You Have Company Stock. Now What?

RSUs, stock options, and why the thing stopping most people isn’t knowledge. It’s inertia.

If you have RSUs vesting every quarter and stock options you’ve been meaning to deal with, you’re probably overdue for a plan. (You probably know that already).

This post covers the key tax rules, a three-part framework for deciding what to do with a concentrated position, and the one thing that stops most people from following through even when they know exactly what they should be doing.

The framework works whether your concentration came from equity comp, stock purchases, or inheritance. And it’s worth noting upfront: equity is rarely the only moving piece in someone’s financial life. A plan that accounts for all aspects of your finances is likely to result in a better outcome than one that treats the stock in isolation.

The Tax Rules, Without the Jargon (OK, Maybe There Is Some Jargon After All)

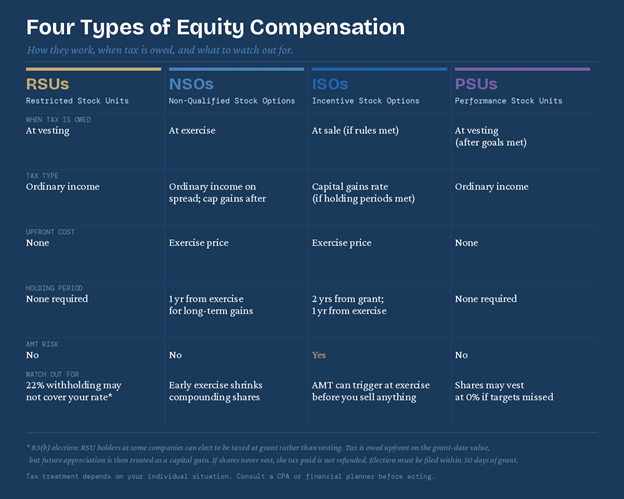

Figure 1: RSUs, NSOs, ISOs, and PSUs side by side. When tax is owed, what type of tax applies, and what to watch out for.

When RSUs vest, income tax is triggered on whatever they’re worth on that day, whether you sell them or not. So, holding onto vested RSUs is less of a tax move than a choice to keep owning your company’s stock (you will be taxed at either short-term or long-term capital gains rates on the growth after they vest). It’s also common practice for employers to withhold federal taxes at 22% when RSUs vest. Depending on your situation, your actual rate may differ, so it’s worth planning ahead and making sure you have the cash set aside for your tax bill if you are in a higher tax bracket. [1,2,3]

NSOs work differently, and there are two separate tax events to keep track of. The first happens when you exercise: the difference between your exercise price and the current market value of the shares gets taxed as ordinary income right then, regardless of whether you sell. The second happens when you eventually sell: any additional gain from that point forward is a capital gain. If you sell within a year of exercising, that gain is taxed as a short-term capital gain at your ordinary income rate. Hold for more than a year before selling, and it qualifies as a long-term capital gain, which may carry a lower rate than ordinary income, though that depends on your income level and overall tax situation. The key thing to understand is that these are two distinct events with two different tax treatments, and they don’t offset each other. [1]

ISOs can get you better tax treatment: if you hold the shares for at least two years from the grant date and one year from when you exercised, your gains typically get taxed at the lower capital gains rate instead of as regular income. Two things to watch out for, though. First, exercising ISOs can potentially trigger AMT, a parallel tax calculation that could create a bill even before you’ve sold anything. Second, there’s a $100,000 annual cap on ISOs, and anything above that is treated like an NSO. The tax benefit is real, but so is the risk. If the stock drops before you hit the holding period, you can lose actual money even while technically qualifying for the favorable rate. The right call depends on how much risk you’re comfortable taking with the holding period you choose. [4,5]

