86% of California State Employees Are Handling Their Finances Alone.

Here’s What They May Be Missing.

If you work for the State of California, SMUD, Caltrans, CDCR, or any other CalPERS-covered employer, you have access to a strong retirement benefit package. A defined benefit pension, Savings Plus 401(k) and 457(b) options, and (depending on your role) Social Security coordination that often requires careful planning.

And yet, according to a recent financial preparedness survey of nearly 5,000 California state employees, the overwhelming majority of you are navigating all of that on your own.[1]

That’s not a judgment. It’s a data point. And it’s worth understanding why it matters.

What the Research Actually Says

The 2024 California State Employees Financial Preparedness Report, published by the California State Employees Association (CSEA) and based on a survey of active and retired state workers, found some numbers that are hard to ignore:[1]

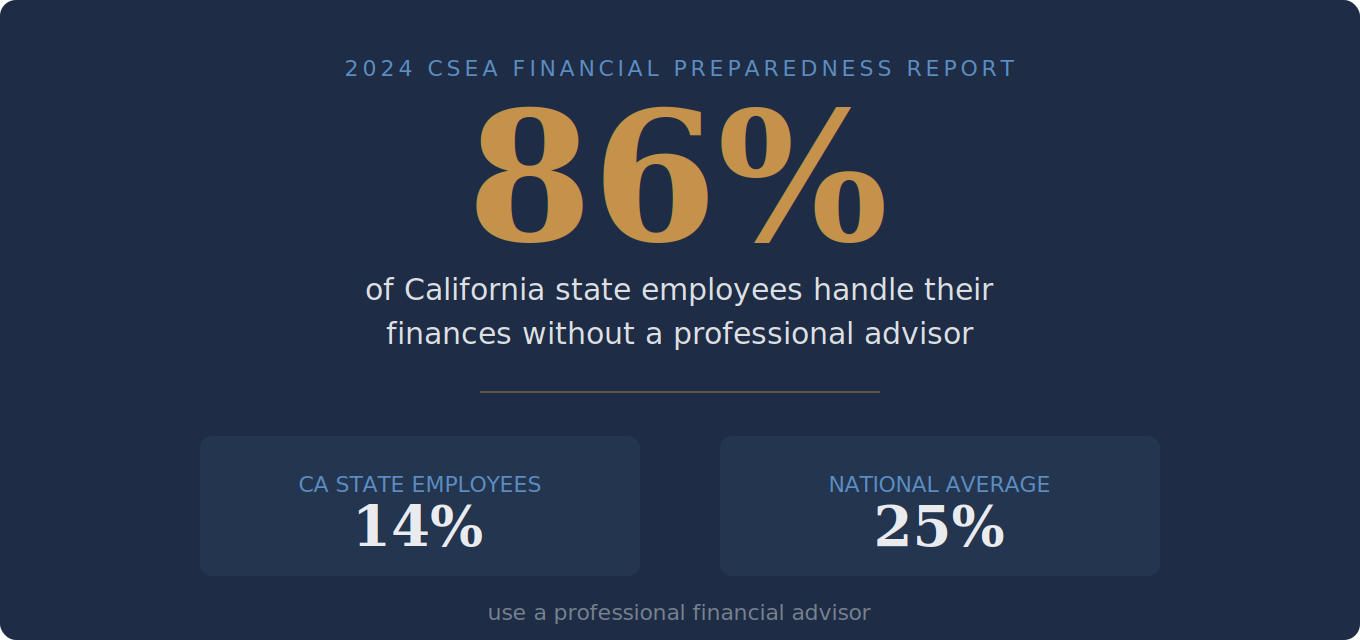

86% of California state employees handle their own financial and retirement planning, relying on friends, family, and online resources rather than a professional advisor.

Only 14% use a professional financial advisor, compared to roughly 25% of Americans nationally.

