Asset Location: Optimizing Your Investments For Tax Efficiency

You’ve probably heard the investing basics: diversify your portfolio, keep costs low, stay invested for the long term. All solid advice. But there’s a less-talked-about strategy that may quietly improve your after-tax returns without necessarily changing what you’re invested in or taking on more risk. It’s called asset location, and it’s one of those planning details that tends to separate a thoughtful investment strategy from a generic one.

The concept is fairly simple: different types of accounts are taxed differently, and different types of investments generate different kinds of taxable income (or none at all). Asset location is the practice of deliberately matching your investments to the right account types, with the goal of reducing what you hand over to the IRS. It doesn’t change your overall asset allocation (your mix of stocks, bonds, alternatives, etc.), but it may noticeably improve how much of your return you actually keep.

Vanguard’s research suggests that a well-implemented asset location strategy may add between 0.05% and 0.30% of after-tax return annually,[1] which may compound into real dollars over time. More recent Vanguard research from October 2023 found that going a step further and optimizing placement of equity subclasses like U.S. vs. international and growth vs. value may add up to another 0.10% annually.[2] These are modeled estimates, not guarantees, and results will vary. But the potential is real enough to be worth understanding.

Start With the Accounts

Before you can decide what goes where, it helps to understand the three main investment account types and how each one is generally taxed.

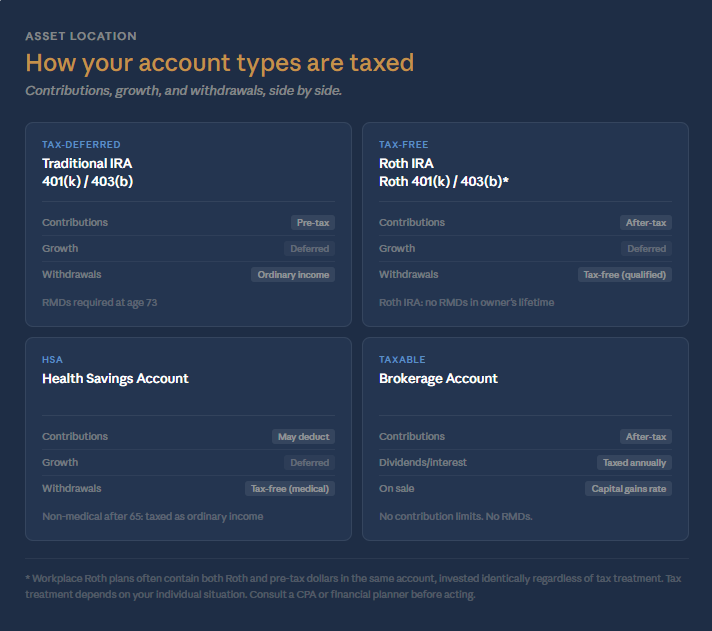

Tax-Deferred Accounts

Contributions to tax-deferred accounts (think traditional 401(k)s, IRAs, and 403(b)s) are typically made with pre-tax dollars, which may reduce your taxable income in the year you contribute. The money can grow without annual tax drag; you can generally buy, sell, and reinvest dividends inside the account without owing taxes on those transactions in the current year. The trade-off is that withdrawals in retirement are generally taxed as ordinary income. These accounts are also subject to required minimum distributions (RMDs) once you reach the required age. (Inherited IRAs come with their own RMD rules that often differ from those that apply to the original account owner, and are worth understanding separately if you’ve received or expect to receive one.)

Tax-Free Accounts

Roth accounts work differently. Contributions go in after-tax with no upfront deduction, but qualified withdrawals in retirement are generally tax-free, including all the accumulated growth. Roth IRA funds are not subject to RMDs during the account owner’s lifetime under current law. For these reasons, Roth funds may benefit the most from strong appreciation over time, since that growth may not be taxed upon qualified withdrawal.

