Savings Plus, the CalPERS 457, and Your 401(k): Making Sense of Supplemental Retirement Savings as a California State Employee

A CalPERS pension may not fully fund the lifestyle you're picturing in retirement, and closing that gap may mean saving and investing more beyond the pension itself. If you work for the state or CSU (California State University), you have access to Savings Plus, which offers not one but two options, a 401(k) and a 457(b), and it's not always clear which one should carry the bulk of that supplemental saving. If you work for a public agency or school district, it may be the CalPERS 457 Plan instead, but only if your employer has chosen to contract with CalPERS for it (SMUD employees: check with HR, since SMUD is a local agency rather than a state department, and the specific plans on offer vary by employer).

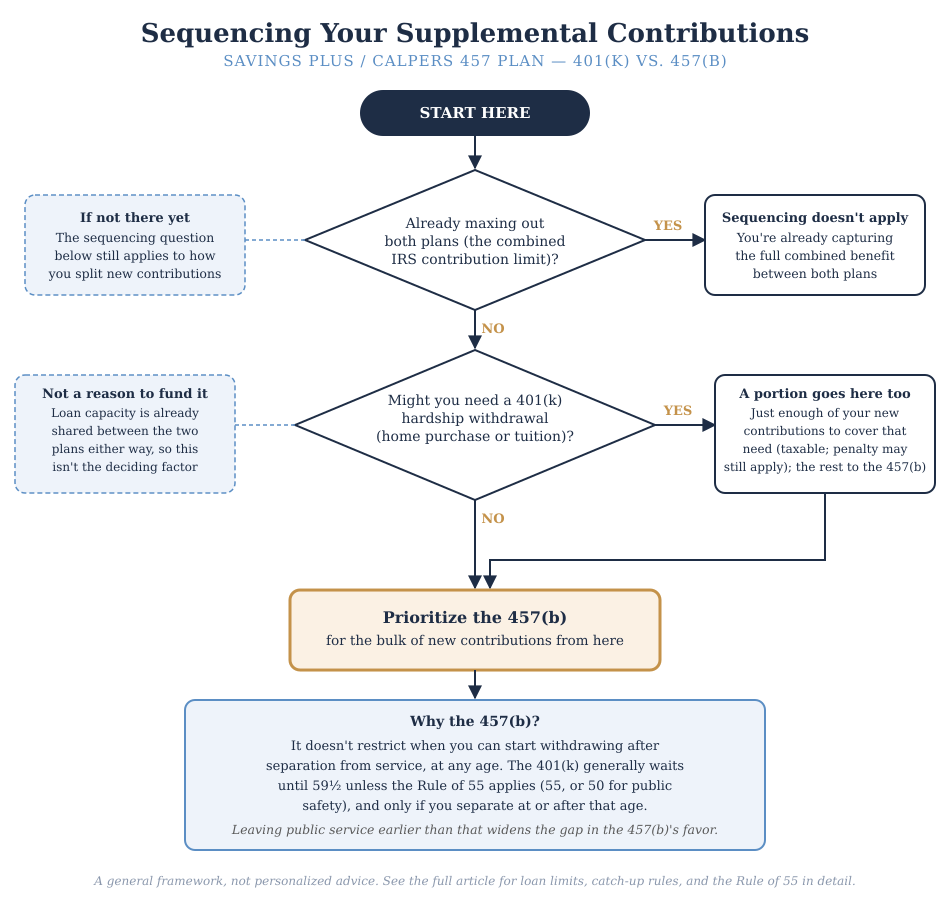

Whichever combination applies to you, the practical takeaway tends to be similar: for most participants who aren't maxing out both plans, funding the 457(b) before the 401(k) may make more sense. Though the reasoning may not be obvious, so here's what's actually driving that (in my opinion).

The Two Plans, Briefly

Savings Plus (a 401(k) and 457(b), run by the California Department of Human Resources and Nationwide, not CalPERS) is available to State of California and CSU employees. [1] The CalPERS 457 Plan is a separate 457(b) that CalPERS offers directly to public agencies and school districts that choose to contract for it. [2] Either way, using both a 401(k) and a 457(b) draws on two separate IRS limits, not one: the elective deferral cap (the amount you can contribute from your paycheck) for 2026 is $24,500 per plan (assuming no catch-up), so using both effectively doubles your contribution room to $49,000. [3]