Why Concentration Is Riskier Than It Feels

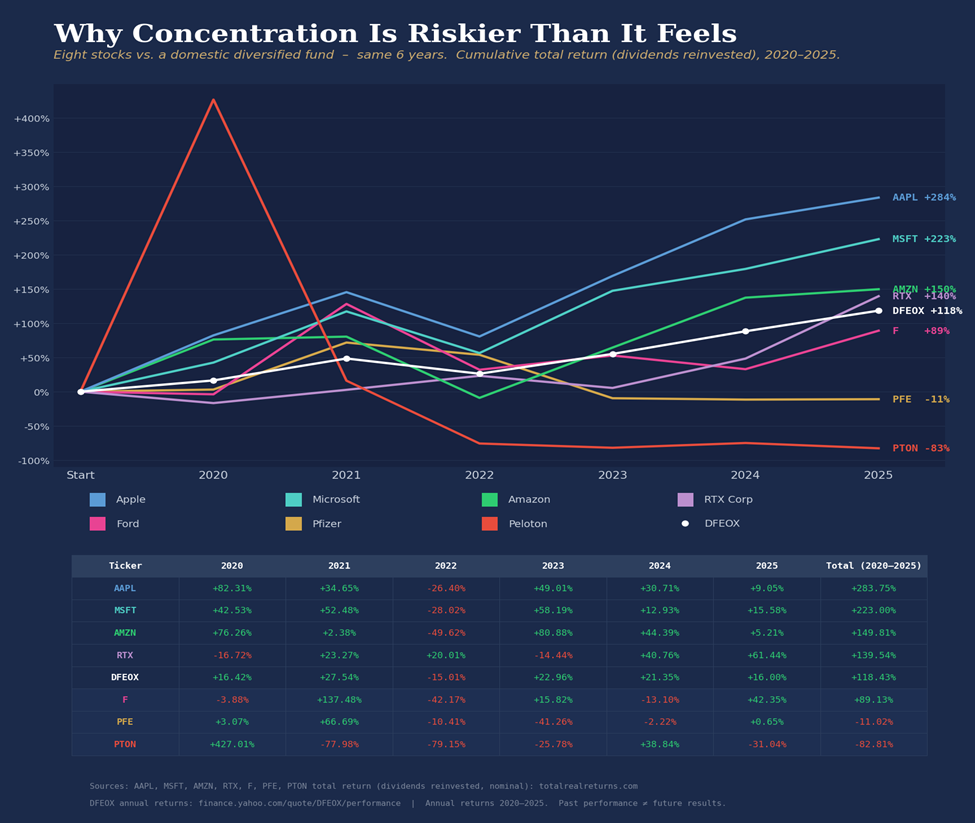

Figure 2: Eight stocks compared to DFEOX - DFA U.S. Core Equity 1 Fund (~2,700 stocks). Same six years, 2020-2025, cumulative total return with dividends reinvested. AAPL: +284%; MSFT: +223%; AMZN: +150%; RTX: +140%; DFEOX: +118%; Ford: +89%; PFE: -11%; PTON: -83%. Sources: totalrealreturns.com (AAPL, MSFT, AMZN, RTX, F, PFE, PTON); finance.yahoo.com (DFEOX)

This illustration uses a limited set of widely recognized companies for educational purposes and is not representative of all outcomes. The securities shown were selected solely as examples; this is not a recommendation. Performance shown is historical and does not indicate future results.

Harry Markowitz published his groundbreaking paper in 1952, showing that diversification can reduce risk for a given level of expected return, compared with concentrating in a single investment. (He won the Nobel Prize in Economics in 1990 for the work.) Not exactly a hot take at this point, but worth understanding why. When you own a single stock, you carry the risk that’s specific to that company: a bad earnings quarter, a leadership change, a regulatory problem, PR issues, whatever. That’s sometimes referred to as uncompensated risk, meaning you’re potentially taking on extra volatility that isn’t necessarily rewarded with higher expected returns. Spreading across many stocks reduces that layer, because when one company hits a rough patch, others don’t necessarily follow. If you’ve generated meaningful wealth from a concentrated position, it may be worth taking some risk off the table and diversifying, rather than letting it all ride. [6]

What the chart shows is that outcomes would have varied depending on which stock you happened to hold (if you held one of them). Apple and Microsoft both ended up towards the top over the full period, but each fell roughly 26-28% in 2022, which means even the highest performers in the period had rough patches. RTX also outpaced the fund (eventually). Amazon performed a little better, but with a bumpier ride. Peloton (which was up over 400% at its peak in 2020) collapsed to an 82% cumulative loss by 2025. Ford spiked +137% in 2021 on EV optimism, then gave back most of it the following year, and eventually trailed the fund over the full six years. Pfizer surged +67% in 2021 on vaccine demand, then spent the next four years in decline, ending with a negative total return including dividends. (If you want to see more cautionary tales of volatility from brands you probably recognize, just go look up AMC, Boeing, Bed Bath & Beyond, Anheiser Busch, etc….)