One important nuance worth spelling out: workplace retirement plans like 401(k)s and 403(b)s often hold more than one tax type in a single account (even though it may be a Roth 401(k) or Roth 403(b) in name). Even when an employee is contributing to the Roth side, employer contributions are typically made on a pre-tax basis, meaning the same account may contain both Roth (after-tax) and pre-tax dollars. And because all funds in a workplace plan are invested through the same menu of options, everything is generally invested the same way regardless of the tax treatment of each dollar. That makes workplace plans poor candidates for implementing asset location within the account itself. It is one practical reason why rolling over retirement funds into IRAs, separating Roth dollars into a Roth IRA and pre-tax dollars into a Traditional IRA, may make sense over time, both from an asset location standpoint and for greater flexibility when managing distributions in retirement.

Health Savings Accounts (HSAs)

HSAs are sometimes lumped in with Roth accounts as “tax-free,” and for qualified medical expenses, they actually are. Contributions may be tax-deductible, the funds grow tax-deferred, and withdrawals for eligible healthcare costs are tax-free. That's a combination designed to address those specific planning goals.

As an investment vehicle for general retirement savings, though, HSAs have some real limitations worth keeping in mind. After age 65, you can withdraw HSA funds for any purpose, but non-medical withdrawals are taxed as ordinary income, similar to a traditional IRA. And the inheritance treatment is notably less favorable than a Roth IRA: when an HSA passes to a non-spouse beneficiary, the full account value is generally included in the beneficiary’s taxable income in the year of inheritance.[3] For these reasons, HSAs are often better suited to lower-volatility investments, particularly if the account could pass to heirs or if non-medical withdrawals in retirement are a realistic possibility.

Taxable Brokerage Accounts

Taxable accounts don’t offer upfront deductions or tax-free withdrawals, but they come with flexibility the other account types can’t match. There’s no contribution limit, no RMDs, and generally no restriction on when you can access the money. Investments held here are subject to capital gains tax when sold (at the generally lower long-term rate if held more than a year) and dividends may qualify for preferential tax rates as well.

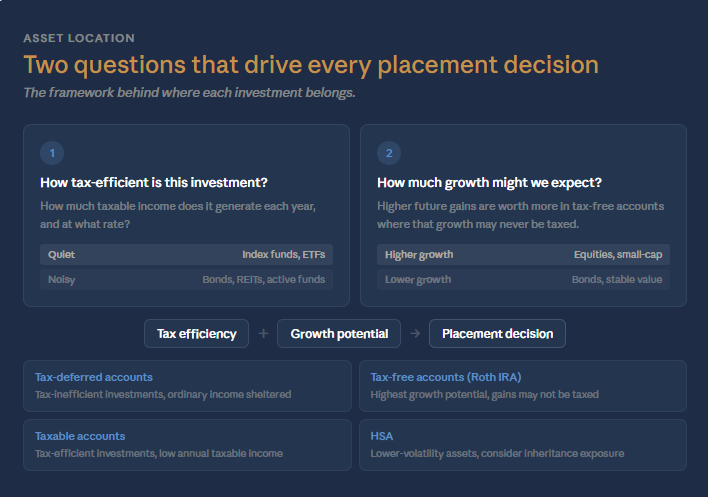

The Two Lenses That Drive Asset Location

Once you understand the accounts, asset location decisions generally come down to two overlapping questions: How tax-efficient is this investment? And how much growth might we expect from it?

Lens 1: Tax Efficiency

Some investments are relatively quiet from a tax perspective. A broad U.S. stock market index fund, for example, typically has low turnover and mostly qualified dividends, meaning it may not generate much of an annual tax bill if held in a taxable account.

Other investments are noisier. Taxable bond funds generate interest income every year, and that interest is typically taxed at ordinary income rates, the same rates that apply to your wages. REITs (real estate investment trusts) present a similar consideration: a large share of their distributions are often treated as ordinary income rather than the more favorably taxed qualified dividends, though they may qualify for a 20% deduction on that income under the Tax Cuts and Jobs Act.[4] Actively managed equity funds with high turnover may also generate short-term capital gains distributions taxed at ordinary rates, rather than the lower long-term capital gains rate that applies to longer-held positions.

The principle that follows: investments that tend to generate a lot of ordinary income are often better placed in a tax-sheltered account, where that income may compound without an annual tax hit. Investments that tend to generate less taxable income, or income that qualifies for lower rates, may be a better fit in a taxable account.

