You Left Your CalPERS Employer. Now What?

A plain-language guide to your options when you leave a CalPERS-covered job before you're ready to retire

Maybe you landed a role in the private sector. Maybe you relocated for family reasons. Maybe the job just wasn't the right fit anymore. Whatever happened, you've left your CalPERS-covered employer before retirement, and now you have the question: what actually happens to the benefits you've been building?

The short answer is that CalPERS doesn't disappear from your life. This article walks through those choices in plain language so you can make an informed decision rather than a default one.

What You've Built

When you work for a CalPERS-covered employer, two things are happening in your account at the same time. First, you're making employee contributions, which are a percentage of your salary set by your retirement formula and membership tier. Second, your employer is making its own contributions on your behalf into the broader fund. Only the first bucket (your own contributions plus the interest they've earned) is refundable to you. Employer contributions aren't yours to take with you; they go toward funding pension benefits for current and future retirees across the system.[1]

The pension benefit itself, that lifetime monthly payment you've heard described as "2% at 62" or "2.7% at 57" or some similar formula, isn't funded from a personal account the way a 401(k) is. It's a defined benefit: a promise from CalPERS to pay you a calculated amount for life once you reach eligibility.[2]

Are You Vested?

Your vesting status is the key factor in understanding your options. CalPERS uses a two-part test: you need both sufficient service credit and minimum age to collect.[3]

The Service Credit Side

For most CalPERS members, the vesting threshold is five years of CalPERS-credited service. There are some exceptions, most notably for State of California Second Tier employees, who generally need 10 years, but the five-year mark applies to the large majority of members working for state agencies, cities, counties, etc.[3]

If you've crossed that five-year threshold, you're considered vested in the pension side of things, meaning the right to a future benefit is locked in regardless of where you work next. If you haven't yet hit five years, you don't have a right to a future pension unless you return to CalPERS-covered employment, use reciprocity with another qualifying public retirement system, or had part-time status that qualifies under a specific exception.