DFEOX (a fund with ~2,700 stocks) returned +118% over the same period. Not the best outcome on this list, but not the worst by a long shot, either, and without the same level of risk that is carried when holding a single company. That’s the core of what diversification actually does: it doesn’t guarantee the best return, but it can reduce the impact of extreme single-company outcomes.

Now, keep in mind that when you are looking at this graphic, the intent is to show you a range of outcomes from familiar companies (many of which issue equity compensation).

Research suggests over 100 distinct ways advisors add value across planning domains.¹³ Effective advisors go deep on services most relevant to their clients' needs.

The Three-Sleeve Framework

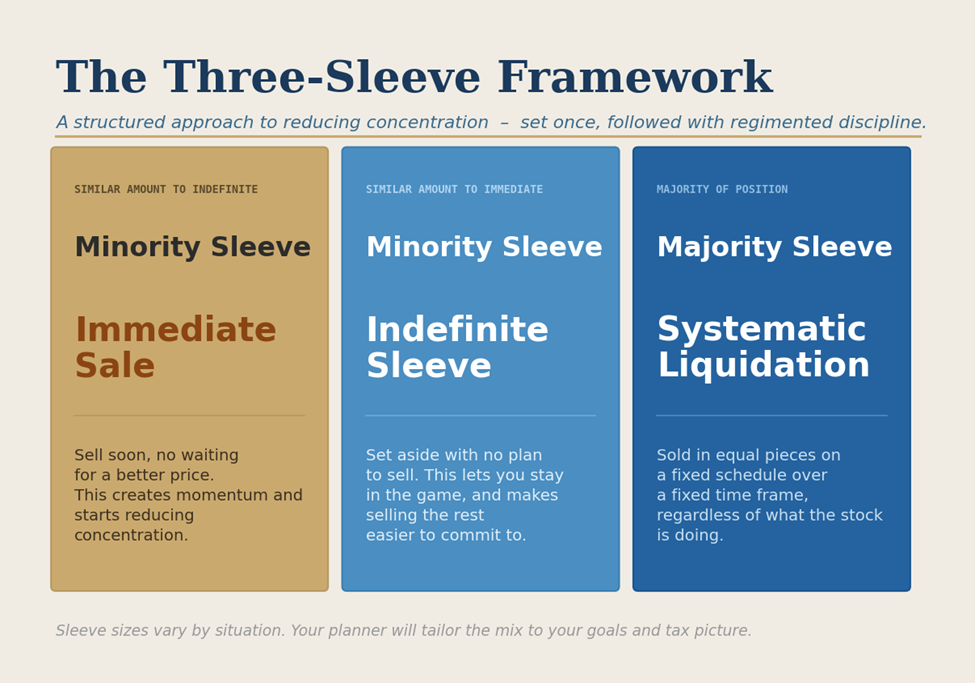

Figure 3: The Three-Sleeve Framework, a structured approach for systematically reducing a concentrated stock position. Systematic Liquidation is the largest sleeve; Immediate Sale and Indefinite Sleeve are typically similar in size. Your planner will tailor the mix to your goals and tax picture.

If you have a concentrated position, you probably already know, on some level, that you should probably take some risk off the table (probably). The issue isn’t awareness. It’s (probably) follow-through. You may fully intend to make a move, and then something stops you. Not because you’re reckless. Because the decision is genuinely hard to make in the moment. The stock may have done well recently, so maybe it keeps going up, and selling now gives you feelings of FOMO. Or it’s down, and selling now feels like locking in a loss. There’s a seemingly good reason to wait either way. So the position just keeps sitting there.

So, here’s where the Three-Sleeve Framework comes into play. Instead of telling yourself you’re going to make a well-timed decision every quarter, you set up a structure in advance and follow it (similar to dollar cost averaging, but in reverse and with shares).

You may also tie it to something real: a home purchase, a college fund, an earlier retirement. Selling with a clear purpose increases the likelihood that it actually happens. Whereas selling as a vague risk-reduction idea could get pushed to next quarter indefinitely (go look at the last graphic again if you need more convincing you’d do otherwise). A financial planner can help you connect the dots between what you’re working toward and how much stock you should sell to get there. Once you have that picture, you divide the position into three parts:

Immediate sale: Sell this piece soon, without waiting for a better price, then reinvest the proceeds. Its only job is to get the ball rolling and start bringing your concentration down.