Lens 2: Growth Potential

The second lens is about making the most of your tax-free space. Consider two scenarios: a Roth IRA that grows from $100,000 to $400,000 over time, where all of that $300,000 gain could be tax-free upon qualified withdrawal, versus that same $300,000 gain inside a traditional IRA, which would likely be taxed as ordinary income when withdrawn. All else being equal, you’d take the tax-free account. (Safe assumption.) So apply that thinking to how you allocate within each account: generally, you’d prefer your higher-growth investments to be in the accounts that may not tax the gains.

Higher-growth assets held over long accumulation periods are often considered good candidates to hold more of in Roth accounts, since their future gains may not be taxed upon qualified withdrawal. Conversely, lower-growth, income-producing assets like investment-grade bond funds are often reasonable fits for a traditional IRA. Withdrawals would generally be taxed as ordinary income, but bond interest in a taxable account would likely have been taxed at ordinary rates anyway. The net result is that tax-deferred shelter gets applied where it may provide the most benefit.

Putting It Together: A General Framework

Combining both lenses produces a rough framework, though your specific situation always matters:

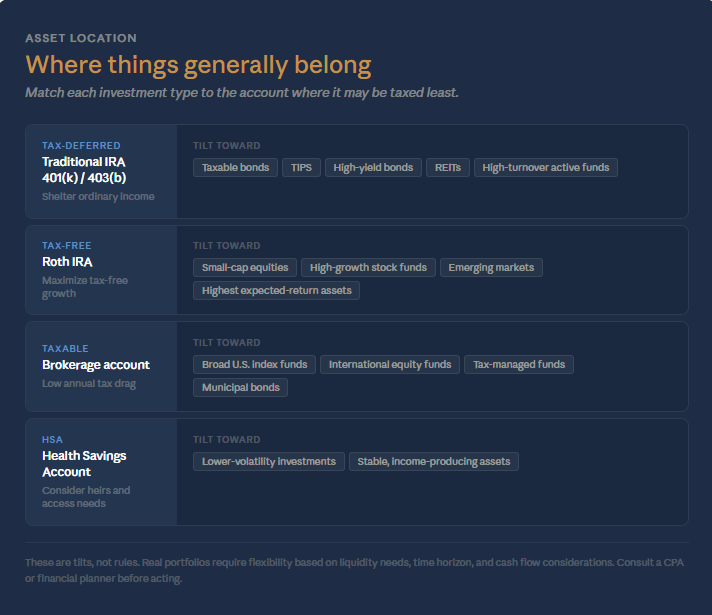

•Tax-deferred accounts: Tilt toward investments that generate more ordinary income. Sheltering that income from annual taxation may help reduce tax drag over time.

•Tax-free accounts (Roth IRAs specifically): Tilt toward assets with stronger long-term appreciation potential, since qualified gains may not be taxed upon withdrawal. As noted above, this applies more cleanly to IRAs than to workplace plans, where the mixed tax nature of the account limits what you can do with asset location.

•Taxable brokerage accounts: Tilt toward tax-efficient assets that generate relatively modest annual taxable income, or assets that carry specific tax advantages that are only accessible when held in a taxable account.

As Fidelity has put it: “You can’t control market returns, and you can’t control tax law, but you can control how you use accounts that offer tax advantages.”[5]

Worth emphasizing: these are tilts, not rules. Asset location is a directional framework, not a rigid prescription. You don’t have to perfectly segregate every holding to get value from it. Holding some bonds in a taxable account, some equities in a traditional IRA, or some growth assets in an HSA doesn’t mean the strategy is broken. It means you’re working with real constraints, which is what everyone is doing.

