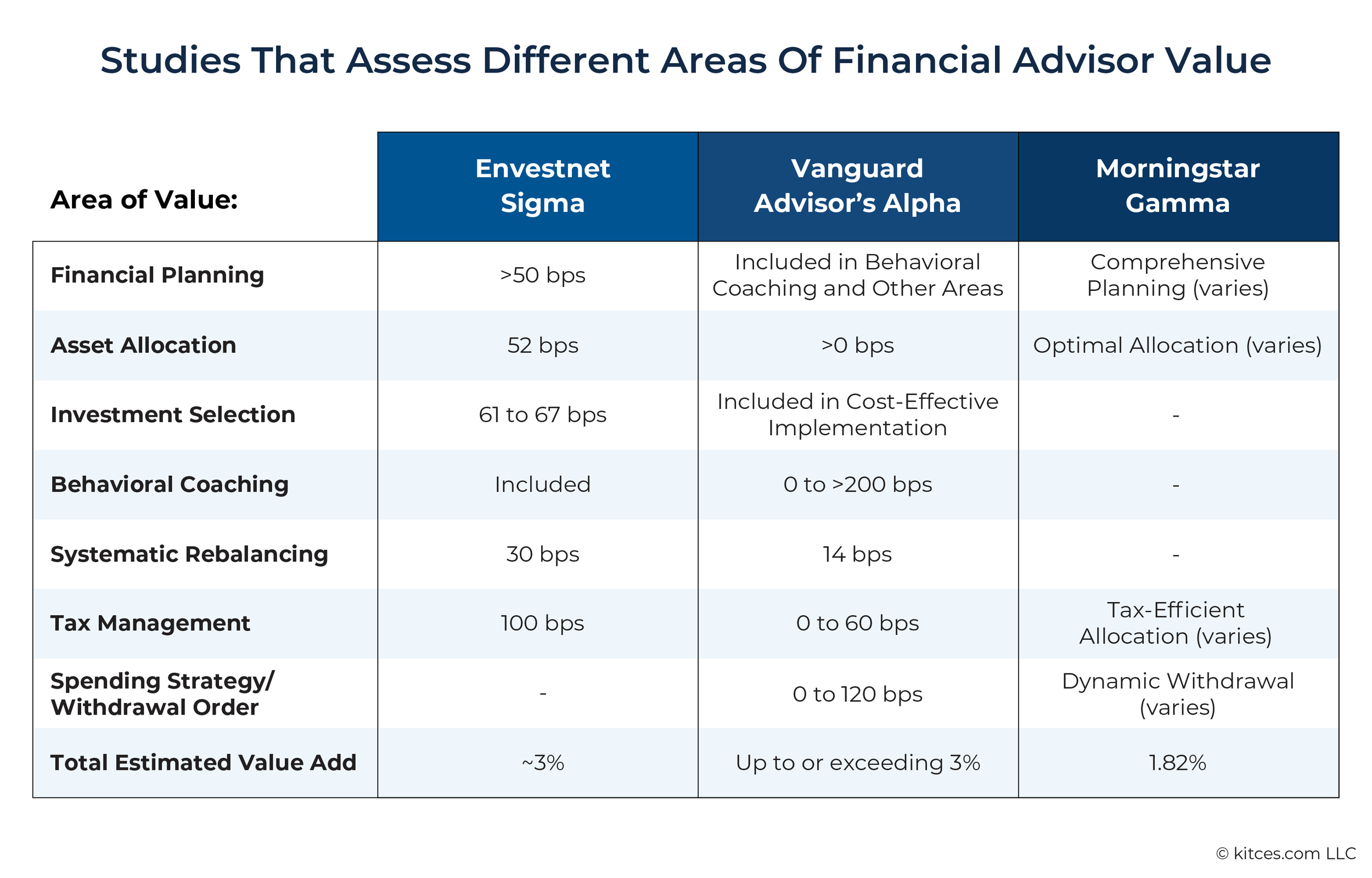

The Research: Quantifying Adviser's Alpha

Vanguard research suggests that following certain practices may improve investor outcomes over time, though results vary and are not consistent year to year.2 This isn't predictable annual outperformance, it's irregular value-add peaking when investors are most tempted to abandon well-designed plans.