Indefinite sleeve: Set this aside with no real plan to sell it. It’s your way of staying in the game if the stock takes off. It also makes it a lot easier to sell everything else, because you haven’t completely walked away. (You’re not giving up on the company. You’re just being sensible about the rest.)

Systematic liquidation: Sell this in equal pieces on a fixed schedule over four or five years, regardless of what the stock is doing at the time, and reinvest it accordingly. This is the hardest part to stick to, and usually the most valuable.

The Hardest Part: Actually Doing It

Most quarters, there’s going to be a good reason not to sell. When the stock is up, selling feels like leaving money on the table (look at the chart again, and ask yourself if you’d be diversifying your Microsoft or Apple stock). When it’s down, selling feels like locking in a loss (Again, now go look at Peloton or Pfizer). Both reactions are understandable. Together, they mean nothing ever happens.

The solution is a fixed schedule you set up ahead of time (when you were thinking clearly) plus someone who makes sure the trades actually go through. One of the more underrated things a financial planner brings to the table is that they can handle the implementation directly. The trades go through without having to pass through your emotional filter, avoiding a potential last-minute hesitation.

And because your equity is one piece of a larger financial picture, a planner can also make sure what you’re doing with the stock actually makes sense alongside everything else.

Option Timing: The Leverage Test and the NSO Counterintuition

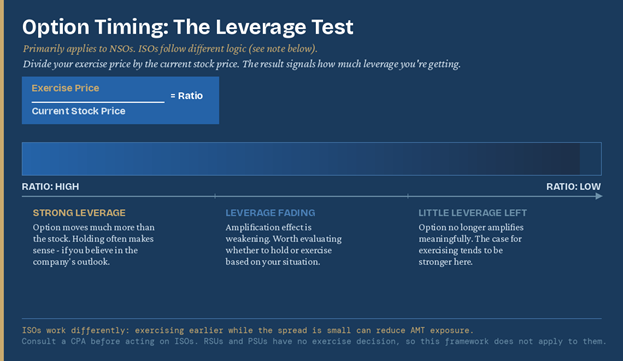

Figure 4: The Leverage Test. Divide your exercise price by the current stock price. A higher ratio means more amplification from holding; as the ratio falls, the case for exercising tends to strengthen.

An unexercised option lets you participate in the stock’s upside without putting up any money or owing any taxes yet. That’s a pretty unusual combination, and it’s worth understanding before you take action. A common practice is to exercise as soon as possible to get the capital gains clock running, but I’m going to suggest there is something else you need to consider first called The Leverage test.

The leverage test is a way to gauge how much of that amplification you’re getting on your stock option. Divide your exercise price by the current stock price. When that ratio is high, the option still moves a lot more than the stock, which means you’re getting real leverage from holding. As it falls, that amplification fades, and the case for exercising tends to get stronger. That said, the ratio is only part of the picture. The company’s health and trajectory matter too, and a high ratio may not be as meaningful if there are real questions about where the business is headed (remember the whole concentration thing we just finished talking about).

Also if you’re planning on leaving the company, your plan documents will tell you how long you have to exercise before the options expire due to leaving the company. It varies, so it’s worth looking that up before you give notice. [7]

For NSOs, exercising early to start the capital gains clock often doesn’t work out the way people expect. The moment you exercise, you pay the purchase price plus income taxes on the gain so far. That immediately shrinks the number of shares you have left working for you (assuming you sell off some shares to take care of the tax bill). If you wait, all of your options keep compounding. Yes, you’ll face a higher tax bill later, but because taxes are a percentage of whatever you gain, that larger bill reflects a larger gain, and in some scenarios, you may keep more after taxes, but outcomes depend on future stock performance, timing, and your tax situation. This logic only holds if the stock continues to grow. If the company stalls or declines, waiting can work against you.