The Loan Ceiling Doesn't Double

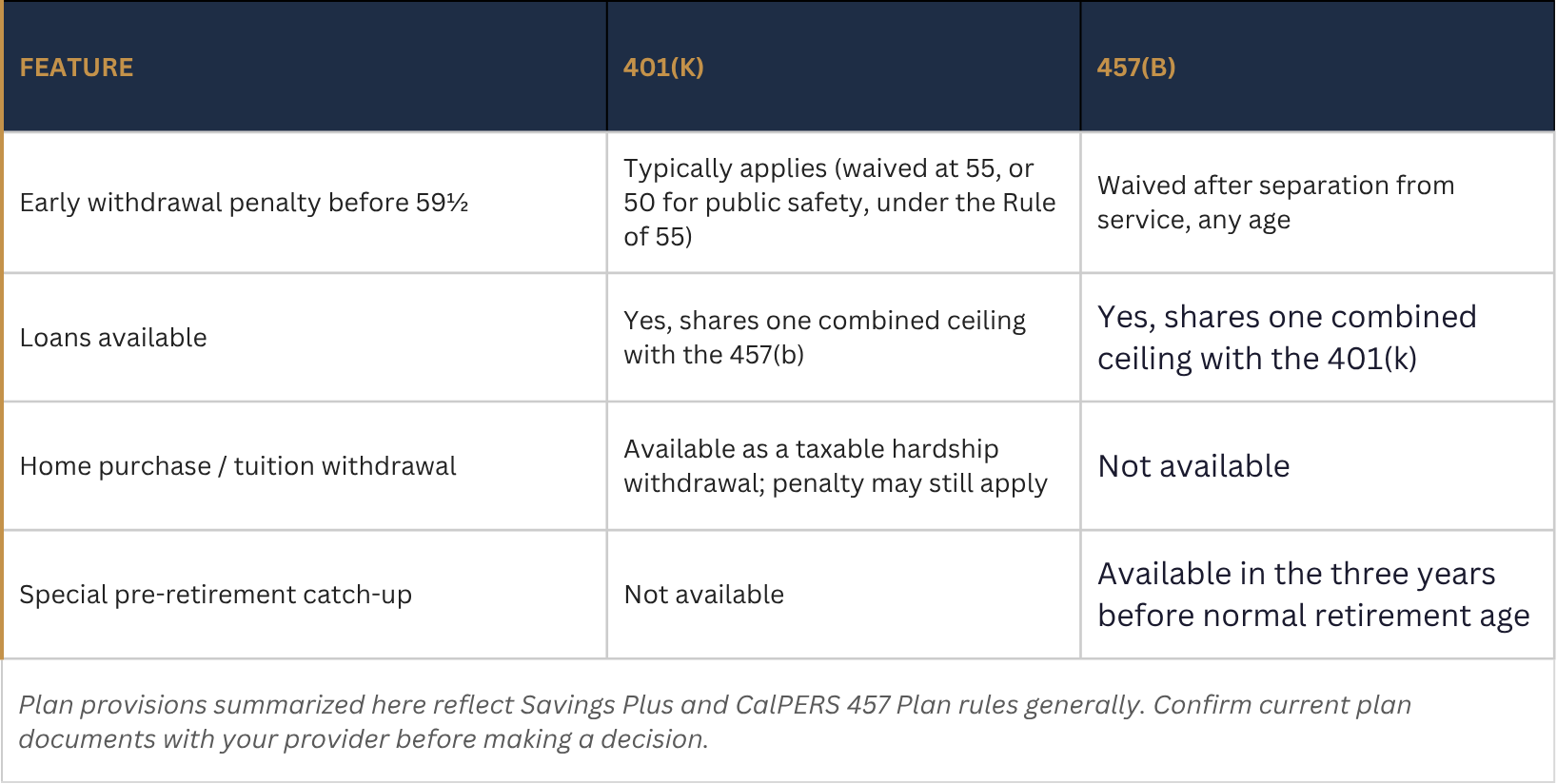

Both plans generally offer a loan, but having two accounts doesn't actually double what you can potentially borrow. Federal tax rules treat every plan the same employer maintains as a single plan for this purpose, so there's one combined ceiling, the lesser of $50,000 or 50% of your vested balance (the portion of the account that's fully yours), calculated across the 401(k) and the 457(b) together rather than separately for each. [4][5][6] Reaching the full $50,000 requires $100,000 in vested balance total, whether that's concentrated in one plan or split across both. That removes the main reason to overfund the 401(k) specifically, since the 457(b) counts toward the same shared loan ceiling.

The Hardship Withdrawal's Cost

The 401(k)'s one remaining distinguishing feature is the hardship withdrawal: an in-service withdrawal (meaning you can take the money out while still working) for a first-time home purchase or college tuition. The 457(b) doesn't offer either option. [4] But qualifying for the hardship and avoiding the 10% early withdrawal penalty are separate tests: meeting the hardship criteria doesn't by itself exempt you from the penalty if you're under 59½. [7] The withdrawal is permanent, with no repayment option. If any portion comes from a designated Roth account, the tax treatment depends on whether the distribution satisfies the applicable Roth distribution requirements under IRS rules. [8] That mix of cost, taxability, and permanence makes it a last resort, not something to plan a 401(k) balance around.

The Rule of 55: A Narrowing Nuance

The 401(k) also has a potential path to penalty-free access before age 59½, known as the Rule of 55. If you separate from service during or after the calendar year you turn 55, withdrawals from your current employer's 401(k) may be exempt from the 10% early withdrawal penalty, although pretax distributions generally remain subject to ordinary income tax. Eligibility depends on your individual circumstances and applicable IRS rules. [9] For qualified public safety employees under a governmental plan, police, firefighters, and similar roles, that age drops to 50. [9] This narrows the 457(b)'s advantage for anyone separating at or after that age; the edge is largest for someone leaving earlier, whether by choice or otherwise. The exception applies only to the plan of the employer you just left, so rolling that 401(k) into an IRA before 59½ gives it up (though there is another way to get funds out of an IRA before 59½ called the 72(t) or SEPP, but it comes with its own nuances). [9]

What's easy to miss: if you leave that job before the year you turn 55, the Rule of 55 doesn't apply at all, even if you wait until 55 or later to actually take the withdrawal. What matters is the age you were when you separated, not the age you are when you withdraw. [9][10] In that case, the 401(k) reverts to the standard 59½ threshold, the same result as if the Rule of 55 didn't exist, which strengthens the case for prioritizing the 457(b) for anyone who might leave public service earlier than that.

NOTE Confirm specifics with your plan administrator: the loan lookback calculation, whether the CalPERS 457 Plan and a local agency's 401(k) count as the “same employer” for aggregation, whether your role qualifies for the age-50 exception, and how the plan treats money rolled in from a 401(k) or IRA (which generally loses the 457(b)'s blanket penalty exemption) can all vary. [10]

Catch-Up Contributions and the 2026 Roth Rule

If you're 50 or older, both plans allow a catch-up on top of the standard limit: $8,000 for 2026 ($32,500 total per plan), or $11,250 if you'll turn 60 through 63 during the year ($35,750 total). [11] The 457(b) has one more option: a special catch-up in the three years before your plan's normal retirement age (the age your plan sets for this, not necessarily when you plan to retire) that may allow contributions up to double the standard limit, $49,000 for 2026, though it can't be combined with the age-based catch-up in the same year. [12]

NOTE One more 2026 change: if your prior-year FICA wages (wages subject to Social Security and Medicare tax) from your employer exceeded $150,000, age-based catch-up contributions must now be made as Roth rather than pretax; the 457(b)'s special three-year catch-up is currently exempt from that requirement. [13]

The Bottom Line

Put together, a workable framework looks like this: direct enough to the 401(k) to cover a plausible home purchase or tuition need, in case the hardship withdrawal option is ever necessary, and prioritize the 457(b) for the bulk of new contributions after that. The reasoning comes down to access, not capacity: the loan ceiling is shared between the two plans either way, so it doesn't favor one over the other. What favors the 457(b) is that it doesn't restrict when you can start withdrawing after separation from service, while the 401(k) generally does until 59½, unless the Rule of 55 applies (55 for most participants, 50 for qualified public safety employees). That difference matters most if you're aiming for an earlier retirement: the 457(b) removes the waiting period entirely, while the 401(k) only catches up once you reach the applicable age.

This is a framework, not a formula, and it assumes you're not already maxing out both plans. If you are, the sequencing question doesn't really apply, and deferring the full $49,000 combined, more with catch-up contributions, is a notable opportunity in its own right for higher-income households looking for more ways to defer current income. Otherwise, how this applies depends on your income, your timeline, whether the Rule of 55 or its public safety equivalent applies to you, and your plan's specific rules for catch-up contributions. This is where personalized analysis tends to matter.