The Age Side

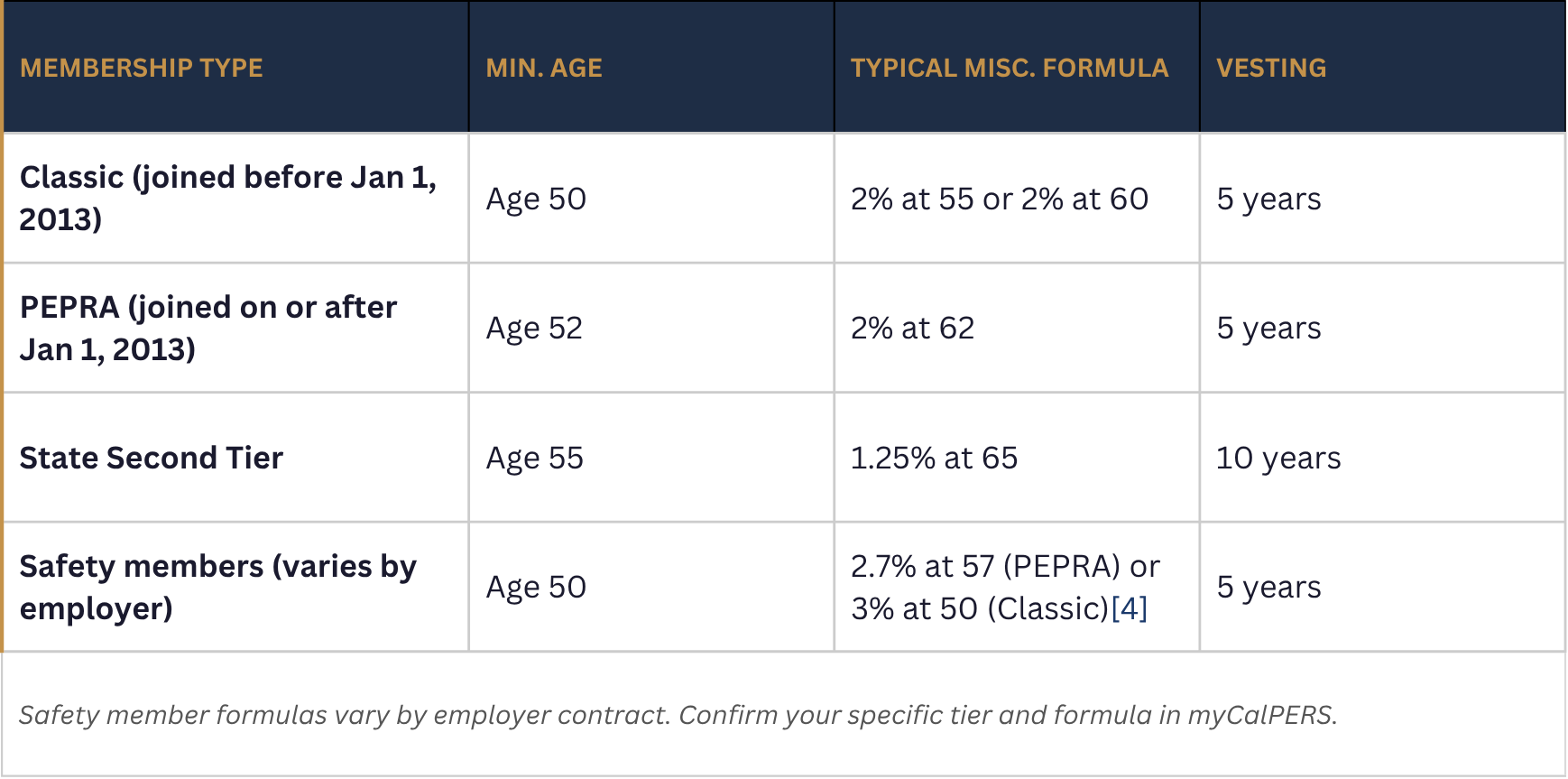

Vesting in the service credit sense doesn't mean you can start collecting tomorrow. You also have to reach the minimum retirement age for your formula, which varies depending on when you became a CalPERS member:[4]

So, for example, if you're a 38-year-old Classic miscellaneous member with eight years of service credit and you leave your employer today, you're vested in the service credit sense, but you can't collect until you reach at least age 50. That gap, between your separation date and your earliest retirement eligibility date, is what makes the decisions below so consequential.

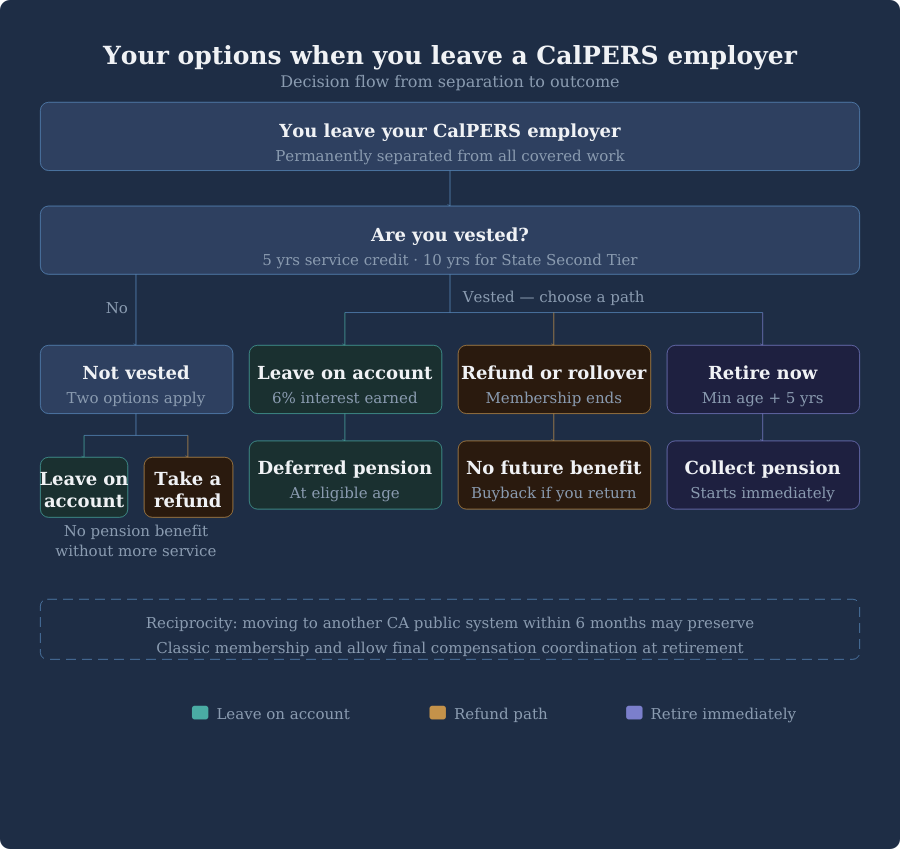

Your Three Main Options at Separation

Once you've permanently left all CalPERS-covered employment, CalPERS will mail you a document called Options at Separation. It lays out what comes next. In practice, you have three paths.[5]