When researchers asked why, the answers were familiar: it costs too much, I don’t have enough saved, I haven’t found someone I trust, or I just don’t think I need one.[1]

Those are all reasonable-sounding explanations. But here’s where the data gets interesting, because the same survey measured how those two groups actually feel about their financial lives.

The Confidence Gap You Can Measure

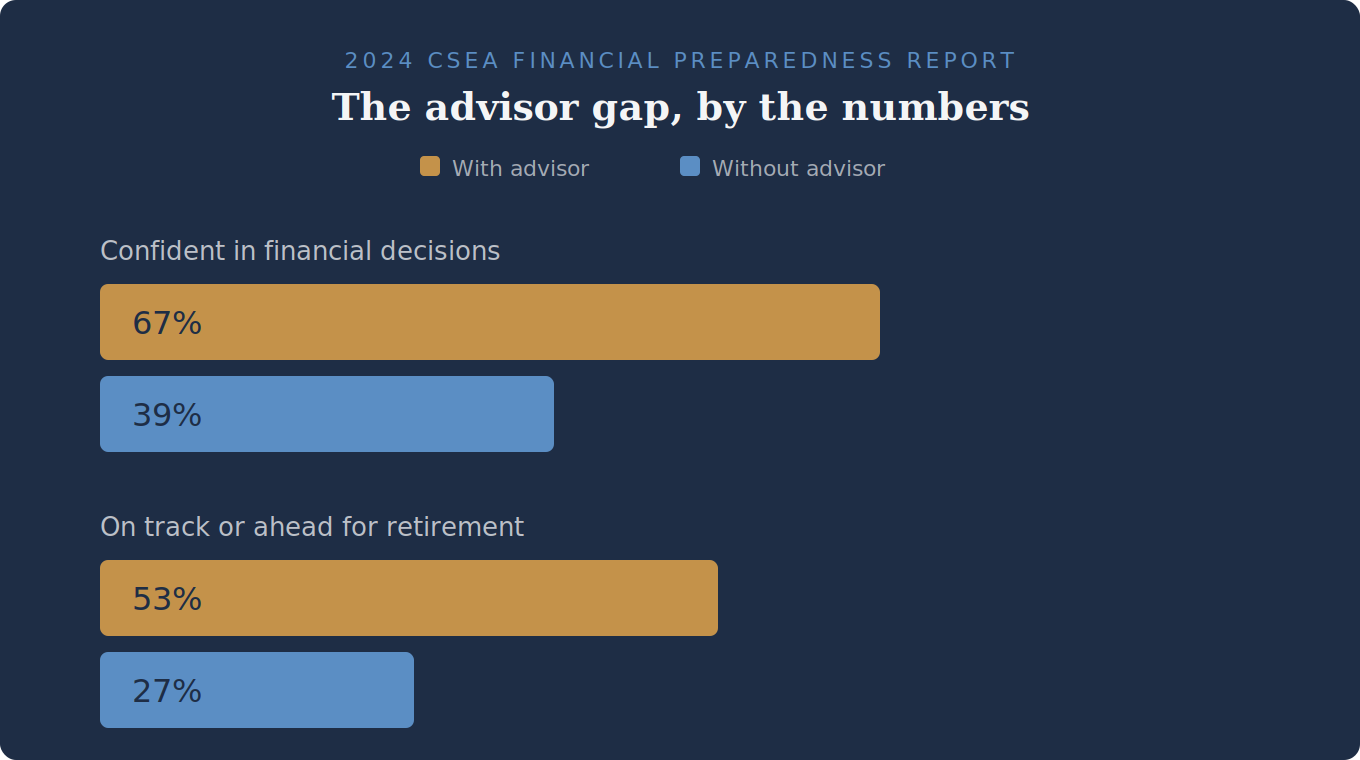

State employees with an advisor: 67% felt confident in their financial decision-making. State employees without an advisor: 39%.

State employees with an advisor: 53% said they were on track or ahead of schedule for retirement. State employees without an advisor: 27%.