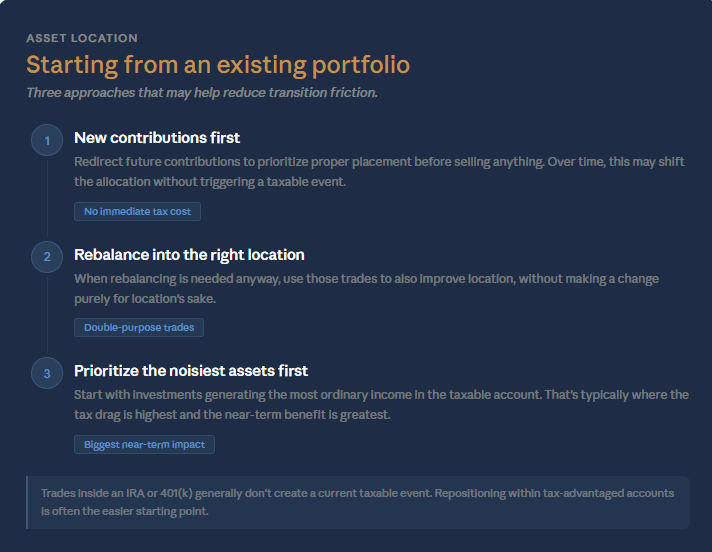

If You’re Starting from an Existing Portfolio

If your investments are already spread across multiple accounts and you haven’t been thinking about asset location, getting started isn’t always as simple as deciding where new contributions go. In many cases, moving toward a better-located portfolio will require selling some existing holdings and repositioning them into different accounts.

That transition has real costs. Selling appreciated investments in a taxable account to move them could trigger capital gains taxes. Depending on how long you’ve held those positions and your current bracket, that tax bill may offset some of the near-term benefit. There’s no universal answer here; it depends on the size of the embedded gain, your time horizon, and your current and expected future tax rates.

A few approaches that may help reduce transition friction:

•New contributions first. Redirect future contributions to prioritize proper placement before selling anything. Over time, this may help shift the allocation without triggering a taxable event.

•Rebalance into the right location. When the portfolio drifts, and rebalancing is needed anyway, use those trades to also improve location. Selling bonds in a taxable account and replacing them with equities while moving the bond exposure to a traditional IRA improves placement without making a change purely for location’s sake.

•Prioritize highest-income-generating assets first. If you can only reposition some holdings in the near term, start with the investments generating the most ordinary income in the taxable account. That’s typically where the tax drag is highest.

For investments already inside an IRA or 401(k), repositioning is generally simpler because trades within a tax-advantaged account don’t generate a current taxable event. If your bonds are sitting in a Roth IRA and your equities are in a traditional IRA, you may be able to swap the allocations without immediate tax consequences.

This is one area where working through the numbers with a financial planner tends to be worthwhile, since the right pace of transition often depends on a careful look at your specific situation.

Layering In Additional Strategies

Asset location works best as part of a broader tax-planning framework. Two strategies that pair naturally with it are tax-loss harvesting and Roth conversions.

Tax-loss harvesting involves strategically selling investments that have declined in value to realize a loss that may offset capital gains elsewhere in the portfolio, or up to $3,000 of ordinary income per year. Because harvesting plays out in taxable accounts, the composition of that account matters. A well-located taxable account holding tax-efficient equities tends to create more harvesting opportunities over time, since equity positions are more likely to experience periodic declines that may be harvested without significantly disrupting the overall strategy.

Roth conversions involve deliberately moving pre-tax dollars from a traditional IRA or 401(k) into a Roth account and paying taxes at today’s rate. Done systematically, particularly in lower-income years before RMDs begin, conversions may grow the pool of tax-free space available for higher-growth assets. These strategies may also reinforce each other: harvested losses in a taxable account can sometimes offset the income generated by a Roth conversion in the same year, potentially reducing the net tax cost of both.

I’ve written in more detail about Roth conversion strategies and the value of coordinated investment planning if either is useful context for how asset location fits in the bigger picture.

A Few Practical Caveats

Asset location tends to add the most value when you have solid balances across multiple account types. If your retirement savings are concentrated entirely in one type of account, there’s limited ability to optimize placement. The more diversity you have across taxable, traditional, and Roth accounts, the more flexibility you have to apply these principles.

Asset location is a portfolio-level strategy, not an account-level one. Each individual account will hold a different mix of investments and will likely perform differently in any given year. A bond-heavy traditional IRA will look very different from a Roth IRA holding primarily equities. If you evaluate each account in isolation, this may feel disorienting. The right lens is how all of your accounts perform together.