Sources

[1] California Department of Human Resources, “Savings Plus Program,” calhr.ca.gov.

[2] CalPERS, “Deferred Compensation,” calpers.ca.gov/members/retirement-benefits/deferred-compensation.

[3] California State University, Fresno, Administration and Finance, “2026 Comparison Chart: 401(k) vs. 457(b).”

[4] California State University, Northridge, Human Resources, “Savings Plus Program.”

[5] Internal Revenue Service, “Issue Snapshot: Borrowing Limits for Participants with Multiple Plan Loans,” irs.gov (IRC §72(p)(2)(A)).

[6] Nationwide Retirement Solutions, “Savings Plus Loan Fact Sheet,” nrsforu.com.

[7] Internal Revenue Service, “401(k) Plan Hardship Distributions: Consider the Consequences,” irs.gov.

[8] Internal Revenue Service, “Retirement Plans FAQs on Designated Roth Accounts,” irs.gov.

[9] Internal Revenue Service, “Retirement Topics: Exceptions to Tax on Early Distributions,” irs.gov.

[10] Fidelity, “What Is the Rule of 55?” fidelity.com.

[11] Internal Revenue Service, “401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500,” irs.gov/newsroom.

[12] Nationwide Retirement Solutions, “IRS Contribution Limits,” nrsforu.com.

[13] Internal Revenue Service, “Retirement Topics: Catch-up Contributions,” irs.gov; Quarles Law Firm, “SECURE 2.0 Act Retirement Plan Update: Roth Catch-Up Contributions in 2026.”

Disclosures

Fiduciary Financial Advisors does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action. Before investing, consider investment objectives, risks, fees, and expenses. Investments in securities involve the risk of loss, including loss of principal. Past performance is no guarantee of future returns. The views and opinions reflected in the content are subject to change at any time without notice. The content speaks only as of the date indicated. Some information was obtained from external sources. The information is believed to be accurate, but there is no guarantee that it is.

This content is for educational purposes only and does not constitute personalized tax, legal, or investment advice. Consult a qualified CFP®, CPA, or attorney before taking action.

Fiduciary Financial Advisors is a registered investment adviser. Nothing here constitutes individualized investment advice. Examples are illustrative only and not recommendations. No guarantee of future results. Third-party data is not independently verified.

CFP® and CERTIFIED FINANCIAL PLANNER® are certification marks owned by the CFP Board.

You Left Your CalPERS Employer. Now What?

A plain-language guide to your options when you leave a CalPERS-covered job before you're ready to retire

Maybe you landed a role in the private sector. Maybe you relocated for family reasons. Maybe the job just wasn't the right fit anymore. Whatever happened, you've left your CalPERS-covered employer before retirement, and now you have the question: what actually happens to the benefits you've been building?

The short answer is that CalPERS doesn't disappear from your life. This article walks through those choices in plain language so you can make an informed decision rather than a default one.

What You've Built

When you work for a CalPERS-covered employer, two things are happening in your account at the same time. First, you're making employee contributions, which are a percentage of your salary set by your retirement formula and membership tier. Second, your employer is making its own contributions on your behalf into the broader fund. Only the first bucket (your own contributions plus the interest they've earned) is refundable to you. Employer contributions aren't yours to take with you; they go toward funding pension benefits for current and future retirees across the system.[1]

The pension benefit itself, that lifetime monthly payment you've heard described as "2% at 62" or "2.7% at 57" or some similar formula, isn't funded from a personal account the way a 401(k) is. It's a defined benefit: a promise from CalPERS to pay you a calculated amount for life once you reach eligibility.[2]

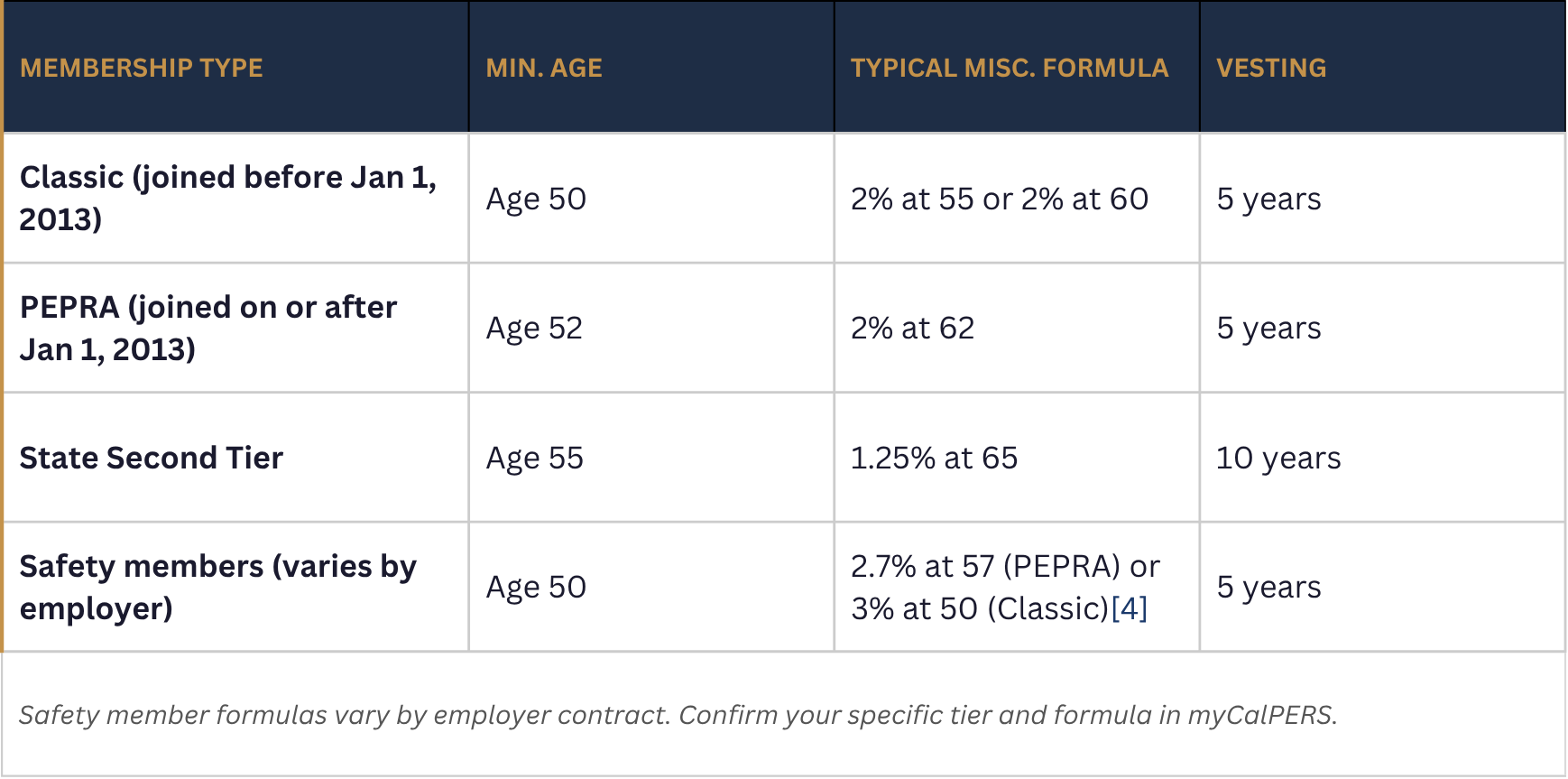

Are You Vested?