Option 1: Leave Your Contributions on Account

You can leave your employee contributions exactly where they are, earning interest, until you reach minimum retirement age and choose to retire. CalPERS credits accounts left on deposit with interest at a rate of 6% per year, and your membership and service credit remain fully intact.[6]

If you're vested, this approach preserves your right to a lifetime pension payment starting at minimum retirement age. The pension amount you'd eventually receive is based on your service credit at separation, your final compensation, and your age when you actually retire. You won't earn additional CalPERS service credit during the years you're working elsewhere, but the credit you built doesn't evaporate.

One thing to know about this option: under federal Required Minimum Distribution rules, if you haven't retired or refunded your account, CalPERS will eventually require a distribution. The age threshold depends on your birth year: age 73 for those born between 1951 and 1959, and age 75 for those born in 1960 or later.[7] If you're leaving public employment mid-career, that deadline is likely far enough away to not be a factor in the initial decision.

Option 2: Take a Refund or Roll Over Your Contributions

You can request a refund of your employee contributions and the interest they've earned. This terminates your CalPERS membership. Once you choose this path, you forfeit your right to any future pension benefit, disability retirement, or survivor benefits under CalPERS.[8]

The refund is taxable as ordinary income unless you roll it over into a qualified retirement account (an IRA or an eligible employer plan that accepts rollovers). If you receive the money directly, CalPERS is required to withhold 20% for federal income tax, and you may face an additional 10% early withdrawal penalty if you're under 59½ and don't roll the funds over.[9]

If you later return to CalPERS-covered employment and want to buy back your prior service credit, you can do so, but the cost is typically higher than what you were originally refunded, and it increases over time as interest accrues.[8]

Option 3: Retire Immediately (If You're Eligible)

If you've reached minimum retirement age and have at least five years of service credit, you may be eligible to apply for retirement now rather than deferring it.[4] This tends to come up most often for members who've spent a longer career in public service, or who are separating later in their working years.

Retiring at the minimum age typically means accepting a lower benefit factor than if you waited, since most CalPERS formulas are structured to reward retiring later. It also means your CalPERS health benefits question comes into focus immediately (more on that below). For many people, the timing question of when to start CalPERS benefits involves a breakeven analysis that intersects with Social Security timing, other savings, and healthcare coverage, so it pays to run those numbers before making the call.

Reciprocity With Another Public Retirement System

If you're leaving one public employer and heading to another, or you're considering it, CalPERS has reciprocal agreements with most other California public retirement systems. Reciprocity allows you to coordinate benefits between systems in a way that tends to be more favorable than treating them as entirely separate.[14]

The mechanics work like this: there's no transfer of funds or service credit between systems. Instead, when you retire from both systems simultaneously (using the same retirement date), your highest final compensation from either system can be used to calculate the pension from each. You draw separate retirement payments from each system.[14]

To establish reciprocity, the main rule to know is the six-month window: you need to move from one reciprocal system to the next within six months, without a gap in active membership.[15] If you take more than six months off before joining a new public employer, reciprocity likely won't apply.

Reciprocity also affects your CalPERS membership tier. Classic members who move to another CalPERS-covered employer within six months typically retain their Classic membership status, which matters quite a bit given the more generous formulas Classic tiers carry relative to PEPRA.[16]

Reciprocal systems include, but are not limited to Other CalPERS-covered employers (which automatically share membership); CalSTRS (California State Teachers’ Retirement System); County “1937 Act” systems such as LACERA, SCERS, and others; San Francisco Employees’ Retirement System (SFERS); and various other qualifying California public retirement systems. If you’re moving to a position under one of these systems, ask both systems about reciprocity before your start date.

What to Think Through Before You Decide

The options at separation aren't equally consequential for everyone. Here is what you should think through:

• Are you vested? If you haven't hit five years of service credit, your options look different than if you have. A non-vested member taking a refund isn't forfeiting a pension they'd otherwise have. A vested member doing the same often is.[3]

• How long until minimum retirement age? The longer the runway, the more you want to think carefully about whether leaving contributions on account makes sense.[4]

• Will you return to public sector work? If there's any realistic chance you'll come back to a CalPERS employer, keeping your membership intact is probably the better decision. Service credit is additive, and buying it back later is expensive.[8]

• What's the reciprocity picture? If you're heading to another California public employer, verify the six-month window and establish reciprocity before your start date. This is one of the decisions that's easy to get right.[15]

• What does your retirement income picture look like overall? CalPERS pension income, if it's eventually payable, is one piece of a broader picture that often includes Social Security, your Savings Plus Program (which is comprised of a 457(b) and 401(k) plan), or other deferred compensation balance, and non-retirement savings. The refund decision looks different depending on what else is in that picture.