Investment management encompasses vastly more than choosing funds. The real value lies in everything around those choices.

A Quick Note on Basis Points

"Basis points" (bps) measure small percentages:

1 basis point = 0.01%

100 basis points = 1%

So "~150 basis points" means approximately 1.5% annually. "34-70 basis points" means 0.34% to 0.70%.

Why use basis points? These small differences compound dramatically over decades. A 50 basis point (0.50%) annual advantage can mean tens or hundreds of thousands of dollars over 30 years.

The Four Pillars of Value

Dimensional organizes the value proposition into: Competence, Coaching, Convenience, and Continuity.¹

1. Competence: Technical Expertise That Matters

Cost-Effective Implementation

Average investors pay 57-79 bps annually in fund expenses. Those using low-cost funds pay just 16-20 bps. This 34-70 bps differential compounds relentlessly over decades.³

Understanding Your Portfolio Composition

Many investors contributing for years without a coherent philosophy end up with suboptimal portfolios. The most common pattern I see: significant overconcentration in the S&P 500 through multiple index funds, target-date funds that hold S&P exposure, and individual holdings that overlap with the index.

When we review these portfolios, clients often realize for the first time that they have virtually no exposure to smaller U.S. companies, international markets, or meaningful fixed income allocation. Everything is essentially the same 500 large-cap U.S. stocks, held multiple times across different accounts.

Your portfolio's composition (asset allocation and market exposure) is your returns' primary driver. It's about intentionally accessing different sources of expected return across size (large vs. small), geography (U.S. vs. international vs. emerging), and asset classes (stocks vs. bonds vs. real estate).

Heavy concentration in the S&P 500 is an implicit bet that large-cap U.S. stocks will keep outperforming everything else. That might work. Or not. But it should be conscious, not accidental.

Beyond knowing what you own, you need to know why. Your investment strategy should connect directly to actual financial goals.

We examine both sides: return drivers (asset allocation, market exposure, emphasizing higher expected return areas) and cost drags (implementation costs, taxes, expense ratios). We evaluate every holding: keep, sell, or donate, ensuring each serves a deliberate purpose aligned with your timeline and goals.

Your net returns come from assembling these components thoughtfully. Not just picking "best" funds, but how everything works together.

Converting Idle Cash Into Working Capital

Cash accumulation where it shouldn't be is widespread: substantial balances in checking/savings without purpose, RSU proceeds languishing, or money transferred to investment accounts but never deployed. We systematically review and invest these idle positions.

Disciplined Rebalancing: 14-30 Basis Points

Market movements push portfolios from target allocations. A portfolio designed with a certain stock/bond mix will naturally drift as different asset classes perform differently. Rebalancing primarily controls risk.⁴ A portfolio that's drifted to hold more stocks than intended has taken on more volatility and downside exposure than originally planned.

The challenge? Rebalancing is psychologically uncomfortable, selling winners and buying losers when instincts scream otherwise.

Calibrating Risk to Timeline

Risk is the probability of insufficient funds when needs arise. Someone purchasing a home in five years needs dramatically different allocation than someone two decades from retirement.

We construct appropriate equity/fixed income/cash combinations based on your timeline and risk tolerance. Vanguard research shows simple portfolios (like 60/40 index funds) deliver returns comparable to complex endowment portfolios.⁵ Simplicity has genuine advantages.

Tax Optimization: 0-100 Basis Points

The goal: minimize lifetime tax burden, not this year's bill. Sometimes accepting higher current taxes positions you for dramatically lower lifetime taxes.