Your vesting status is the key factor in understanding your options. CalPERS uses a two-part test: you need both sufficient service credit and minimum age to collect.[3]

The Service Credit Side

For most CalPERS members, the vesting threshold is five years of CalPERS-credited service. There are some exceptions, most notably for State of California Second Tier employees, who generally need 10 years, but the five-year mark applies to the large majority of members working for state agencies, cities, counties, etc.[3]

If you've crossed that five-year threshold, you're considered vested in the pension side of things, meaning the right to a future benefit is locked in regardless of where you work next. If you haven't yet hit five years, you don't have a right to a future pension unless you return to CalPERS-covered employment, use reciprocity with another qualifying public retirement system, or had part-time status that qualifies under a specific exception.

The Age Side

Vesting in the service credit sense doesn't mean you can start collecting tomorrow. You also have to reach the minimum retirement age for your formula, which varies depending on when you became a CalPERS member:[4]

So, for example, if you're a 38-year-old Classic miscellaneous member with eight years of service credit and you leave your employer today, you're vested in the service credit sense, but you can't collect until you reach at least age 50. That gap, between your separation date and your earliest retirement eligibility date, is what makes the decisions below so consequential.

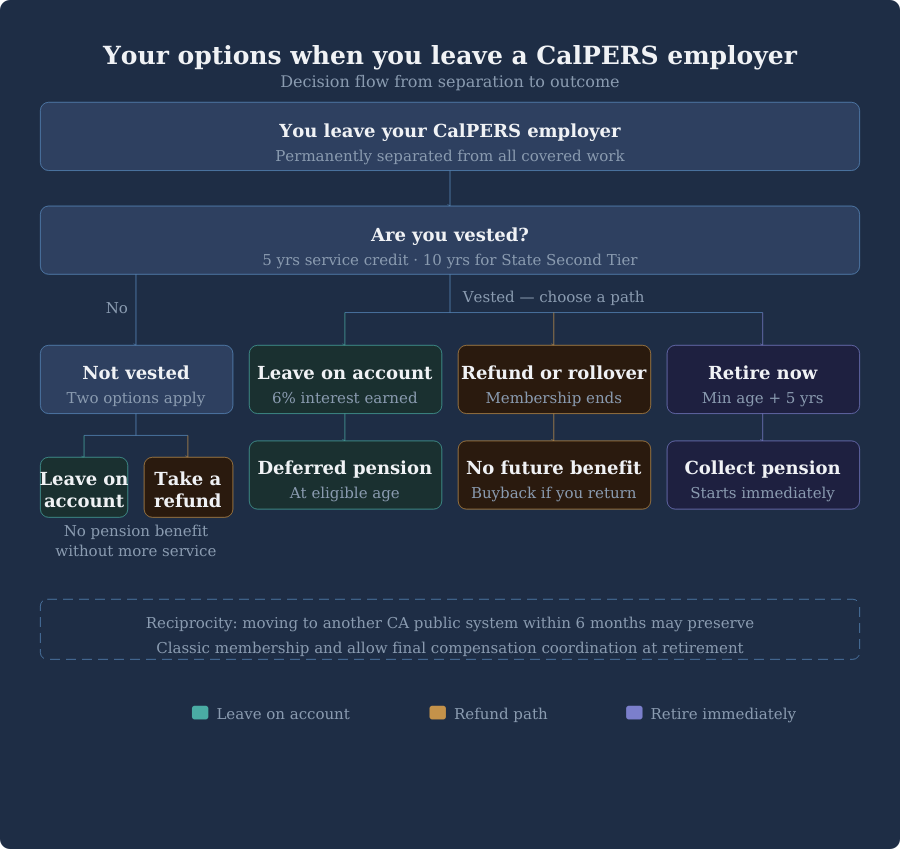

Your Three Main Options at Separation

Once you've permanently left all CalPERS-covered employment, CalPERS will mail you a document called Options at Separation. It lays out what comes next. In practice, you have three paths.[5]

Option 1: Leave Your Contributions on Account

You can leave your employee contributions exactly where they are, earning interest, until you reach minimum retirement age and choose to retire. CalPERS credits accounts left on deposit with interest at a rate of 6% per year, and your membership and service credit remain fully intact.[6]

If you're vested, this approach preserves your right to a lifetime pension payment starting at minimum retirement age. The pension amount you'd eventually receive is based on your service credit at separation, your final compensation, and your age when you actually retire. You won't earn additional CalPERS service credit during the years you're working elsewhere, but the credit you built doesn't evaporate.

One thing to know about this option: under federal Required Minimum Distribution rules, if you haven't retired or refunded your account, CalPERS will eventually require a distribution. The age threshold depends on your birth year: age 73 for those born between 1951 and 1959, and age 75 for those born in 1960 or later.[7] If you're leaving public employment mid-career, that deadline is likely far enough away to not be a factor in the initial decision.

Option 2: Take a Refund or Roll Over Your Contributions

You can request a refund of your employee contributions and the interest they've earned. This terminates your CalPERS membership. Once you choose this path, you forfeit your right to any future pension benefit, disability retirement, or survivor benefits under CalPERS.[8]

The refund is taxable as ordinary income unless you roll it over into a qualified retirement account (an IRA or an eligible employer plan that accepts rollovers). If you receive the money directly, CalPERS is required to withhold 20% for federal income tax, and you may face an additional 10% early withdrawal penalty if you're under 59½ and don't roll the funds over.[9]

If you later return to CalPERS-covered employment and want to buy back your prior service credit, you can do so, but the cost is typically higher than what you were originally refunded, and it increases over time as interest accrues.[8]

Option 3: Retire Immediately (If You're Eligible)

If you've reached minimum retirement age and have at least five years of service credit, you may be eligible to apply for retirement now rather than deferring it.[4] This tends to come up most often for members who've spent a longer career in public service, or who are separating later in their working years.