That’s not a marginal difference. That’s roughly double the confidence and nearly double the retirement readiness, at least as self-reported.[2]

Now, correlation is not causation (people who seek out advisors may already be more financially engaged). But the gap is wide enough to raise a question worth sitting with: if you’re in the 86% handling your finances without professional guidance, what are the odds there are opportunities you haven’t fully considered?

What DIY Planning May Miss for CalPERS Employees

The reason this matters more for public employees than, say, someone with a basic 401(k) and no pension is that your benefits stack is notably complex. There are moving parts that interact with each other, and because some of those decisions (like your pension option election or retirement date) are difficult or impossible to undo, the cost of a misstep may compound over time.

Here are some of the areas where a qualified advisor tends to help clarify the picture for CalPERS members:

Pension Timing and Retirement Date Optimization

Your CalPERS benefit is calculated using a formula, and the timing of when you retire may significantly affect your monthly benefit for life. Retiring right before versus right after a birthday quarter, for example, may change your benefit factor. Many employees look at their pension estimate and assume that’s the number, without realizing that a few strategic adjustments to timing could increase their monthly income (or overlook the impact that a prior divorce may have if the pension benefit was part of the settlement).

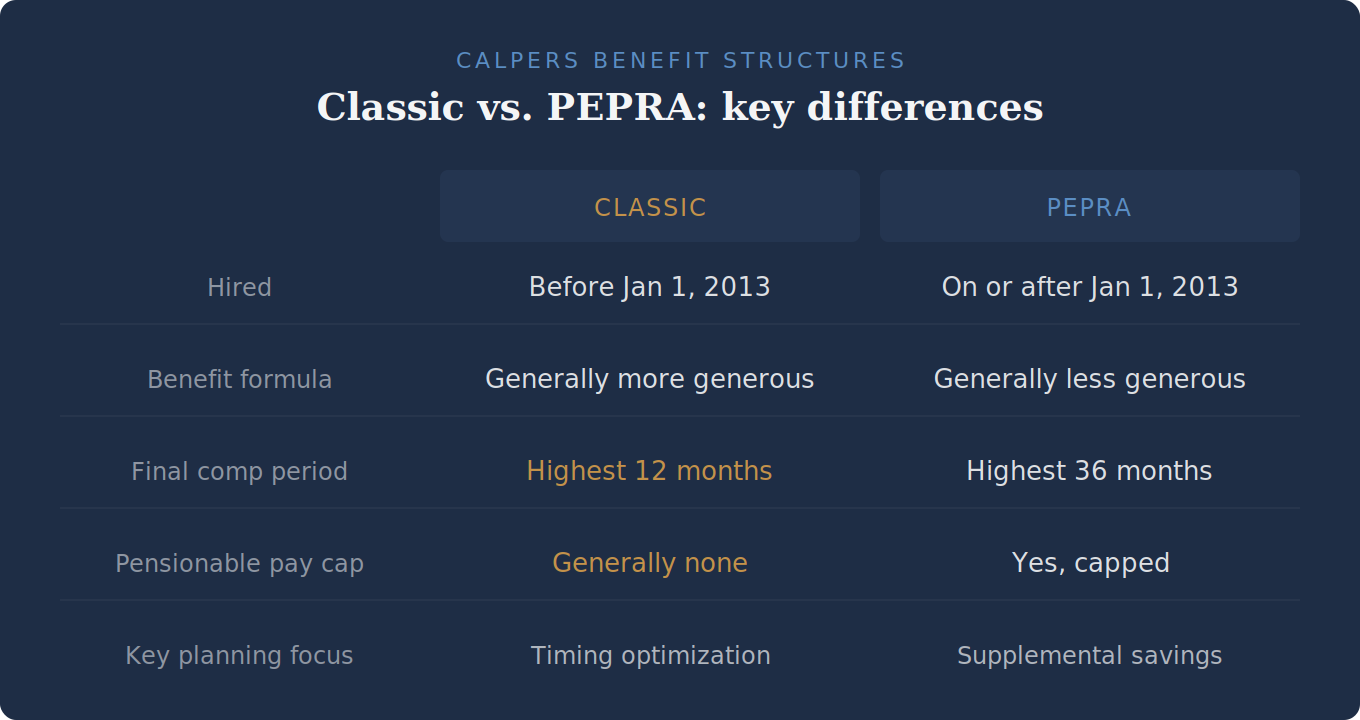

And the stakes here differ depending on when you were hired. If you started with a CalPERS-covered employer before January 1, 2013, you’re a “Classic” member with a generally more generous benefit formula, and your final compensation is based on your highest 12 consecutive months of pay. If you were hired on or after that date, you fall under PEPRA (the Public Employees’ Pension Reform Act), which uses a generally less generous formula, a 36-month final compensation period, and a cap on the salary that counts toward your pension. (For simplicity, this overview focuses on miscellaneous members. Safety members and State Second Tier members have different formulas and benefit structures.)[3]

That’s a significant difference. A Classic member nearing retirement may have a richer benefit, but that also means more complex optimization decisions around timing, final comp windows, and retirement option elections. A PEPRA member, on the other hand, is generally working with a less generous formula, which may make supplemental savings strategy and tax planning that much more important for closing the gap between their pension income and the retirement lifestyle they want. Either way, understanding which set of rules applies to you (and how to work within them) is one of the areas where professional guidance may be worth exploring.

