Savings Plus, the CalPERS 457, and Your 401(k): Making Sense of Supplemental Retirement Savings as a California State Employee

A CalPERS pension may not fully fund the lifestyle you're picturing in retirement, and closing that gap may mean saving and investing more beyond the pension itself. If you work for the state or CSU (California State University), you have access to Savings Plus, which offers not one but two options, a 401(k) and a 457(b), and it's not always clear which one should carry the bulk of that supplemental saving. If you work for a public agency or school district, it may be the CalPERS 457 Plan instead, but only if your employer has chosen to contract with CalPERS for it (SMUD employees: check with HR, since SMUD is a local agency rather than a state department, and the specific plans on offer vary by employer).

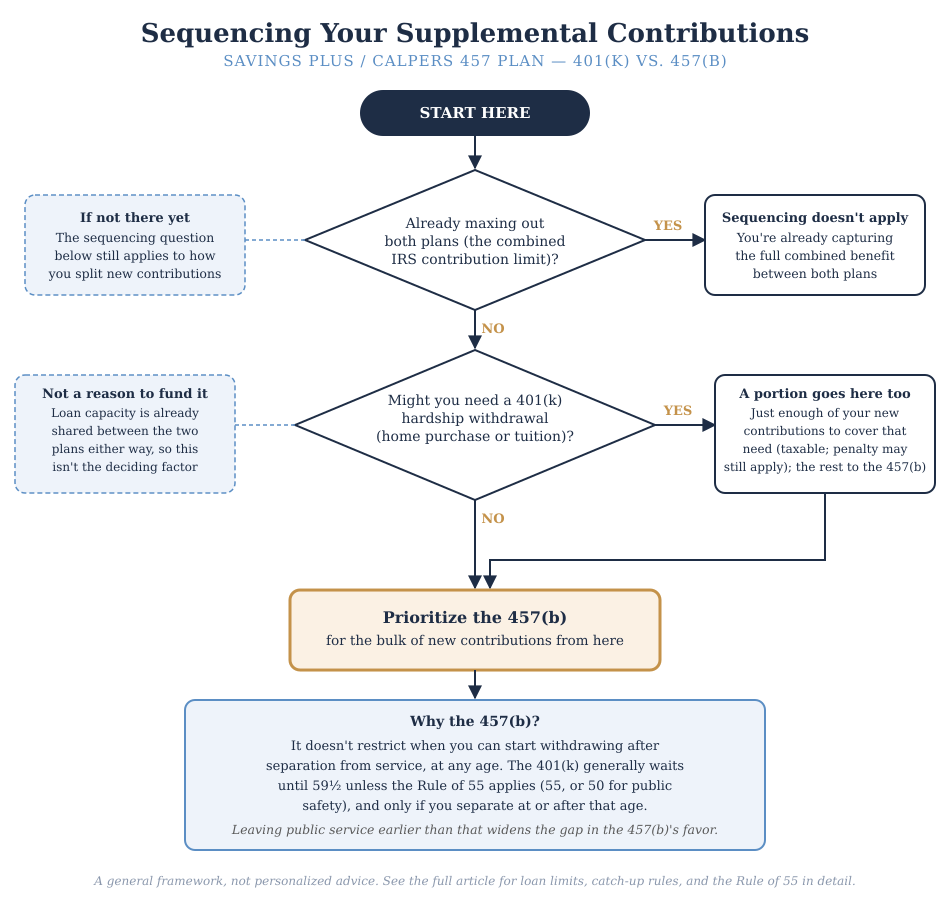

Whichever combination applies to you, the practical takeaway tends to be similar: for most participants who aren't maxing out both plans, funding the 457(b) before the 401(k) may make more sense. Though the reasoning may not be obvious, so here's what's actually driving that (in my opinion).