Strategies include:⁶

Strategic asset placement (tax-efficient equities in taxable accounts, bonds in retirement accounts)

Loss harvesting during declines

Gain harvesting during low-income years

Replacing tax-inefficient funds

Donating appreciated securities versus cash

Retirement Withdrawal Strategies: 0-120 Basis Points

For retirees with multiple account types, withdrawal order significantly impacts lifetime taxes. Informed strategies add 0-153 bps annually while extending portfolio longevity.⁷

And Many More

Research suggests over 100 distinct ways advisors add value across planning domains.¹³ Effective advisors go deep on services most relevant to their clients' needs.

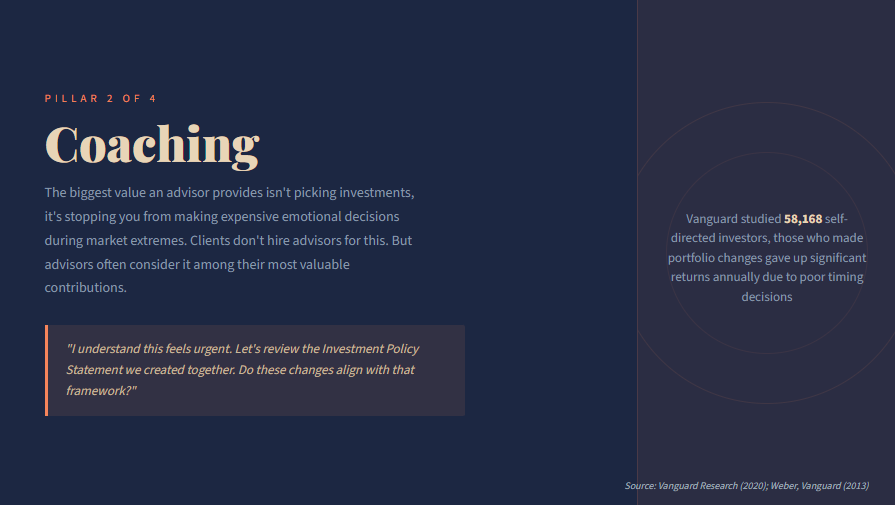

2. Coaching: The Behavioral Advantage (The Biggest Value-Add)

Behavioral coaching potentially adds up to 200 basis points annually, the single most valuable service advisors provide.⁸

Here's a paradox: clients don't hire advisors for emotional guidance. Yet advisors recognize this as among our most valuable contributions.

Vanguard analyzed 58,168 self-directed investors: those who made portfolio changes sacrificed 104-150 bps due to poor market timing.⁹ European analysis revealed investors consistently underperforming their own fund holdings, a persistent "behavior gap."¹⁰

The pattern: when markets surge, investors extrapolate gains indefinitely and increase risk. When markets crash, fear drives capitulation at exactly the wrong moment.

An advisor's function during these periods is rational perspective: "I understand this feels urgent. Let's review the Investment Policy Statement we created together. Do these changes align with that framework?"

Clients engage advisors not from lack of intelligence, but recognizing the value of accountability.¹¹ Advisors aren't immune to emotion, we've developed systematic processes prioritizing rational analysis over emotional reaction.

Building relationships before market extremes enables advisors to function as behavioral circuit breakers.