Related to that: these decisions don’t exist in a vacuum. Asset location works best when considered alongside your broader accumulation strategy (how you’re building assets across different account types over time), your distribution strategy (which accounts you plan to draw from first in retirement and in what sequence), and your anticipated cash flow needs in both the near and longer term. A placement decision that looks optimal on paper may be less so if it creates friction with how you plan to access the money, triggers unnecessary taxes when you need liquidity, or conflicts with a Roth conversion strategy you’re running in parallel.

As a practical example: it may make sense to hold a sizable bond position in a taxable account for a period of time if those funds are earmarked for a specific near-term purpose, but the time horizon is still longer than a savings account would warrant. That’s not a failure of the strategy; it’s a reasonable acknowledgment that liquidity needs and optimal placement don’t always line up perfectly. The framework is directional guidance, and real financial lives require flexibility.

Rebalancing also requires some coordination. When the overall portfolio drifts from its target allocation, getting it back on track ideally involves trades that don’t create unnecessary taxable events.

And finally: tax law changes. The favorable treatment of qualified dividends and the REIT pass-through deduction under the TCJA have already evolved, and may continue to. A solid asset location strategy is worth reviewing periodically rather than treating as a one-time setup.

The Bottom Line

Asset location may add real value, but it works best on top of a solid foundation: a diversified, low-cost portfolio with an asset allocation that fits your goals and time horizon. The strategy is an optimization layer, not a substitute for getting the fundamentals right first.

For investors who have multiple account types and are in higher tax brackets, the potential is worth taking seriously. Done thoughtfully, it generally comes down to intentional placement decisions made when accounts are funded and revisited as part of ongoing planning.

One honest reality: knowing the right strategy and actually implementing it, then continuing to monitor and maintain it over time, are two different things. If you know you’re unlikely to follow through on the mechanics on your own, or that periodic review tends to slip when life gets busy, working with an advisor as an accountability partner is a practical solution. Beyond building the initial plan, an advisor may help ensure that rebalancing, repositioning, and tax-layer decisions like loss harvesting and Roth conversions actually happen when the opportunity is there, rather than sitting on a to-do list indefinitely. I wrote more about that dynamic in Your Finances Called, if that resonates.

This is where personalized analysis tends to matter most, because the right approach depends on your specific account balances, tax situation, investment mix, and time horizon.

Sources

1. Vanguard, “Asset Location Can Lead to Lower Taxes,” Vanguard Investor Education. investor.vanguard.com

2. Sachin Padmawar et al., “Asset Location for Equity,” Vanguard Research, October 2023. corporate.vanguard.com

3. Internal Revenue Code § 223; IRS Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans. Regarding HSA inheritance: IRC § 223(f)(8); upon death, a non-spouse beneficiary must include the fair market value of the HSA in gross income in the year of the account holder’s death.

4. Internal Revenue Code § 199A; Tax Cuts and Jobs Act of 2017 (P.L. 115-97). The 20% deduction on qualified REIT dividends is currently scheduled to expire after December 31, 2025, absent Congressional action.

5. Andrew Bachman, Director of Financial Solutions, Fidelity Investments, as cited in Fidelity Viewpoints, “Asset Location: Investing in the Right Accounts.” fidelity.com

Disclosures

The information contained in this article is intended for educational purposes only and does not constitute tax or investment advice. Asset location strategies depend on individual circumstances including account balances, tax situation, investment mix, and time horizon. Results discussed in this article are illustrative and modeled; they are not guarantees of future performance. Please consult a qualified financial and/or tax professional for guidance specific to your situation. Tax laws are subject to change; the TCJA provisions referenced, including the Section 199A deduction, are subject to Congressional action beyond 2025.

Investment advisory services are offered through Fiduciary Financial Advisors, a registered investment adviser. This article is for informational and educational purposes only and should not be construed as personalized investment, tax, or legal advice. Any references to scheduling a consultation are for general informational purposes and do not create an advisory relationship. Third-party research, statistics, and survey data cited are believed to be reliable but have not been independently verified. All data is subject to change. References to CFP® professionals relate to industry research and do not imply that any specific outcome will be achieved.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.