The Two Plans, Briefly

Savings Plus (a 401(k) and 457(b), run by the California Department of Human Resources and Nationwide, not CalPERS) is available to State of California and CSU employees. [1] The CalPERS 457 Plan is a separate 457(b) that CalPERS offers directly to public agencies and school districts that choose to contract for it. [2] Either way, using both a 401(k) and a 457(b) draws on two separate IRS limits, not one: the elective deferral cap (the amount you can contribute from your paycheck) for 2026 is $24,500 per plan (assuming no catch-up), so using both effectively doubles your contribution room to $49,000. [3]

The Loan Ceiling Doesn't Double

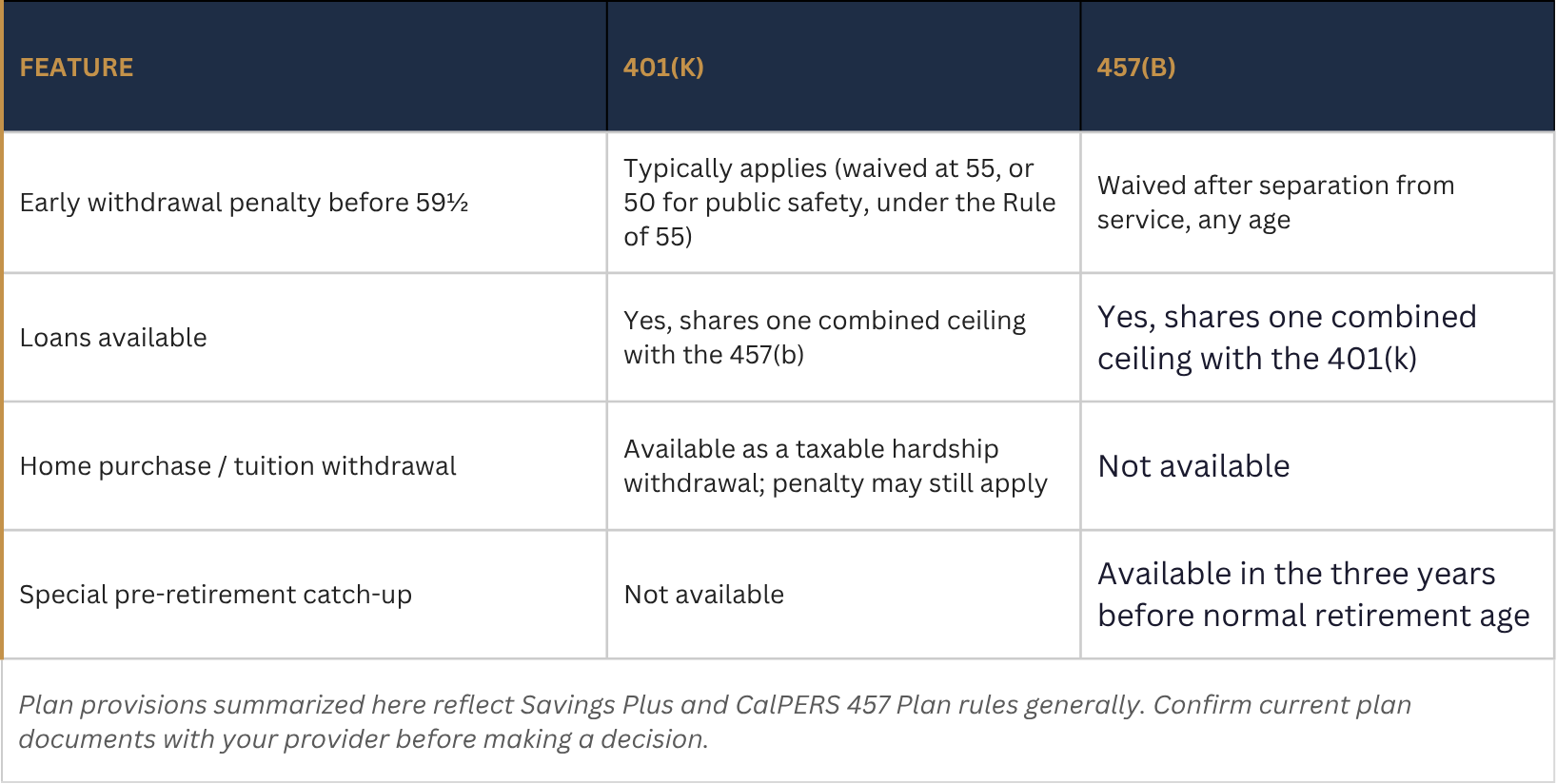

Both plans generally offer a loan, but having two accounts doesn't actually double what you can potentially borrow. Federal tax rules treat every plan the same employer maintains as a single plan for this purpose, so there's one combined ceiling, the lesser of $50,000 or 50% of your vested balance (the portion of the account that's fully yours), calculated across the 401(k) and the 457(b) together rather than separately for each. [4][5][6] Reaching the full $50,000 requires $100,000 in vested balance total, whether that's concentrated in one plan or split across both. That removes the main reason to overfund the 401(k) specifically, since the 457(b) counts toward the same shared loan ceiling.

The Hardship Withdrawal's Cost

The 401(k)'s one remaining distinguishing feature is the hardship withdrawal: an in-service withdrawal (meaning you can take the money out while still working) for a first-time home purchase or college tuition. The 457(b) doesn't offer either option. [4] But qualifying for the hardship and avoiding the 10% early withdrawal penalty are separate tests: meeting the hardship criteria doesn't by itself exempt you from the penalty if you're under 59½. [7] The withdrawal is permanent, with no repayment option. If any portion comes from a designated Roth account, the tax treatment depends on whether the distribution satisfies the applicable Roth distribution requirements under IRS rules. [8] That mix of cost, taxability, and permanence makes it a last resort, not something to plan a 401(k) balance around.

The Rule of 55: A Narrowing Nuance