Retiring at the minimum age typically means accepting a lower benefit factor than if you waited, since most CalPERS formulas are structured to reward retiring later. It also means your CalPERS health benefits question comes into focus immediately (more on that below). For many people, the timing question of when to start CalPERS benefits involves a breakeven analysis that intersects with Social Security timing, other savings, and healthcare coverage, so it pays to run those numbers before making the call.

Reciprocity With Another Public Retirement System

If you're leaving one public employer and heading to another, or you're considering it, CalPERS has reciprocal agreements with most other California public retirement systems. Reciprocity allows you to coordinate benefits between systems in a way that tends to be more favorable than treating them as entirely separate.[14]

The mechanics work like this: there's no transfer of funds or service credit between systems. Instead, when you retire from both systems simultaneously (using the same retirement date), your highest final compensation from either system can be used to calculate the pension from each. You draw separate retirement payments from each system.[14]

To establish reciprocity, the main rule to know is the six-month window: you need to move from one reciprocal system to the next within six months, without a gap in active membership.[15] If you take more than six months off before joining a new public employer, reciprocity likely won't apply.

Reciprocity also affects your CalPERS membership tier. Classic members who move to another CalPERS-covered employer within six months typically retain their Classic membership status, which matters quite a bit given the more generous formulas Classic tiers carry relative to PEPRA.[16]

Reciprocal systems include, but are not limited to Other CalPERS-covered employers (which automatically share membership); CalSTRS (California State Teachers’ Retirement System); County “1937 Act” systems such as LACERA, SCERS, and others; San Francisco Employees’ Retirement System (SFERS); and various other qualifying California public retirement systems. If you’re moving to a position under one of these systems, ask both systems about reciprocity before your start date.

What to Think Through Before You Decide

The options at separation aren't equally consequential for everyone. Here is what you should think through:

• Are you vested? If you haven't hit five years of service credit, your options look different than if you have. A non-vested member taking a refund isn't forfeiting a pension they'd otherwise have. A vested member doing the same often is.[3]

• How long until minimum retirement age? The longer the runway, the more you want to think carefully about whether leaving contributions on account makes sense.[4]

• Will you return to public sector work? If there's any realistic chance you'll come back to a CalPERS employer, keeping your membership intact is probably the better decision. Service credit is additive, and buying it back later is expensive.[8]

• What's the reciprocity picture? If you're heading to another California public employer, verify the six-month window and establish reciprocity before your start date. This is one of the decisions that's easy to get right.[15]

• What does your retirement income picture look like overall? CalPERS pension income, if it's eventually payable, is one piece of a broader picture that often includes Social Security, your Savings Plus Program (which is comprised of a 457(b) and 401(k) plan), or other deferred compensation balance, and non-retirement savings. The refund decision looks different depending on what else is in that picture.

• What's the tax impact of a refund? If you're taking a refund in a year with high other income, the tax drag can add up. If you're in a lower-income year, the impact is more manageable. Rolling into an IRA avoids current taxation but still closes the CalPERS door.[9]

Don't Lose Track of Your Account

CalPERS will send you an Annual Member Statement every fall, but those go to the address on file. Keep your contact information current in myCalPERS, and check your account periodically, especially as you approach your eligible retirement window.[17]

This is where it gets personal.

The choice between leaving contributions on account, taking a refund, and establishing reciprocity intersects with your tax situation, your other retirement savings, your career plans, and how you model lifetime income. The right answer depends on the details of your situation. If you've recently left a CalPERS-covered employer and want to think through your specific numbers, I'm happy to help you work through it.

Sources

1. CalPERS. "Refund Member Contributions." calpers.ca.gov/page/active-members/retirement-benefits/refund-member-contributions

2. CalPERS. "Service & Disability Retirement." calpers.ca.gov/members/retirement-benefits/service-disability-retirement

3. CalPERS PERSpective. "CalPERS 101: Your Pension and the Vesting System." news.calpers.ca.gov/your-calpers-pension-is-on-a-vesting-system-heres-what-that-means

4. CalPERS. "Options at Separation" (PDF). calpers.ca.gov/documents/options-at-separation/download

5. CalPERS. "Options at Separation" letter (PDF). calpers.ca.gov/documents/options-at-separation/download

6. CalPERS. "A Benefits Guide for Public Agency Members" (PDF). calpers.ca.gov/documents/new-member-public-agency-guide/download

7. SECURE 2.0 Act of 2022; IRS Final Regulations on Required Minimum Distributions (89 Federal Register 58886, eff. Jan. 1, 2025). federalregister.gov/documents/2024/07/19/2024-14542/required-minimum-distributions

8. CalPERS. "Refund Member Contributions." calpers.ca.gov/page/active-members/retirement-benefits/refund-member-contributions

9. CalPERS. "Refund Election Form Packet — Special Tax Notice: Your Rollover Options" (PDF). calpers.ca.gov/documents/refund-election-form-packet/download

10. CalPERS. "Eligibility & Enrollment (Active Members)." calpers.ca.gov/members/health-benefits/eligibility-and-enrollment

11. CalPERS. "COBRA Coverage." calpers.ca.gov/members/health-benefits/eligibility-and-enrollment/cobra

12. CalPERS. "Eligibility & Enrollment (Retirees)." calpers.ca.gov/retirees/health-and-medicare/eligibility-and-enrollment

13. CalPERS PERSpective. "Health Vesting 101." news.calpers.ca.gov/health-vesting-101/

14. CalPERS. "Reciprocity (Linking Retirement Systems)." calpers.ca.gov/members/retirement-benefits/reciprocity

15. CalPERS PERSpective. "What You Need to Know About Reciprocity." news.calpers.ca.gov/what-you-need-to-know-about-reciprocity-2/

16. CalPERS. "Public Employees' Pension Reform Act (PEPRA)." calpers.ca.gov/page/about/laws-legislation-regulations/public-employees-pension-reform-act

17. CalPERS. "A Benefits Guide for Public Agency Members" (PDF). calpers.ca.gov/documents/new-member-public-agency-guide/download

Disclosures

Fiduciary Financial Advisors does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action. Before investing, consider investment objectives, risks, fees, and expenses. Investments in securities involve the risk of loss, including loss of principal. Past performance is no guarantee of future returns. The views and opinions reflected in the content are subject to change at any time without notice. The content speaks only as of the date indicated. Some information was obtained from external sources. The information is believed to be accurate, but there is no guarantee that it is.