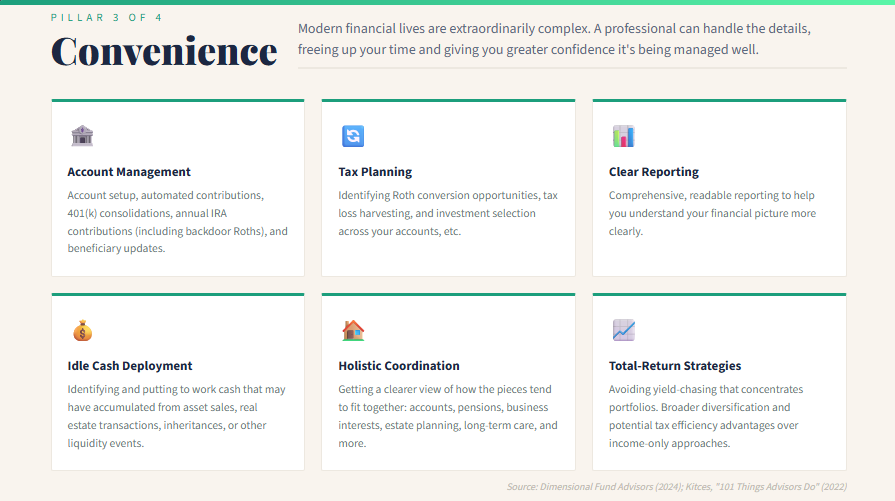

3. Convenience: Integrated Management and Peace of Mind

Modern financial lives are extraordinarily complex: multiple accounts, former employer plans, pensions, business interests, estate planning, tax optimization, long-term care.

Families engage advisors to spend time with family rather than managing portfolios, gain professional oversight, ensure continuity for spouses/children, and have someone seeing how all pieces fit together.

Navigating Administrative Complexity

We help navigate (often handling directly) tasks like: account establishment, automated contributions, 401(k) consolidation, Roth conversions, annual IRA contributions including backdoor Roths, investment selection in employer plans/HSAs, beneficiary updates, trust funding, among many other administrative details that would otherwise consume your time and attention.

Clear, Comprehensive Reporting

Quality reports help you understand your portfolio without needing an advanced degree.

Total-Return vs. Income-Only Strategies

With suppressed bond yields, many retirees' portfolios don't generate sufficient income. The temptation: chase yield through high-yield bonds or dividend strategies.

The problem? These typically concentrate portfolios, reduce diversification, and often expose principal to greater risk than disciplined total-return strategies.¹²

Total-return approaches (considering both income and appreciation) can provide broader diversification, potential tax efficiency advantages, and may support portfolio sustainability depending on the investor’s circumstances.

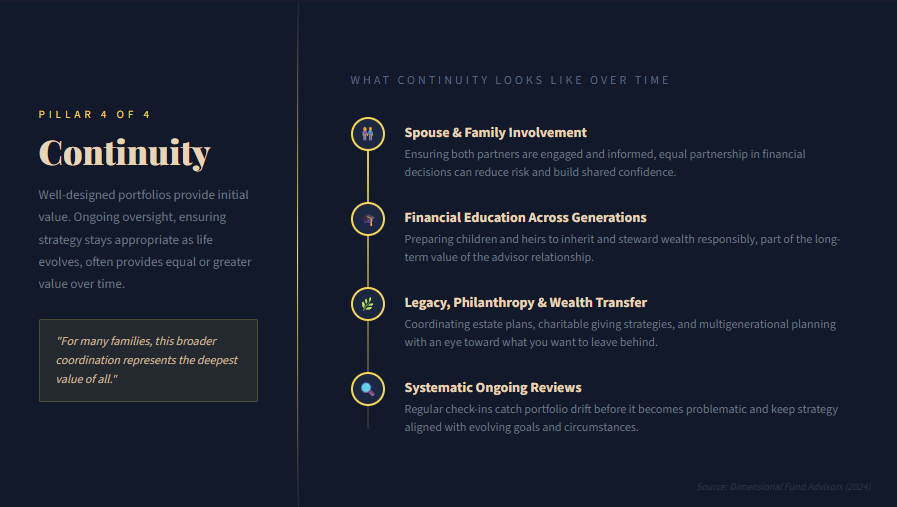

4. Continuity: Family, Legacy, and Multigenerational Planning

Professional advisors facilitate spouse involvement, children's financial education, wealth transfer, philanthropy, multigenerational planning, and legacy creation.

For many families, this broader coordination represents the deepest value.

Systematic Ongoing Reviews

Well-designed portfolios provide initial value. Ongoing oversight ensuring strategy remains appropriate, provides equal or greater value over time. Regular reviews catch drift before it becomes problematic.