• What's the tax impact of a refund? If you're taking a refund in a year with high other income, the tax drag can add up. If you're in a lower-income year, the impact is more manageable. Rolling into an IRA avoids current taxation but still closes the CalPERS door.[9]

Don't Lose Track of Your Account

CalPERS will send you an Annual Member Statement every fall, but those go to the address on file. Keep your contact information current in myCalPERS, and check your account periodically, especially as you approach your eligible retirement window.[17]

This is where it gets personal.

The choice between leaving contributions on account, taking a refund, and establishing reciprocity intersects with your tax situation, your other retirement savings, your career plans, and how you model lifetime income. The right answer depends on the details of your situation. If you've recently left a CalPERS-covered employer and want to think through your specific numbers, I'm happy to help you work through it.

Sources

1. CalPERS. "Refund Member Contributions." calpers.ca.gov/page/active-members/retirement-benefits/refund-member-contributions

2. CalPERS. "Service & Disability Retirement." calpers.ca.gov/members/retirement-benefits/service-disability-retirement

3. CalPERS PERSpective. "CalPERS 101: Your Pension and the Vesting System." news.calpers.ca.gov/your-calpers-pension-is-on-a-vesting-system-heres-what-that-means

4. CalPERS. "Options at Separation" (PDF). calpers.ca.gov/documents/options-at-separation/download

5. CalPERS. "Options at Separation" letter (PDF). calpers.ca.gov/documents/options-at-separation/download

6. CalPERS. "A Benefits Guide for Public Agency Members" (PDF). calpers.ca.gov/documents/new-member-public-agency-guide/download

7. SECURE 2.0 Act of 2022; IRS Final Regulations on Required Minimum Distributions (89 Federal Register 58886, eff. Jan. 1, 2025). federalregister.gov/documents/2024/07/19/2024-14542/required-minimum-distributions

8. CalPERS. "Refund Member Contributions." calpers.ca.gov/page/active-members/retirement-benefits/refund-member-contributions

9. CalPERS. "Refund Election Form Packet — Special Tax Notice: Your Rollover Options" (PDF). calpers.ca.gov/documents/refund-election-form-packet/download

10. CalPERS. "Eligibility & Enrollment (Active Members)." calpers.ca.gov/members/health-benefits/eligibility-and-enrollment

11. CalPERS. "COBRA Coverage." calpers.ca.gov/members/health-benefits/eligibility-and-enrollment/cobra

12. CalPERS. "Eligibility & Enrollment (Retirees)." calpers.ca.gov/retirees/health-and-medicare/eligibility-and-enrollment

13. CalPERS PERSpective. "Health Vesting 101." news.calpers.ca.gov/health-vesting-101/

14. CalPERS. "Reciprocity (Linking Retirement Systems)." calpers.ca.gov/members/retirement-benefits/reciprocity

15. CalPERS PERSpective. "What You Need to Know About Reciprocity." news.calpers.ca.gov/what-you-need-to-know-about-reciprocity-2/

16. CalPERS. "Public Employees' Pension Reform Act (PEPRA)." calpers.ca.gov/page/about/laws-legislation-regulations/public-employees-pension-reform-act

17. CalPERS. "A Benefits Guide for Public Agency Members" (PDF). calpers.ca.gov/documents/new-member-public-agency-guide/download

Disclosures

Fiduciary Financial Advisors does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action. Before investing, consider investment objectives, risks, fees, and expenses. Investments in securities involve the risk of loss, including loss of principal. Past performance is no guarantee of future returns. The views and opinions reflected in the content are subject to change at any time without notice. The content speaks only as of the date indicated. Some information was obtained from external sources. The information is believed to be accurate, but there is no guarantee that it is.

This content is for educational purposes only and does not constitute personalized tax, legal, or investment advice. Consult a qualified CFP®, CPA, or attorney before taking action.

Fiduciary Financial Advisors is a registered investment adviser. Nothing here constitutes individualized investment advice. Examples are illustrative only and not recommendations. No guarantee of future results. Third-party data is not independently verified.

CFP® and CERTIFIED FINANCIAL PLANNER® are certification marks owned by the CFP Board.