This content is for educational purposes only and does not constitute personalized tax, legal, or investment advice. Consult a qualified CFP®, CPA, or attorney before taking action.

Fiduciary Financial Advisors is a registered investment adviser. Nothing here constitutes individualized investment advice. Examples are illustrative only and not recommendations. No guarantee of future results. Third-party data is not independently verified.

CFP® and CERTIFIED FINANCIAL PLANNER® are certification marks owned by the CFP Board.

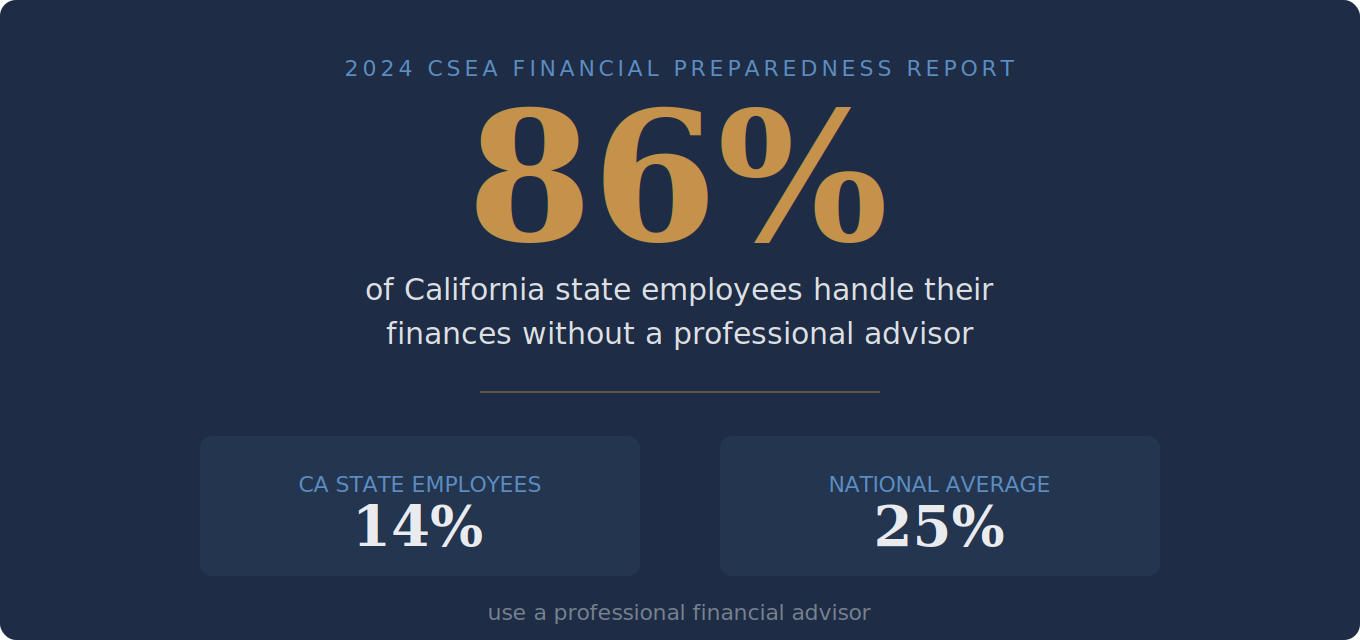

86% of California State Employees Are Handling Their Finances Alone.

Here’s What They May Be Missing.

If you work for the State of California, SMUD, Caltrans, CDCR, or any other CalPERS-covered employer, you have access to a strong retirement benefit package. A defined benefit pension, Savings Plus 401(k) and 457(b) options, and (depending on your role) Social Security coordination that often requires careful planning.

And yet, according to a recent financial preparedness survey of nearly 5,000 California state employees, the overwhelming majority of you are navigating all of that on your own.[1]

That’s not a judgment. It’s a data point. And it’s worth understanding why it matters.

What the Research Actually Says

The 2024 California State Employees Financial Preparedness Report, published by the California State Employees Association (CSEA) and based on a survey of active and retired state workers, found some numbers that are hard to ignore:[1]

86% of California state employees handle their own financial and retirement planning, relying on friends, family, and online resources rather than a professional advisor.

Only 14% use a professional financial advisor, compared to roughly 25% of Americans nationally.

When researchers asked why, the answers were familiar: it costs too much, I don’t have enough saved, I haven’t found someone I trust, or I just don’t think I need one.[1]

Those are all reasonable-sounding explanations. But here’s where the data gets interesting, because the same survey measured how those two groups actually feel about their financial lives.