The 401(k) also has a potential path to penalty-free access before age 59½, known as the Rule of 55. If you separate from service during or after the calendar year you turn 55, withdrawals from your current employer's 401(k) may be exempt from the 10% early withdrawal penalty, although pretax distributions generally remain subject to ordinary income tax. Eligibility depends on your individual circumstances and applicable IRS rules. [9] For qualified public safety employees under a governmental plan, police, firefighters, and similar roles, that age drops to 50. [9] This narrows the 457(b)'s advantage for anyone separating at or after that age; the edge is largest for someone leaving earlier, whether by choice or otherwise. The exception applies only to the plan of the employer you just left, so rolling that 401(k) into an IRA before 59½ gives it up (though there is another way to get funds out of an IRA before 59½ called the 72(t) or SEPP, but it comes with its own nuances). [9]

What's easy to miss: if you leave that job before the year you turn 55, the Rule of 55 doesn't apply at all, even if you wait until 55 or later to actually take the withdrawal. What matters is the age you were when you separated, not the age you are when you withdraw. [9][10] In that case, the 401(k) reverts to the standard 59½ threshold, the same result as if the Rule of 55 didn't exist, which strengthens the case for prioritizing the 457(b) for anyone who might leave public service earlier than that.

NOTE Confirm specifics with your plan administrator: the loan lookback calculation, whether the CalPERS 457 Plan and a local agency's 401(k) count as the “same employer” for aggregation, whether your role qualifies for the age-50 exception, and how the plan treats money rolled in from a 401(k) or IRA (which generally loses the 457(b)'s blanket penalty exemption) can all vary. [10]

Catch-Up Contributions and the 2026 Roth Rule

If you're 50 or older, both plans allow a catch-up on top of the standard limit: $8,000 for 2026 ($32,500 total per plan), or $11,250 if you'll turn 60 through 63 during the year ($35,750 total). [11] The 457(b) has one more option: a special catch-up in the three years before your plan's normal retirement age (the age your plan sets for this, not necessarily when you plan to retire) that may allow contributions up to double the standard limit, $49,000 for 2026, though it can't be combined with the age-based catch-up in the same year. [12]