Savings Plus Strategy (the 401(k)/457(b) Decision)

If you’re a state employee, you have access to both a 401(k) and a 457(b) through Savings Plus, which means you may be able to contribute up to $49,000 per year in 2026 (or more if you’re over 50 or nearing retirement and eligible for catch-up provisions).[4] But many employees may not be maximizing both plans, and may not be thinking strategically about whether to use pre-tax, Roth, or a combination. The right answer depends on your current tax bracket, your expected pension income, your other sources of retirement income, and your timeline. This is especially true for PEPRA members, whose pension formula and pensionable pay cap may make supplemental savings through Savings Plus an important lever for building retirement security.

And if you work for an employer like SMUD that offers its deferred compensation through Fidelity rather than the Savings Plus/Nationwide platform, the investment options and fee structures are different, which may matter for how you allocate.

Social Security Coordination

Not every CalPERS member pays into Social Security (it depends on your employer’s specific arrangement).[5] For those who do, coordinating your pension income, Savings Plus distributions, and Social Security claiming strategy may noticeably affect your total after-tax retirement income. For those who don’t, understanding how that gap affects your overall plan may be just as important.

Tax Planning Around Retirement

Your CalPERS pension is fully taxable as ordinary income. So are distributions from your Savings Plus accounts (unless they’re Roth). If you’re retiring in California, where state income tax rates may run above 9% for many retirees, the difference between a tax-aware withdrawal strategy and just taking money as you need it may be larger than you’d think.

This is where Roth conversion planning in the years leading up to retirement tends to be especially valuable, and where DIY planners may not realize what options are available to them.

Why Most People Put This Off

(Even When They Know Better)

If you’ve been meaning to get your financial plan together "someday," you’re in very large company. Financial procrastination isn’t laziness. It’s usually one of a few predictable things:

The complexity feels overwhelming. CalPERS alone has multiple benefit formulas, PEPRA vs. Classic distinctions, reciprocity rules, and different employer contracts. Add in Savings Plus, Social Security, tax planning, and retirement timing decisions, and it’s understandable that many people just default to "I’ll figure it out later."

There’s no forcing function until retirement is close. Unlike a leaky roof or a check engine light, the consequences of not having a plan often don’t show up right away. But by the time they do (often in the form of a tax surprise, a suboptimal pension election, or a realization that you can’t retire when you planned), the window to fix things has narrowed.