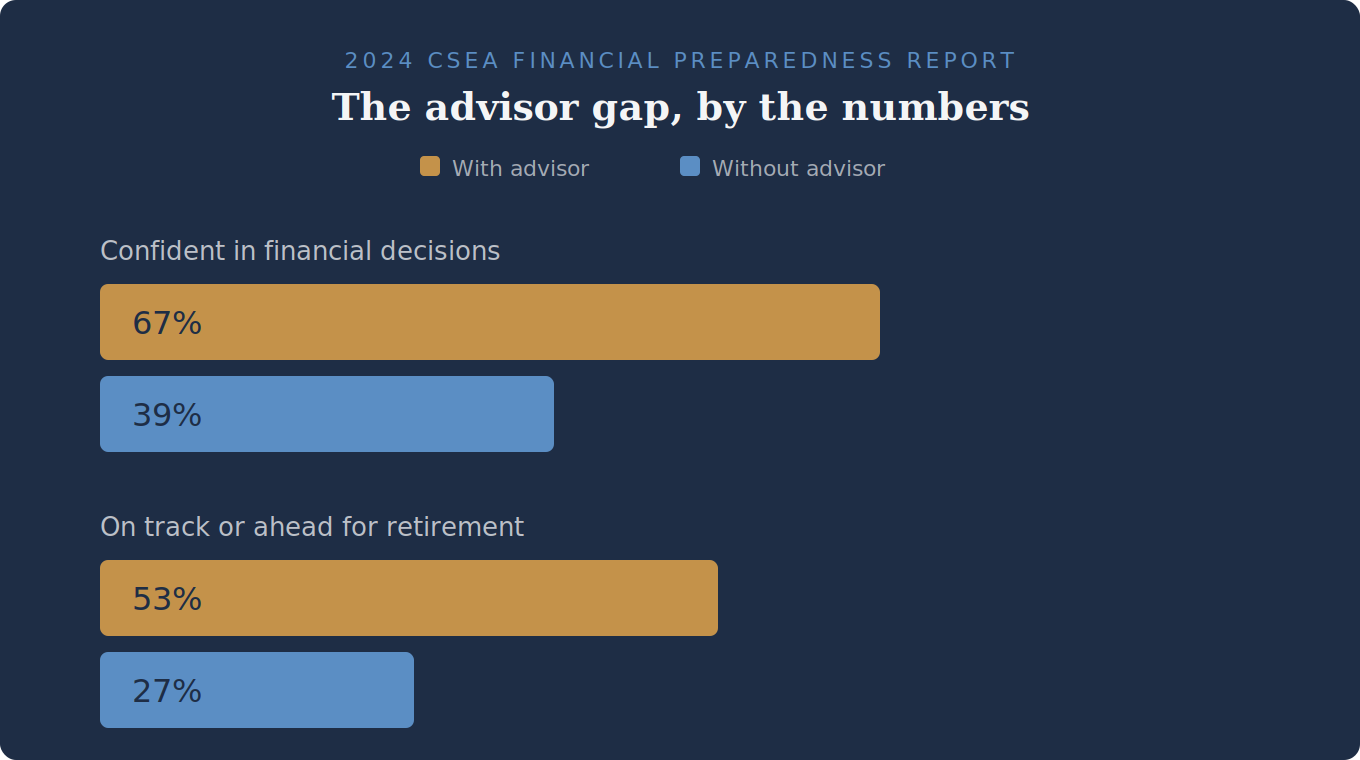

The Confidence Gap You Can Measure

State employees with an advisor: 67% felt confident in their financial decision-making. State employees without an advisor: 39%.

State employees with an advisor: 53% said they were on track or ahead of schedule for retirement. State employees without an advisor: 27%.

That’s not a marginal difference. That’s roughly double the confidence and nearly double the retirement readiness, at least as self-reported.[2]

Now, correlation is not causation (people who seek out advisors may already be more financially engaged). But the gap is wide enough to raise a question worth sitting with: if you’re in the 86% handling your finances without professional guidance, what are the odds there are opportunities you haven’t fully considered?

What DIY Planning May Miss for CalPERS Employees

The reason this matters more for public employees than, say, someone with a basic 401(k) and no pension is that your benefits stack is notably complex. There are moving parts that interact with each other, and because some of those decisions (like your pension option election or retirement date) are difficult or impossible to undo, the cost of a misstep may compound over time.

Here are some of the areas where a qualified advisor tends to help clarify the picture for CalPERS members:

Pension Timing and Retirement Date Optimization

Your CalPERS benefit is calculated using a formula, and the timing of when you retire may significantly affect your monthly benefit for life. Retiring right before versus right after a birthday quarter, for example, may change your benefit factor. Many employees look at their pension estimate and assume that’s the number, without realizing that a few strategic adjustments to timing could increase their monthly income (or overlook the impact that a prior divorce may have if the pension benefit was part of the settlement).

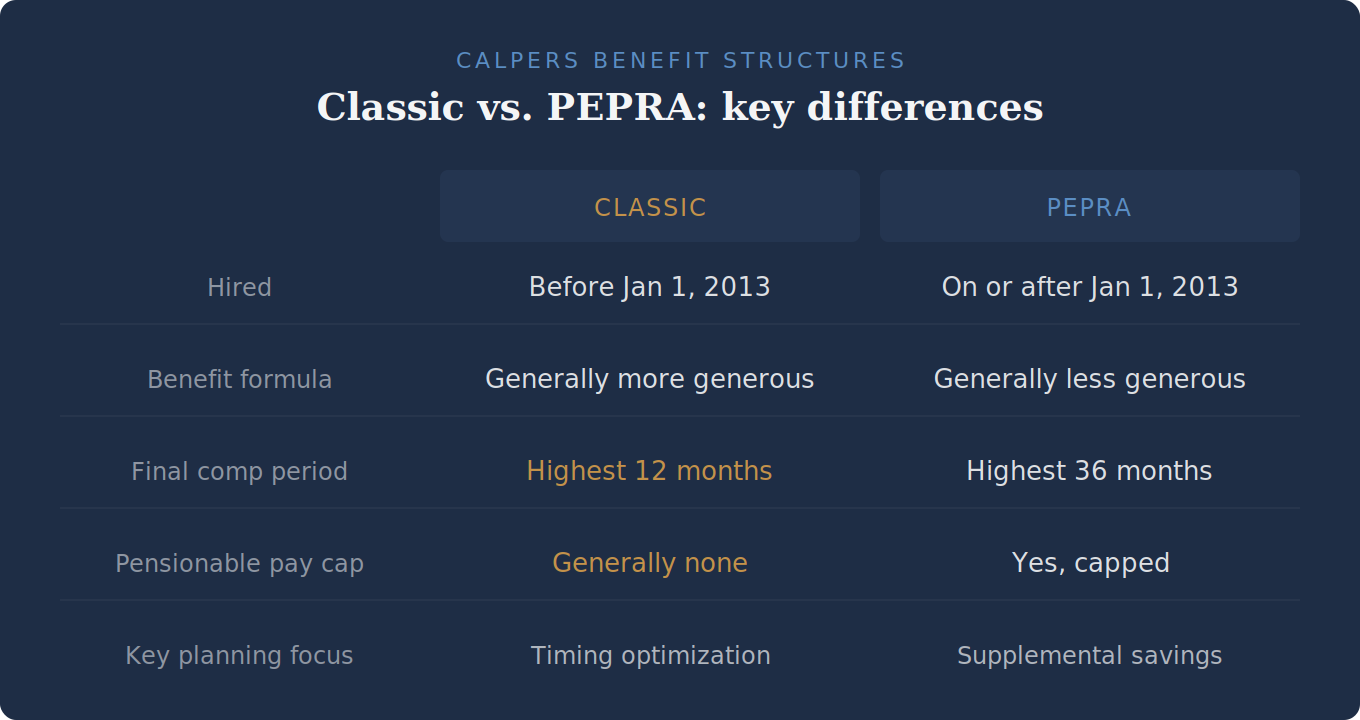

And the stakes here differ depending on when you were hired. If you started with a CalPERS-covered employer before January 1, 2013, you’re a “Classic” member with a generally more generous benefit formula, and your final compensation is based on your highest 12 consecutive months of pay. If you were hired on or after that date, you fall under PEPRA (the Public Employees’ Pension Reform Act), which uses a generally less generous formula, a 36-month final compensation period, and a cap on the salary that counts toward your pension. (For simplicity, this overview focuses on miscellaneous members. Safety members and State Second Tier members have different formulas and benefit structures.)[3]

That’s a significant difference. A Classic member nearing retirement may have a richer benefit, but that also means more complex optimization decisions around timing, final comp windows, and retirement option elections. A PEPRA member, on the other hand, is generally working with a less generous formula, which may make supplemental savings strategy and tax planning that much more important for closing the gap between their pension income and the retirement lifestyle they want. Either way, understanding which set of rules applies to you (and how to work within them) is one of the areas where professional guidance may be worth exploring.