It’s worth calling out that ISOs are a different story. For those, exercising earlier while the spread is still small probably makes more sense, since it may help reduce or avoid AMT exposure down the road. The right call depends on the type of option you have, your tax situation, and where the company is headed (again, an unknown that warrants thinking about reducing concentration). [1]

More Things Worth Thinking About

• The 22% RSU withholding. It’s common practice, but it may not cover your actual tax rate. It’s worth factoring that into your planning so a shortfall doesn’t catch you off guard. [2,3]

• RSUs piling up without a decision. Every time shares vest and you don’t sell, you’re effectively choosing to hold more concentrated stock. That might be fine, but it’s worth making that call intentionally rather than by default by inaction. [2]

• Exercising NSOs early for the capital gains clock. For NSOs, this often reduces the number of shares left compounding and can leave you with less after taxes, not more - though the right answer depends on the company’s trajectory. ISOs work differently: exercising earlier while the spread is small can sometimes reduce AMT exposure. [1]

• Skipping the AMT conversation before exercising ISOs. Exercising can potentially trigger AMT even when you haven’t sold anything yet. Worth a conversation with a CPA before you act. [4,5]

• Not tracking your cost basis. Knowing what you originally paid for your shares, and when, matters a lot when it comes to calculating gains and managing your tax bill. It’s important to not lose track of, especially across multiple grants and exercise dates (surprisingly even in this day and age, this typically isn’t automatically tracked within the account the shares are held in). [1]

• Treating your company’s stock like it can’t go wrong. Even very good companies can hit rough patches. The risk of owning a single stock is real, and it doesn’t go away just because you work there. [6]

Ready to Talk It Through?

If you’ve read this far, you’ve probably noticed how quickly the moving pieces add up. Keeping the rules straight across RSUs, NSOs, ISOs, and PSUs is one thing. Figuring out the optimal strategy for the specific type you have is another. And then there’s the question of how your equity comp fits alongside everything else in your financial life.

The complexity is especially amplified when you also have multiple, or even all of the above types of equity compensation. (I recently ran into this, and it was the catalyst for putting this article together.

If you want help sorting through your own situation, I’d enjoy the conversation.

Sources

All factual claims draw on primary sources: IRS publications, statutory tax code, peer-reviewed academic research, and one practitioner reference for the option exercise framework.

[1] Internal Revenue Service: Topic No. 427: Stock Options Authoritative IRS overview of ISO and NSO tax treatment: when income is recognized, how it is taxed, and required reporting forms.

[2] Internal Revenue Service: Publication 525: Taxable and Nontaxable Income IRS publication covering the tax treatment of various compensation types, including stock-based compensation. Confirms that RSU income is recognized at vesting as ordinary income and reported on Form W-2.

[3] Internal Revenue Service: Publication 15 (Circular E): Employer's Tax Guide Establishes the 22% flat supplemental wage withholding rate (37% on amounts above $1 million) that applies to RSU vesting income.

[4] Cornell Law LII: 26 U.S. Code § 422: Incentive Stock Options Full statutory text of IRC Section 422: qualifying disposition holding periods (2 years from grant, 1 year from exercise), the $100,000 annual ISO cap, and conditions under which favorable tax treatment is lost.

[5] Internal Revenue Service: Topic No. 556: Alternative Minimum Tax IRS overview of the Alternative Minimum Tax, including how ISO exercises can trigger AMT liability and the rules for calculating the AMT adjustment on incentive stock options.

[6] Harry Markowitz, The Journal of Finance: Portfolio Selection (1952) The foundational paper establishing Modern Portfolio Theory (JSTOR archive of the original publication). Diversification optimizes the risk-return trade-off, and a diversified portfolio dominates a concentrated single-asset position on a risk-adjusted basis. Awarded the 1990 Nobel Memorial Prize in Economic Sciences.

[7] Carta: How Stock Options Are Taxed: ISO vs. NSO Tax Treatments Practitioner reference on option leverage, ISO/NSO tax differences, and frameworks for exercise timing decisions.

This post is for educational purposes only and does not constitute tax, legal, or investment advice. Please consult a qualified financial planner, CPA, and/or attorney before making decisions about your equity compensation.

Investment advisory services are offered through Fiduciary Financial Advisors, a registered investment adviser. This material is for educational and informational purposes only and is not individualized investment, tax, or legal advice. Equity compensation rules are complex and outcomes depend on plan terms, trading windows, holding periods, and individual tax circumstances. Consult your CPA and/or attorney regarding your situation. Any performance shown is historical, for illustrative purposes, and does not indicate future results. Examples are not representative of all securities or outcomes and are not recommendations to buy or sell any security. Data may be obtained from third-party sources believed to be reliable but not independently verified.”