Trust is a real barrier. The CSEA survey confirmed this.[1] Many state employees haven’t found an advisor they trust, and that’s an understandable concern. Not every advisor understands CalPERS benefits, Savings Plus options, or the specific planning challenges that come with public sector employment. Working with someone who doesn’t know your benefits package well can sometimes feel worse than doing it yourself.

What to Look for If You’re Considering Working with Someone

If you’re a CalPERS member who’s been thinking about getting professional guidance (even if you’ve been thinking about it for a while), here are a few things that tend to matter most:

Fiduciary standard. Look for an advisor who is legally required to act in your best interest, sometimes referred to as a fiduciary. That’s an important distinction worth understanding when evaluating any advisor relationship.

Familiarity with public sector employees and pension benefits. There’s a difference between a generalist financial planner and one who has experience working with pension benefits and public sector employees. Ask whether they’ve worked through pension optimization, deferred compensation strategy, and retirement tax planning with people whose benefits look like yours. Ask how many clients they serve in similar situations.

A comprehensive approach, not just one piece of the puzzle. A good financial plan for a CalPERS member doesn’t stop at a retirement projection. It connects your pension, your supplemental savings, your tax situation, and your investment strategy into a coordinated approach. Look for someone who ties these pieces together rather than addressing them in isolation.

The Bottom Line

You’ve built a career in public service, and the benefits you’ve earned along the way are valuable. But they’re also complex, and the gap between a good plan and no plan may be wider than you’d expect over the course of a retirement.

If you’re one of the 86% who’s been going it alone, that doesn’t mean you’ve been doing it wrong. It might just mean you haven’t found the right fit yet.

Interested in talking through your CalPERS benefits and how they fit into your bigger financial picture? You can schedule a no-obligation introductory conversation below.

Sources

California State Employees Association (CSEA). “2024 California State Employees Financial Preparedness Report.” Published 2024. Survey of nearly 5,000 active and retired California state employees conducted November 2023. N=3,817 active employees (95% confidence, ±2%), N=1,172 retirees (95% confidence, ±2%). Available at cseabenefitsprogram.com.

CSEA. “DIYing Your Own Retirement Savings Plan? Here’s What You Need to Know.” cseabenefitsprogram.com, 2024. National advisor usage estimate (25%) cited from 2022 Harris Poll. Confidence and retirement readiness comparisons derived from the 2024 Financial Preparedness Report.

CalPERS. “Public Employees’ Pension Reform Act (PEPRA).” calpers.ca.gov. PEPRA took effect January 1, 2013, establishing new benefit formulas, final compensation periods, and pensionable compensation caps for members hired on or after that date.

Internal Revenue Service. “401(k) limit increases to $24,500 for 2026; IRA limit increases to $7,500.” irs.gov, November 2025. The 401(k) and governmental 457(b) elective deferral limits are separate, allowing combined contributions of up to $49,000 ($24,500 each) before catch-up provisions.

CalPERS. “Social Security & Your CalPERS Pension.” calpers.ca.gov. Social Security coverage varies by employer arrangement. Non-covered positions (often safety classifications and certain State of California roles) do not withhold Social Security taxes. The Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) were repealed by the Social Security Fairness Act, signed into law January 5, 2025.

Disclosures

This post is for educational purposes only and does not constitute tax, legal, or investment advice. Please consult a qualified financial planner, CPA, and/or attorney before making decisions about your investments.

Investment advisory services are offered through Fiduciary Financial Advisors, a registered investment adviser. This material is for educational and informational purposes only and is not individualized investment, tax, or legal advice. Equity compensation rules are complex and outcomes depend on plan terms, trading windows, holding periods, and individual tax circumstances. Consult your CPA and/or attorney regarding your situation. Any performance shown is historical, for illustrative purposes, and does not indicate future results. Examples are not representative of all securities or outcomes and are not recommendations to buy or sell any security. Data may be obtained from third-party sources believed to be reliable but not independently verified.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.