Savings Plus Strategy (the 401(k)/457(b) Decision)

If you’re a state employee, you have access to both a 401(k) and a 457(b) through Savings Plus, which means you may be able to contribute up to $49,000 per year in 2026 (or more if you’re over 50 or nearing retirement and eligible for catch-up provisions).[4] But many employees may not be maximizing both plans, and may not be thinking strategically about whether to use pre-tax, Roth, or a combination. The right answer depends on your current tax bracket, your expected pension income, your other sources of retirement income, and your timeline. This is especially true for PEPRA members, whose pension formula and pensionable pay cap may make supplemental savings through Savings Plus an important lever for building retirement security.

And if you work for an employer like SMUD that offers its deferred compensation through Fidelity rather than the Savings Plus/Nationwide platform, the investment options and fee structures are different, which may matter for how you allocate.

Social Security Coordination

Not every CalPERS member pays into Social Security (it depends on your employer’s specific arrangement).[5] For those who do, coordinating your pension income, Savings Plus distributions, and Social Security claiming strategy may noticeably affect your total after-tax retirement income. For those who don’t, understanding how that gap affects your overall plan may be just as important.

Tax Planning Around Retirement

Your CalPERS pension is fully taxable as ordinary income. So are distributions from your Savings Plus accounts (unless they’re Roth). If you’re retiring in California, where state income tax rates may run above 9% for many retirees, the difference between a tax-aware withdrawal strategy and just taking money as you need it may be larger than you’d think.

This is where Roth conversion planning in the years leading up to retirement tends to be especially valuable, and where DIY planners may not realize what options are available to them.

Why Most People Put This Off

(Even When They Know Better)

If you’ve been meaning to get your financial plan together "someday," you’re in very large company. Financial procrastination isn’t laziness. It’s usually one of a few predictable things:

The complexity feels overwhelming. CalPERS alone has multiple benefit formulas, PEPRA vs. Classic distinctions, reciprocity rules, and different employer contracts. Add in Savings Plus, Social Security, tax planning, and retirement timing decisions, and it’s understandable that many people just default to "I’ll figure it out later."

There’s no forcing function until retirement is close. Unlike a leaky roof or a check engine light, the consequences of not having a plan often don’t show up right away. But by the time they do (often in the form of a tax surprise, a suboptimal pension election, or a realization that you can’t retire when you planned), the window to fix things has narrowed.

Trust is a real barrier. The CSEA survey confirmed this.[1] Many state employees haven’t found an advisor they trust, and that’s an understandable concern. Not every advisor understands CalPERS benefits, Savings Plus options, or the specific planning challenges that come with public sector employment. Working with someone who doesn’t know your benefits package well can sometimes feel worse than doing it yourself.

What to Look for If You’re Considering Working with Someone

If you’re a CalPERS member who’s been thinking about getting professional guidance (even if you’ve been thinking about it for a while), here are a few things that tend to matter most:

Fiduciary standard. Look for an advisor who is legally required to act in your best interest, sometimes referred to as a fiduciary. That’s an important distinction worth understanding when evaluating any advisor relationship.

Familiarity with public sector employees and pension benefits. There’s a difference between a generalist financial planner and one who has experience working with pension benefits and public sector employees. Ask whether they’ve worked through pension optimization, deferred compensation strategy, and retirement tax planning with people whose benefits look like yours. Ask how many clients they serve in similar situations.

A comprehensive approach, not just one piece of the puzzle. A good financial plan for a CalPERS member doesn’t stop at a retirement projection. It connects your pension, your supplemental savings, your tax situation, and your investment strategy into a coordinated approach. Look for someone who ties these pieces together rather than addressing them in isolation.

The Bottom Line

You’ve built a career in public service, and the benefits you’ve earned along the way are valuable. But they’re also complex, and the gap between a good plan and no plan may be wider than you’d expect over the course of a retirement.

If you’re one of the 86% who’s been going it alone, that doesn’t mean you’ve been doing it wrong. It might just mean you haven’t found the right fit yet.

Interested in talking through your CalPERS benefits and how they fit into your bigger financial picture? You can schedule a no-obligation introductory conversation below.

Sources

California State Employees Association (CSEA). “2024 California State Employees Financial Preparedness Report.” Published 2024. Survey of nearly 5,000 active and retired California state employees conducted November 2023. N=3,817 active employees (95% confidence, ±2%), N=1,172 retirees (95% confidence, ±2%). Available at cseabenefitsprogram.com.

CSEA. “DIYing Your Own Retirement Savings Plan? Here’s What You Need to Know.” cseabenefitsprogram.com, 2024. National advisor usage estimate (25%) cited from 2022 Harris Poll. Confidence and retirement readiness comparisons derived from the 2024 Financial Preparedness Report.

CalPERS. “Public Employees’ Pension Reform Act (PEPRA).” calpers.ca.gov. PEPRA took effect January 1, 2013, establishing new benefit formulas, final compensation periods, and pensionable compensation caps for members hired on or after that date.

Internal Revenue Service. “401(k) limit increases to $24,500 for 2026; IRA limit increases to $7,500.” irs.gov, November 2025. The 401(k) and governmental 457(b) elective deferral limits are separate, allowing combined contributions of up to $49,000 ($24,500 each) before catch-up provisions.

CalPERS. “Social Security & Your CalPERS Pension.” calpers.ca.gov. Social Security coverage varies by employer arrangement. Non-covered positions (often safety classifications and certain State of California roles) do not withhold Social Security taxes. The Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) were repealed by the Social Security Fairness Act, signed into law January 5, 2025.

Disclosures

This post is for educational purposes only and does not constitute tax, legal, or investment advice. Please consult a qualified financial planner, CPA, and/or attorney before making decisions about your investments.

Investment advisory services are offered through Fiduciary Financial Advisors, a registered investment adviser. This material is for educational and informational purposes only and is not individualized investment, tax, or legal advice. Equity compensation rules are complex and outcomes depend on plan terms, trading windows, holding periods, and individual tax circumstances. Consult your CPA and/or attorney regarding your situation. Any performance shown is historical, for illustrative purposes, and does not indicate future results. Examples are not representative of all securities or outcomes and are not recommendations to buy or sell any security. Data may be obtained from third-party sources believed to be reliable but not independently verified.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.