The Quantified Value

Research shows:

Value varies by circumstances, but cumulative effects meaningfully improve outcomes.²

The Bottom Line

The true value isn't about "delivering" returns or picking winning stocks.

It's about making better decisions consistently, avoiding behavioral mistakes during emotional moments, creating clarity amid complexity, ensuring money serves your goals, maintaining discipline when instincts scream otherwise, and handling administrative minutiae.

Investment selection is part of professional management. But comprehensive planning, behavioral coaching, tax optimization, administrative execution, and coordinated oversight typically create the most significant impact.

The question isn't "Can I manage investments myself?"

It's: "Would I make consistently better decisions (and feel genuinely confident) with a professional partner? Would I rather spend my time and energy on things I enjoy?"

For many, research and experience strongly suggest yes. And unlike beating the market, those are areas where we aim to provide support and a disciplined process, based on each client’s circumstances.

Interested in exploring whether professional management might add value? Let's discuss your goals, current approach, and whether we might work well together.

Sources and References

¹ Lupescu, Apollo. "Communicating the Value of Your Advice." Dimensional Fund Advisors Applied Communications Workshop, November 13, 2024.

² Kinniry, Francis M. Jr., Colleen M. Jaconetti, Michael A. DiJoseph, Yan Zilbering, Donald G. Bennyhoff, and Georgina Yarwood. "Putting a Value on Your Value: Quantifying Adviser's Alpha." Vanguard Research, June 2020.

³ Ibid. Analysis based on asset-weighted expense ratios across mutual funds and ETFs available in Europe as of December 31, 2019.

⁴ Ibid. Vanguard research on portfolio rebalancing showing value-add of 26-86 basis points depending on market conditions and geography.

⁵ Based on 2019 NACUBO-Commonfund Study of Endowments, as cited in Kinniry et al., "Putting a Value on Your Value: Quantifying Adviser's Alpha."

⁶ Kinniry et al., "Putting a Value on Your Value: Quantifying Adviser's Alpha." Asset location value-add ranges from 0-110 basis points depending on jurisdiction and individual circumstances.

⁷ Harbron, Garrett L., Warwick Bloore, and Josef Zorn. "Withdrawal Order: Making the Most of Retirement Assets." Vanguard Research, 2019, as cited in Kinniry et al.

⁸ Kinniry et al., "Putting a Value on Your Value: Quantifying Adviser's Alpha." Behavioral coaching estimated at approximately 150 basis points annually.

⁹ Weber, Stephen M. "Most Vanguard IRA Investors Shot Par by Staying the Course: 2008–2012." Vanguard Research, 2013, as cited in Kinniry et al.

¹⁰ Kinniry et al., "Putting a Value on Your Value: Quantifying Adviser's Alpha." Analysis of European investor returns versus fund returns showing median negative gaps across categories.

¹¹ Bennyhoff, Donald G. "The Vanguard Adviser's Alpha Guide to Proactive Behavioural Coaching." Vanguard Research, 2018, as referenced in Dimensional Fund Advisors communications.

¹² Kinniry et al., "Putting a Value on Your Value: Quantifying Adviser's Alpha." Discussion of total-return versus income-only investing strategies for retirees.

¹³ Van Deusen, Adam. "101 Things That Advisors Actually DO To Add Value (Beyond Just Allocating A Portfolio)." Kitces.com, November 28, 2022. Available at: https://www.kitces.com/blog/advisors-add-value-proposition-financial-planning-ideal-clients-target-persona-differentiation/

¹⁴ Tharp, Derek. "Quantifying (More Accurately) The Real Impact Of A Financial Advisor's Costs On Their Clients' Nest Eggs." Kitces.com, October 23, 2024. Available at: https://www.kitces.com/blog/financial-advisor-costs-fees-aum-fee-only-high-new-worth-ramit-sethi-facet/

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark in the United States, which it authorizes use of by individuals who successfully complete CFP Board's initial and ongoing certification requirements.