NOTE One more 2026 change: if your prior-year FICA wages (wages subject to Social Security and Medicare tax) from your employer exceeded $150,000, age-based catch-up contributions must now be made as Roth rather than pretax; the 457(b)'s special three-year catch-up is currently exempt from that requirement. [13]

The Bottom Line

Put together, a workable framework looks like this: direct enough to the 401(k) to cover a plausible home purchase or tuition need, in case the hardship withdrawal option is ever necessary, and prioritize the 457(b) for the bulk of new contributions after that. The reasoning comes down to access, not capacity: the loan ceiling is shared between the two plans either way, so it doesn't favor one over the other. What favors the 457(b) is that it doesn't restrict when you can start withdrawing after separation from service, while the 401(k) generally does until 59½, unless the Rule of 55 applies (55 for most participants, 50 for qualified public safety employees). That difference matters most if you're aiming for an earlier retirement: the 457(b) removes the waiting period entirely, while the 401(k) only catches up once you reach the applicable age.

This is a framework, not a formula, and it assumes you're not already maxing out both plans. If you are, the sequencing question doesn't really apply, and deferring the full $49,000 combined, more with catch-up contributions, is a notable opportunity in its own right for higher-income households looking for more ways to defer current income. Otherwise, how this applies depends on your income, your timeline, whether the Rule of 55 or its public safety equivalent applies to you, and your plan's specific rules for catch-up contributions. This is where personalized analysis tends to matter.

Sources

[1] California Department of Human Resources, “Savings Plus Program,” calhr.ca.gov.

[2] CalPERS, “Deferred Compensation,” calpers.ca.gov/members/retirement-benefits/deferred-compensation.

[3] California State University, Fresno, Administration and Finance, “2026 Comparison Chart: 401(k) vs. 457(b).”

[4] California State University, Northridge, Human Resources, “Savings Plus Program.”

[5] Internal Revenue Service, “Issue Snapshot: Borrowing Limits for Participants with Multiple Plan Loans,” irs.gov (IRC §72(p)(2)(A)).

[6] Nationwide Retirement Solutions, “Savings Plus Loan Fact Sheet,” nrsforu.com.

[7] Internal Revenue Service, “401(k) Plan Hardship Distributions: Consider the Consequences,” irs.gov.

[8] Internal Revenue Service, “Retirement Plans FAQs on Designated Roth Accounts,” irs.gov.

[9] Internal Revenue Service, “Retirement Topics: Exceptions to Tax on Early Distributions,” irs.gov.

[10] Fidelity, “What Is the Rule of 55?” fidelity.com.

[11] Internal Revenue Service, “401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500,” irs.gov/newsroom.

[12] Nationwide Retirement Solutions, “IRS Contribution Limits,” nrsforu.com.

[13] Internal Revenue Service, “Retirement Topics: Catch-up Contributions,” irs.gov; Quarles Law Firm, “SECURE 2.0 Act Retirement Plan Update: Roth Catch-Up Contributions in 2026.”

Disclosures

Fiduciary Financial Advisors does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action. Before investing, consider investment objectives, risks, fees, and expenses. Investments in securities involve the risk of loss, including loss of principal. Past performance is no guarantee of future returns. The views and opinions reflected in the content are subject to change at any time without notice. The content speaks only as of the date indicated. Some information was obtained from external sources. The information is believed to be accurate, but there is no guarantee that it is.

This content is for educational purposes only and does not constitute personalized tax, legal, or investment advice. Consult a qualified CFP®, CPA, or attorney before taking action.

Fiduciary Financial Advisors is a registered investment adviser. Nothing here constitutes individualized investment advice. Examples are illustrative only and not recommendations. No guarantee of future results. Third-party data is not independently verified.

CFP® and CERTIFIED FINANCIAL PLANNER® are certification marks owned by the CFP Board.